Positions: Short France (EWQ)

1. Germany

The latest German unemployment rate ticked down to 7.7% in May from 7.8% in the previous month and continues to trend at a healthy level (especially when compared to Spain at 20.05% or Ireland at 13.4% and the Eurozone average of 10.1%). However, despite a bullish employment report, we’ve noted a recent slowing across fundamentals, which also prompted our sale of the German equity market via EWG in our virtual portfolio last week (see our recent post “The Contagion Drag” on 5/26).

Further, the resignation of German President Horst Koehler late Friday adds political pressure and uncertainty to Chancellor Merkel’s government that has struggled to exude confidence: not only was an aid package to Greece et al not supported, it cost her party (the Christian Democratic Union or CDU) an election in the important economic state of North Rhine-Westphalia (NRW) and uprooted her party’s majority in the upper house of parliament (Bundesrat), which will drive a wedge in the party’s future policy making.

Koehler’s decision to step down resulted from a comment he made last week that “a country like Germany, which is reliant on foreign trade, must know that military intervention could be necessary to uphold economic interests.” His gaffe on a hot-button topic like Germany’s involvement in Afghanistan (Germany has a sizable military presence in Afghanistan but little popular support) prompted the decision. Interestingly, Merkel encouraged the broadly liked Koehler to stay on. While the position of President is very much ceremonial in Germany, the move creates further consternation; a new President is set to be appointed on June 30th.

Lastly, Koehler’s resignation follows CDU state Premier of Hesse Roland Koch’s resignation last week to work in the private sector.

2. France

France’s PPI popped up to 4% in April year-over-year versus 2.0% in March Y/Y. As we’ve called for a ramp in inflation (globally), it’s important to note that we now forecast inflation to dampen on sequentially tougher annual compares as we head into late Q2 and Q3. Nevertheless, our bearish case on France remains and we’re short the country in our virtual portfolio via EWQ. Like Spain and Italy, France’s deficit and debt imbalances will gain the spotlight like Greece and cause further downward pressure on its capital markets. We also expect its AAA sovereign debt rating to be cut.

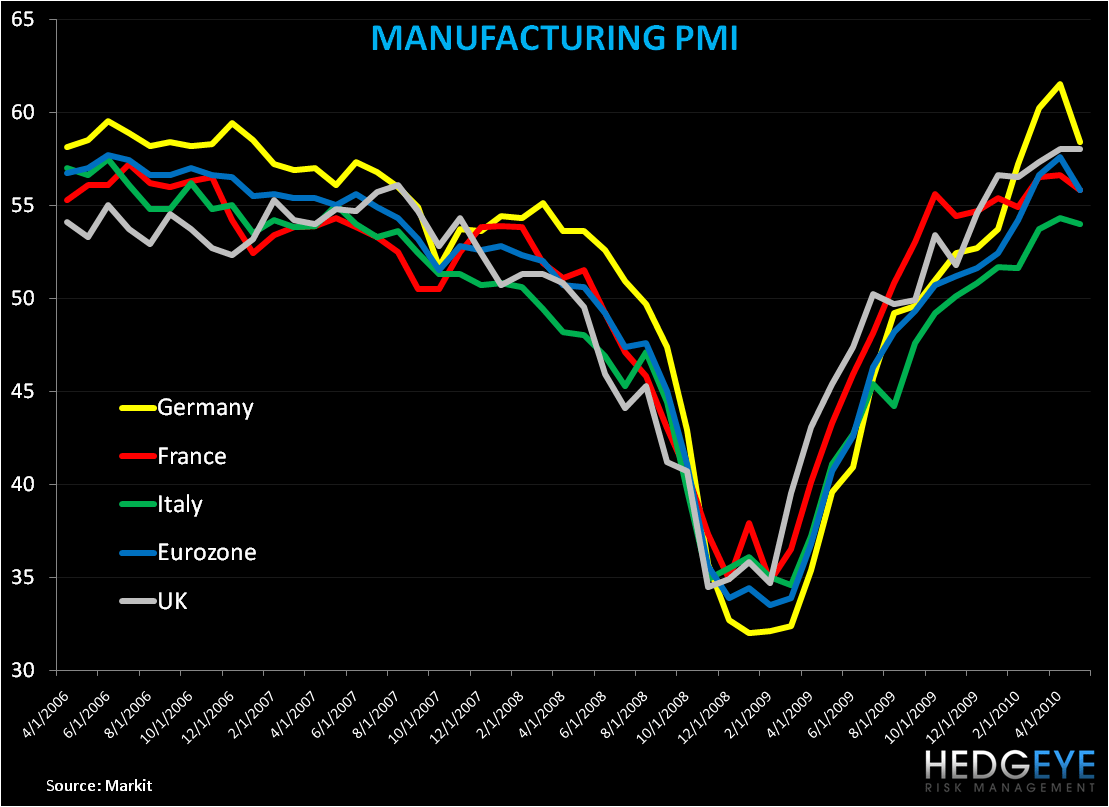

3. Eurozone PMI

Manufacturing PMI contracted across most of Europe with the Eurozone average declining to 55.8 in May from 55.9 in the previous month. The chart below shows waning momentum, reflective of contagion fears, which we’d expect to continue over the coming months.

Matthew Hedrick

Analyst