“I wouldn’t be surprised to see us go to a new recovery high, just to make everybody squirm.”

-Barton Biggs, May 27, 2010

Mornings like these are what I love about this game. A veteran player steps up to the plate and grabs headlines being on the polar opposite side of my positioning. Barton Biggs is now officially the bull who is going to dance with the Thunder Bay Bear.

The aforementioned quote comes from the #2 story on Bloomberg early this morning: “Barton Biggs Says Stock Market Set to Pop in Days.” Notwithstanding that this is a fairly easy call to make after the futures are already “popping”, what I’m more interested in here is whether or not the likes of Mr. Biggs are teeing themselves up for another performance redo of their 2008 seasons. There is systemic risk in that.

With the exception of our short selling and risk management processes, Biggs and I have a lot in common. We both went to Yale. We were both student athletes. We are both overly confident strategists who fancy ourselves as men of the Global Macro Gridiron.

We are both actually pretty grumpy too…

All pleasantries aside, these days it’s Mr. Biggs who is doing the squirming. His NYC based global macro hedge fund, Traxis Partners, cannot afford to prove that the rumor is indeed true – he cannot make money in down markets…

Biggs isn’t alone in this camp. So let’s just call this for what it is. A lot of people grew up in this business like Biggs did, not having to manage interconnected global macro risk on a marked-to-market basis (he was on the sell-side). After going to the buy-side, Biggs missed calling the global macro crash of 2008, and now he is missing the global equity and commodity market meltdowns being perpetuated by the Keynesian Fiat Fools.

I am all for doing global macro but when it comes to defining global macro at Traxis, what is it exactly, Mr. Biggs, that you do? Let’s go through who has been doing the squirming in 2010 to date.

I have no idea what Biggs is down YTD, but here’s a summary of what the perma-bulls in global equities may have missed:

- Asian Equities: Chinese Ox In Box – the Chinese tightened and knocked their stock market to -22% YTD on May 20th

- European Equities: Sovereign Debt Dichotomy has proven disastrous for all of the major European indices, with Greece, Spain, and France down -28%, -24%, -12% YTD, respectively.

- Latin American Equities: Inflation’s V-Bottom has provided the impetus for Mereilles to raise rates in Brazil and mark the Bovespa’s lows at -14% on the YTD low which was established earlier this week.

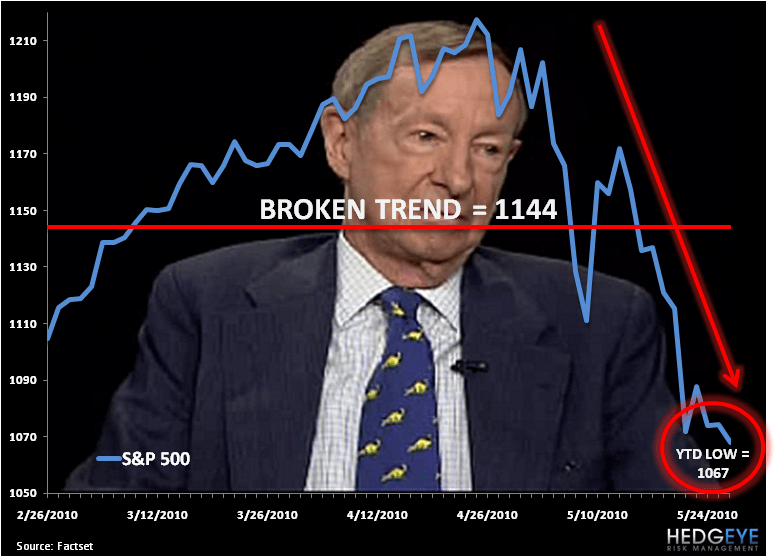

Now if Biggs’ version of global macro is simply being long-only US Equities, he’s probably doing a lot less squirming. After all, all squirming must be relative, right? Nevertheless, he is calling for a “recovery high” on the morning after the SP500 made a fresh YTD low?

The SP500’s closing low of 1067 yesterday was a lower-low for both the YTD and the current cycle. We called for this at the beginning of Q2 with our April Flowers/May Showers slide presentation. I hope Biggs wasn’t buying stocks on the April 23rd peak of 1217, because the market has lost 12.3% of its value since and is now down -4.3% YTD.

We are all for a good bull/bear battle. We want to be the change that we want to see in this business. That starts with being transparent and accountable to our market positioning, real time. If Mr. Biggs is going to get on Bloomberg TV and call our bearish call on European and US Equities “ridiculous”, he will be forced to dance with the Bear in front of a larger audience. Ridiculous is as ridiculous does…

This isn’t Morgan Stanley anymore Barton. Crises in our industry has created a generational opportunity and youth is ambition’s ladder. My former Morgan Stanley analysts are all grown up now. Don’t expect them to be the underlings who will stand down to your former title. The modern day Roman Empire of Wall Street Perceived Wisdoms is falling.

We have moved to 70% cash in our Hedgeye Asset Allocation Model. In terms of US Equities, our asset allocation remains ZERO percent and we are short both the SP500 (SPY) and Nasdaq (QQQQ).

We are still a seller of all buy-and-hope oriented strength. We will likely short the SP500 (SPY) again today. We will cover our shorts when the real squirming out there is over.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer