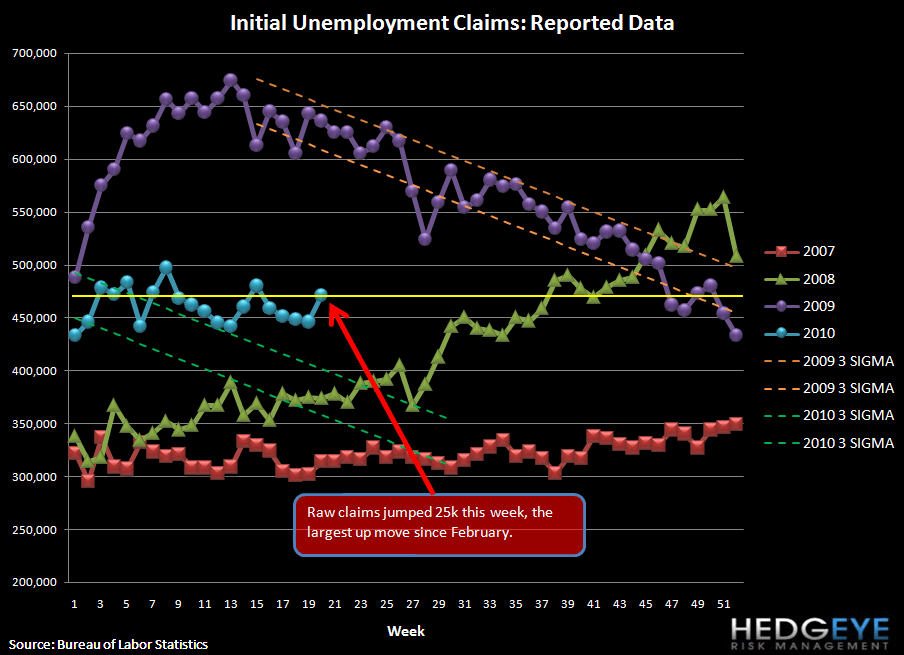

We've been harping on claims for a while now, pointing to the fact that they have been essentially flat for the last five months. This morning they're actually up quite a bit. The initial claims figure rose 25k to 471k from 446k in the prior week (upwardly revised 2k). This takes the 4-week rolling average higher by 3k to 453.5k.

The reality is that without significant improvement in claims, a leading indicator, there will be little improvement in unemployment, and, by extension, net charge-offs for lenders. Remember that most financials, even with the recent sell off, are still pricing in a substantial return to what are considered "normalized" credit costs (i.e. 2005/2006 levels). Based on this morning's number (a continuation of the last 5 months trend), at a minimum, a return to those normalized levels will be delayed. Remember, for unemployment to fall meaningfully, initial claims need to fall to a sustained level of 375-400k. We are 75-100k above that level.

As a reminder around the census, May is the expected peak employment month. Beginning in two weeks the census will become a headwind for job creation.

The following chart shows the census hiring timeline. If the past two cycles are an appropriate model for this year's census, we should start to see Census employment draw down as we move into June, creating a headwind for employment.

Joshua Steiner, CFA

Allison Kaptur

{kind=link}

{kind=link}

{kind=link}