“Don’t tell mom I’m an investment banker. She still thinks I play piano in a brothel.”

– Bruce McKern

Early on in my career on Wall Street I had a friend who ended his Wall Street career after just a few years to become a teacher. He has gone on to become headmaster at one of the best private schools in Ohio, helping to shape the minds of thousands of kids. As for me, I don’t know what it’s like to wake up in the morning and not think about making money.

There are lots of ways to make money legally on Wall Street and some do it better than others. Wall Street storytelling is exemplified by bankers dressing up assets to look better than they are. Then they charge huge fees for this service, while charging you interest on the money you borrow from them (and they can borrow money while paying little to no interest).

Since March of 1792, it does not matter what side of the Street you are on; it’s all about making money. Today, thousands of people are waking up thinking “how can I make money today”, but at the same time they see that Washington is demonizing what has been part of our culture for 218 years.

The excesses of Wall Street are not excusable and are front and center right now, but Wall Street continues to be a necessary and critical part of our culture, and our economy.

With Financial reform on the tip of Obama’s tongue, can the recent string of events be just a coincidence?

(1) SEC charges Goldman Sachs with fraud

(2) Federal prosecutors are investigating whether Morgan Stanley misled investors

(3) Last week the market melts down for some unknown reason….

(4) JPM, GS and BAC have perfect quarters (what were they thinking?)

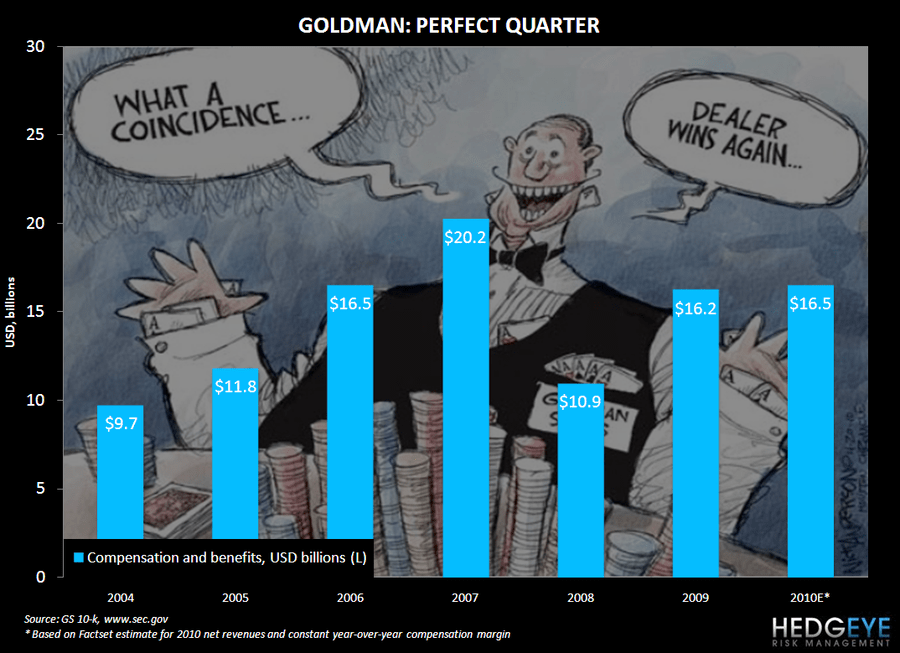

What is not a coincidence is the “Financial Triumvirate” of perfect quarters from JP Morgan, Goldman Sachs and Bank of America (Ken Lewis must be steaming right now). Maybe now it's time for Mr. Bernanke to stop throwing money at the “Piggy-Bankers” who get up every morning and have nothing better to do but think about making money.

He is making life so easy for them….

If you are a client that is on the other side of the “Financial Triumvirate”, you must be thinking “what do they know that I don’t?”. Yes, it’s a stacked house! The big boys have an unfair advantage in knowing exactly what the order flow pipeline looks like, so they can sit back and let their clients come to them for another losing trade. This is a theme Washington can understand!

Even so, you would think that in a “normal quarter” they would still have some trades go against them. Flawless is definitely an outlier and nearly statistically improbable. According to our in-house financial guru, Josh Steiner, in a “normal quarter” the historical charts of profitability distribution suggest that they lose money 5-10% of the time.

When it’s all said and done, Main Street is the biggest loser. The man on the street is not getting paid on his /her savings account while Washington continues to enrich the Piggy-Bankers on Wall Street, whose sole purpose in life is to make money. Last night, the ABC consumer confidence index came in unchanged at -47 for the week ending May 9. The “Financial Triumvirate” may be doing what they do best, but it’s not trickling down to the little guy on Main Street.

After last week, it is much clearer now why the Federal Reserve is keeping rates so low. The European Sovereign debt issues and the size of the new loan facility have exposed the vulnerability of the EU as an economic power, which puts the US in a position of relative strength. Having a sound banking system is critical to maintaining this mystique. This is Dollar bullish!

What can’t be ignored is that the consumer credit cycle of the past 20 years is dead. At the same time, sovereign credit issues, combined with unsupportable entitlement spending, have ushered in an era of political and social instability. This is a negative for the market and equity valuations, and I will point to Healthcare as a classic example. Yesterday, our Healthcare analyst Tom Tobin said to me that he thought that Healthcare as a “safety trade” was gone, as the US and EU governments account for about 50% of payments to Healthcare. Without healthcare, what’s left? Utilities? Please say it’s not so.

How many times in 2008 did you read that “cash is king” and that anything with leverage was going to zero? In 2010 cash is still king and asset valuations are dependent upon the predictability and sustainability of cash flow generation.

Yesterday, we sold our trading long position in QQQQ and took our allocation to US Equities in the Hedgeye Asset Allocation Model back to zero percent. Also, at 12:14 PM we re-shorted the SP500 on strength (SHORTED SPY at $116.69) and our view of the market right here and now with the S&P at 1,155 is implied by our positioning. Financial reform, Healthcare reform, the elimination of the Bush tax cuts, trillion dollar bailouts and the negative credit cycle are all inhibitors to growth.

Wall Street’s interests are not always aligned with those of Main Street, and given what is happening on Main Street today, it is easy to demonize Wall Street. However, not all bankers are bad. Washington is trying to push through its financial reform so it does not want to educate people on the good guys and the critical role they play in today’s economy. Some reform may be necessary, but too much financial reform will not only be an inhibitor to growth, but could also put a damper on a culture that has thrived on the dreams of those waking up, wanting to make money.

Howard Penney

Managing Director