Expecting an in line quarter, it's going to be all about outlook and cost control

"Table drop, slot coin-in and visitation [at River Rock] witnessed double-digit improvements when compared to February 2009. Unfortunately though, the benefit of these increases was offset by a table hold percentage of 14.9%, well below River Rock’s historical average. While this is always very effective marketing, it did in combination with the Olympics related closure of Hastings Racecourse contribute to February 2010 revenues in BC declining by 7.6%, when compared to last year. In January 2010 for comparison, BC revenues were essentially flat, when compared to January 2009."

- Milton Woensdregt, Chief Financial Officer

Milt kind of said it all with the comment above. The local government numbers showing the gov't share of provincial casino revenue numbers also tells us that revenues in 1Q2010 should be modestly down y-o-y. Everyone already knows this, so in this quarter all eyes will be on March and April trends and cost controls. We estimate that GC will report an in-line quarter with revenue of $94MM, slightly below the Street's $95MM estimate. However, despite lower revenues, GC should be able to slightly exceed the consensus EBITDA estimate of $31MM.

Aside from the poor hold at River Rock in February and closure for part of the quarter at Hastings, the y-o-y comparisons are pretty clean - that is, no weather or major hold issues in either quarter. Local share of provincial casino revenues data implies that Great Canadian's BC casinos had a 5% y-o-y decline in gaming revenues. We're estimating a 4% y-o-y decline in BC gaming revenues. On the call we will be focused on:

- March and April trends. We think March was pretty uninspiring - the data implies 3-4% degradation from last year

- Early signs of feedback on the new player tracking rewards program

- Feedback on additions at Georgian Downs and View Royal and the slot refresh at Nova Scotia

- Evidence of control and ROI on their marketing expenditures

1Q2010 Detail

We estimate that River Rock will report $29MM of revenues and $11.4MM of EBITDA.

- We estimate 4% decline or $22.3MM of gaming revenues, assuming:

- 7% increase in drop, 18% hold; 10% increase in slot coin in and 7% win rate

- In 1Q09 table hold was 21.9% and slot win % was 7.1%

- 15% increase in other revenues driven by a 10% increase in F&B and a 29% increase in hotel revenues

- $17.3MM of operating expenses, which compares to $17.4MM last quarter and equates to a 3% increase from 1Q09, driven by an increase in marketing costs.

We estimate Boulevard will report $16.9MM of revenues and $7.8MM of EBITDA.

- We estimate a 4% decline in gaming revenues to $14.4MM, assuming:

- 5% decrease in drop and 19.15% hold; 6% decrease in slot coin in and a 7% win rate

- 1Q09 has an easy hold comparison of 18.3% on tables and slot win % of 6.9%

- We estimate that other revenues are flat relative to 4Q09 results at $2.5MM or up 5% y-o-y

- $9.1MM in operating expenses, down 3% y-o-y

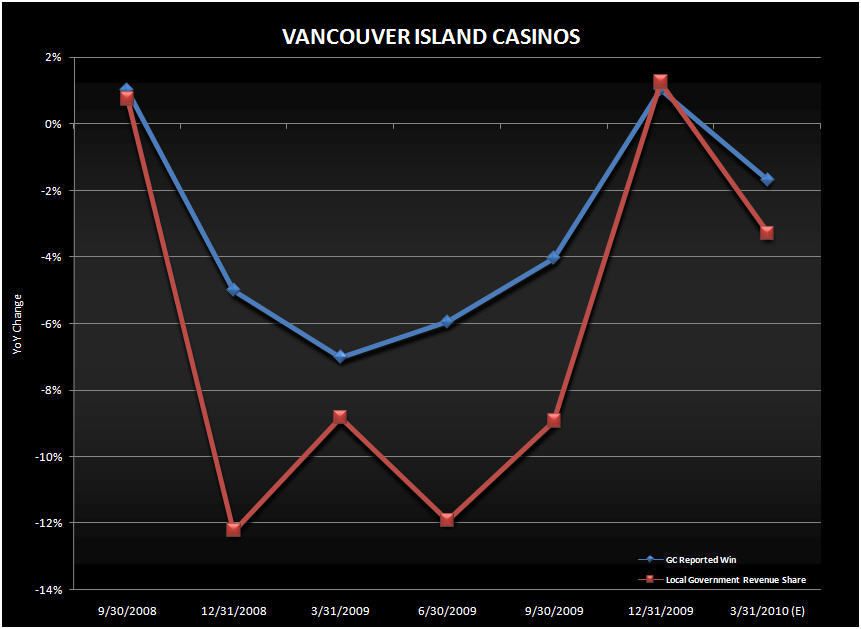

We estimate that Vancouver Island properties will report a $10MM of revenues and $5.9MM of EBITDA.

- We estimate a 2% decline in gaming revenues to $9.1MM, assuming:

- 3% decrease in drop and 23.5% hold; 2% decrease in slot coin in and a 7.2% win rate

- 1Q09 table hold was 24.2% on tables and slot win % of 7.2%

- We estimate that other revenues will increase to 860k.

- Operating expenses flat to 4Q09

Other properties:

- We expect Nova Scotia revenue of $10.8MM and $2.6MM of EBITDA. We actually expect gaming revenues to be up almost 4% at the Nova Scotia properties this quarter and costs to be in-line with last quarter.

- We expect Georgian Downs to be flat with last quarter revenue wise and EBITDA wise.

- Great American properties should be up handsomely due to the FX benefits of a strong Canadian dollar.

- Racetrack revenues should be down about 10% y-o-y given the closure at Hastings.