The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Happy summer. Much has changed in the markets since the last meeting of the Federal Open Market Committee several weeks ago. The target for short-term rates was cut a quarter point and, more important, the runoff of the Fed’s balance sheet ended, removing the tightening bias to US monetary policy.

We had called loudly for the latter and discounted the former, most notably in a discussion on CNBC, so we view the FOMC action as the least that could be done given the political noise coming from the White House. We feel particularly vindicated because Powell and other committee members make clear that no further cuts are likely in the near term. The Street consensus was badly wrong about 2-3 rate cuts in 2019. Philly Fed President Patrick Harker told CNBC’s Steve Liesman on August 22, 2019:

“We’re roughly where neutral is. It’s hard to know exactly where neutral is, but I think we’re roughly where neutral is right now. And I think we should stay here for a while and see how things play out.”

Whether or not anybody on the FOMC actually knows where the neutral rate of interest lies, we do know that short-term rates have eased considerably since the Fed ended the shrinkage of the Fed's System Open Market Account or SOMA. REPO rates for Treasury and agency RMBS collateral have fallen more than half a point in August, albeit on falling volumes, according to the DTCC. The average rate paid was below 2.2% last week and falling, this vs the average of 2.7% at the end of June. Short-term REPO rates spiked over 4% at the close of the second quarter.

Fed Chairman Jerome Powell, Harker and the rest of the FOMC should be watching real market rates and spreads instead of speculating about mythical notions such as neutral rates. The narrative emanating from the Fed’s building in Washington more and more does not track with what we all can see in the markets, thus investors are rightly confused. We know that Chairman Powell likes to speak plainly about policy matters, but he is constrained by the Fed's medieval internal processes and practices.

As we noted in The American Conservative last week (“No, the U.S. Economy Is Not Headed for Recession”): “So the two chief reasons for an inverted yield curve—low or negative interest rates and a huge demand for safe assets—have nothing to do with the direction of the U.S. economy. Indeed, the economy continues to grow strongly, albeit at slower rates than from 2016 to 2018.”

The increasingly assertive Harker and his counterpart in Kansas City, Ester George, are both correct to resist further rate cuts demanded by the howling mob on Wall Street. Sure, equities are more air than earnings, especially the special situations in the unicorn sector – profitless monuments to negative interest rates that only an economist or alpha starved institutional manager loves. Wework, Tesla (TSLA) and Uber (UBER) are just three of our favorite examples.

But even as blue chips trade lower on China related wah-wah, to recall a conversation we had a while back with Ralph Delguidice, opportunities will emerge. After the tears, there will come a time to buy the quality banks and non-bank financials at record low valuations, prices not seen in years. Maybe 3x December '18? The question is how do we arrive at that point given some of the short-term issues we see affecting financials.

The near-term issue of liquidity has been helped by the Fed’s actions with respect to the SOMA, but that only means that the margin squeeze on banks will progress more slowly. Looming down the road is credit. Hope makes stocks rise, but credit makes them fall. Even though default rates remain low, loss given default has started to rise as prices for residential and commercial collateral soften.

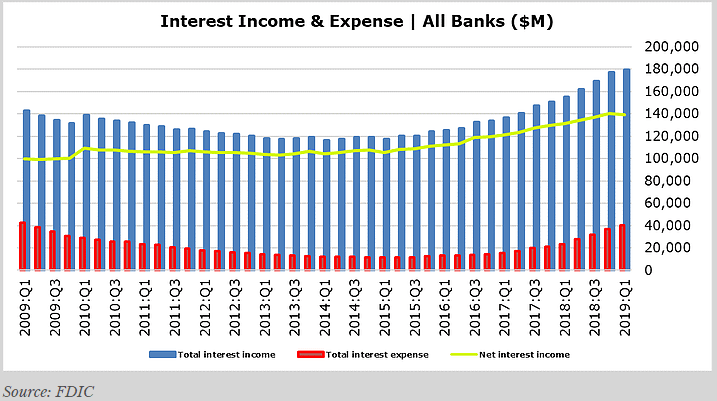

We wait with the greatest anticipation for the release of the quarterly banking profile from the Federal Deposit Insurance Corporation. The release of the industry and bank level data by the FDIC is an important indicator of both the economy and credit trends. One big question that requires validation with the Q2'19 bank data is the state of net interest income in the US banking market.

As we wrote more than a year ago in The Institutional Risk Analyst, net cash income to banks has started to decline under the relentless pressure of short-term interest rates. And as we’ve already noted, the good news is that the rate of increase in bank funding costs has slowed to “only” 30-40% vs 70% year-over-year growth rates in Q1. Yet even with the collapse of middle and long-term yields, the normalization of bank interest expense will continue apace.

We still expect to see total quarterly interest expense for the US banking industry hit $60 billion run rate by the end of the year. Look at the chart below. Ponder what that implies for bank revenue and earnings. And keep in mind that the inverted yield curve does constrain all lenders when it comes to the ability to increase or even maintain price on new loans.

Our friend Joe Garrett of Garrett McAuley in San Francisco notes that default rates are starting to rise, as shown by the latest data from the GSEs and the FHA. Default rates for total loans actually fell slightly in Q2'19, tracking the downward trend in the mostly prime bank portfolio. Yet as we'll be discussing in The IRA Bank Book, rising net default rates suggest that the period of benevolent credit in 1-4 family mortgages is ended.

The FHA market is clearly the hot spot for future loan defaults in the residential mortgage sector, which explains the flurry of proposals coming from Ginnie Mae to manage risk, real and imagined. See our comment in National Mortgage News (“Ginnie Mae and the politics of prepayments”). The next several quarters will include new stresses on banks and non-bank financials as badly distorted prepayment rates and credit spreads intermediaries into a squeeze, the exact opposite of the Volcker-era high rate environment of the 1980s.

We are most impressed by the long-term nature of emerging trends, particularly the possibility that short-term US interest rates may stay significantly above rates in other global markets. Because of the highly developed market for non-bank finance in the US, we suspect that corporate and asset backed yields will remain positive even as the rest of the world sinks into the mud of negative returns. Economies with negative interest rates must, by definition, see a contraction in investment and demand, a little nuance that somehow escapes most economists. Negative rates are a tax on the capital stock of the private sector, clearly a regressive policy in terms of economic growth.

The intriguing possibility we see is a vast increase in capital flowing back into the US as dollar assets offer the only source of positive return for global investors, both private and supranational. When global investors can buy US Treasury debt or GNMA securities and hedge the forward currency risk, that trade becomes compelling. But it only decorates a larger secular trend that could see the US sucking in global capital like a giant economic black hole – this as the rest of the world scrambles to maintain liquidity and revenue.

Does the inverted yield curve predict a coming recession? No, we think it evidences the volatility and distortions caused by the actions of central banks. Thus we agree with Harker and George; the best thing for the FOMC to do at present is nothing. Short-term interest rates are not hurting growth or the financial markets, especially now that the Fed has stopped reducing the size of its balance sheet.

This does not mean, however, that the fact of an inverted yield curve cannot mutate into the cause of an economic slowdown. “If the recent yield curve panic proves anything, it proves that, in financial markets, what may start out as a mere statistical correlation, and possibly a spurious one, can become a genuine causal relationship,” notes Dr. George Selgin at Cato Institute writing on Alt-M (“How to Flip a Yield Curve”). “In particular, if enough people subscribe to a post-hoc fallacy, it may not stay a fallacy for long.”

EDITOR'S NOTE

This Hedgeye Guest Contributor piece was written by Christopher Whalen, author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. This piece does not necessarily reflect the opinion of Hedgeye.