High VIP hold % helps drive market - WYNN and LVS in particular. Here is the property detail.

April was another huge month for gaming revenues which increased 70%. Much of the "huge" growth was driven by VIP table revenues which grew 89% y-o-y, while Mass table revenues increased 36%. Slots were up 28%. While WYNN and LVS gained table revenue share at the expense of all the concessionaires, these sequential gains were driven by much better luck in April vs. March (and much better than normal). Looking at junket RC volumes it appears that just the reverse occurred; WYNN, LVS and to a lesser extent MGM lost share to the three HK-based concessionaires. For WYNN at least, growth in their direct VIP business may have contributed to the higher hold versus volume, which actually wouldn't be such a bad thing.

Y-o-Y Table Revenue Observations

LVS table revenues increased 40%, with growth coming from a 56% increase VIP revenues but only a 16% increase in Mass revenues.

- Sands grew 21%, driven by a 29% increase in VIP revenue and an 8% increase in Mass revenue

- Junket RC increased 43%.

- Hold looks high - roughly 3.3%, but last April's hold was even higher - we estimate 3.6%.

- Venetian was up 21%, driven by a 22% increase in VIP revenues and a 21% increase in Mass

- Junket RC decreased 23% y-o-y, however, hold more than made up the difference. Assuming 18% direct VIP play volume, we estimate that hold for April was 3.7%. Last April, assuming 16% direct play, the hold percentage was only 2.4%.

- Gaming revenue growth would likely have been negative with normal VIP hold.

- Four Seasons was up 475% y-o-y entirely driven by 1360% VIP growth (and massive hold %) with Mass growing a relatively tiny 14%

- Junket VIP RC increased 297% to $649MM. If we assume 35% direct VIP play then hold percentage in the month was north of 5%.

Wynn Macau table revenues were up 87%, primarily driven by a 117% increase in VIP while Mass revenues were only up 11%.

- VIP volumes were driven by Junket RC increase of 77%, high hold, and easy hold comparisons.

- Using the same adjustment factor for direct play in both April 09 and 2010, hold this past month appears to be 3.1% vs. 2.5% last year.

Crown table revenues grew 143%, with the growth fueled by 561% growth in Mass and 113% growth in VIP.

- Altira was up 19%, all due to a 21% increase in VIP revenues which was partly offset by a 16% decline in Mass

- VIP RC was down 4%, but hold comparisons were favorable. Last April hold was only 2.3% while this April it appears to have been 3%.

- CoD table revenue increased 11% sequentially, due to a 15% decrease in VIP win, while Mass was up 1.4%

- Mass was $34MM (they did say that hold was in the low 20's so perhaps drop wasn't so great).

- Junket VIP RC increased 11% sequentially

- If we assume 18% direct play at CoD (in line with what MPEL said on their earnings call), then total VIP RC would be $4.1BN. However, hold in April was very weak at only 1.8%.

SJM continued its hot streak, with table revenues up 87%.

- Mass was up 43% and VIP was up 119%.

- Junket RC volumes increased 130%.

- As we wrote about on several occasions, we believe SJM is being very aggressive on junket pricing.

Galaxy table revenue was up 61%, entirely driven by a 71% increase in VIP win, while Mass increased 18%.

- Starworld's table revenue was up 92%, also entirely driven by 105% growth in VIP revenues, while Mass decreased 15% y-o-y.

MGM table revenue was up 35%.

- Mass revenue growth was 19%, while VIP grew 43%.

- VIP RC grew 26%.

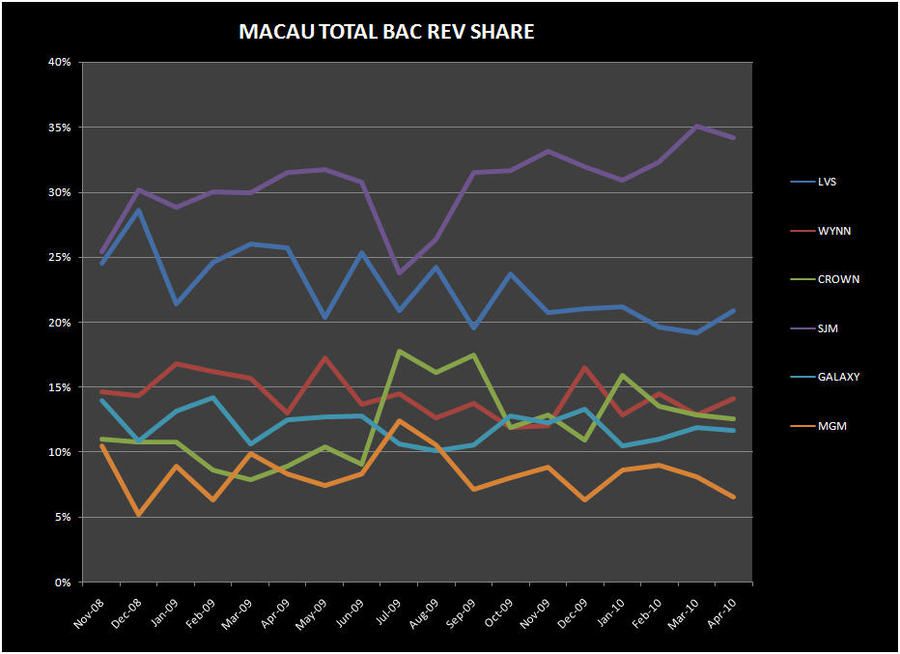

Market Share

LVS share increased 170bps sequentially to 20.9%, with most of the share gain coming from VIP.

- LVS's share of VIP revenues increased to 18.7% from 16.4% in February. However, LVS's share of Junket RC actually decreased 150 bps to 12% which is the lowest share that LVS has had since at least May 2007 (when we started tracking the data).

- Mass share increased by 50 bps to 27.4%.

- Sands gained what it lost last month (44bps), increasing to 6.9% sequentially. Sands gained share across both VIP and Mass win while losing 50bps of junket RC share.

- Venetian gained 30bps to 10.5% sequentially.

- Venetian actually gained 95bps of market share in VIP sequentially to 8.5% but VIP gains were largely offset by a 87bps sequential drop in Mass share. If not for high hold, Venetian's share would have dropped, as Junket RC share fell 80bps to only 5.5% - Venetian's lowest share since opening.

- FS share increased 90bps to 3.5%.

- After SJM, LVS commanded the second highest share of the overall market, mainly due to the strength of their Mass business which commanded market share of 27.4%, followed by Wynn at 9.4%.

WYNN's share increased to 14.1% from 12.9% in March.

- In a reversal of last month's trend, Wynn's gain was entirely driven by higher VIP hold. Wynn's share of the VIP revenues recovered to 15.6% from 14.1% in March. Junket RC fell by 119 bps to 14.4% - falling to fourth place behind SJM, Crown and Galaxy. However, the Encore addition should help in May and as long as they continue to grow their more profitable direct play, which we saw last quarter, it doesn't really matter.

Crown's market share decreased by 30bps to 12.6% in April.

- All of the share loss came from CoD, whose share dropped to 6.4% from 7.5% in March

- CoD's share drop was entirely due to a 1.6% decline in VIP share to 5.9% which was driven by the property's low hold. Junket RC share increased by 100bps to 8.3%.

- Altira's share increased to 6.2% from 5.3% in March. Mass market share decreased slightly by 6bps to 1.2% but was more than offset by VIP share growth of 100bps to 7.8% which was all hold related as Junket RC share decreased by 10bps to 8.2%.

After 3 months of climbing, SJM's share slipped by 90 bps to 34.2% - which is still its 2nd highest share month since Nov 2007.

- Despite share of Junket RC increasing by 70bps to 34.9% in April, VIP share decreased 145bps to 31.2%.

- SJM Mass share increased by 150bps to 43.2% sequentially.

Galaxy's share decreased slightly to 11.7% from 11.9% last month.

- Starworld's market share was increased slightly by 2bps sequentially to 9.6%

- Galaxy and it's flagship property gained share in Junket RC. VIP share creeped up for Starworld and was flat for Galaxy while Mass share decreased for both.

MGM's share decreased by 155bps to 6.5%, this is the property's second lowest share month since March 09.

- MGM's share loss can be attributed to a 1.94% sequential decrease in VIP share to 6.3%. Mass share decreased 40 bps to 7.2%. We can't imagine that Encore is doing them any favors... nor is SJM's aggressive share grab.

Slot market commentary

- Slot win grew 28.5% y-o-y to $82MM.

- LVS's slot win grew across all 3 properties by 7% y-o-y to $23MM.

- Wynn slot revenues increased by 3% y-o-y to $15MM.

- Melco's slot win grew 139% y-o-y.

- MGM's slot win grew 35% y-o-y to $8MM.

- SJM's slot win grew 29% to $15MM.

- Galaxy's slot win grew 15% to $2MM.