“A man’s got to have a code”

-Omar (the Wire) and The Hound (Game of Thrones)

My faith in decency and humanism was pleasantly reanimated recently.

I had a leak somewhere in my yard that was causing water to continuously pool. My first thought was that it was a busted line in the sprinkler system so I called Joe the Sprinkler Guy. After describing it to him he didn’t think it was the sprinkler system (he thought it was a leak in the water main) but volunteered to come down and take a look. Sure enough, it wasn’t the sprinkler system and when I offered to give him some $$ for 2-3 hrs of involvement he politely refused …. Not that kind of faux refusal where you can tell they really want to take it but a genuine, “dude, no problem … this is how I operate” refusal.

So, the city guys came out then the town subcontractor came out and went out of his way to “ensure” that the leak was in the service line (i.e. the part of the water line the town is responsible for) not in the feed line to the house (where it actually was).

Now, none of these guys are 1%’ers (or even top 50%’ers) and they had no ulterior motivation for their decisions beyond basic altruism. In the end, I didn’t have to pay the $5K+ it costs to dig a giant hole in my yard and find/fix the leak.

Anyway, the message here has nothing to do with finance.

But on a summer Friday with equities at all-time highs and the biggest white collar worry for many being whether the 10Y will trade up or down 2 bps and what that may or may not mean in terms of the global growth outlook or policy trajectory, it’s worth remembering that it doesn’t cost anything to be kind.

Unlike theoretical musings about “neutral interest rates” or spurious Fed Minutes tea-leafing, magnanimity has an immediate and tangible impact on real people’s lives and paying selflessness and humanism forward networks out nonlinearly.

Find a way to pay it forward this weekend. “A man’s got to have a code”…. and not just when it’s convenient and the sun is shining.

Back to the Global Macro Grind…

Since it’s Friday and we’re striking an optimistic tone, here’s your bullish thesis redux:

Policy pivots backstop financial asset long enough for the U.S. to traverse the steepest comps of the cycle. A trade truce subsequently takes the handoff and helps accelerate growth for a cycle that was primed for inflection anyway. That brings us to the election where the Fed will be reluctant to raise or lower rates (even if things are heating up) while China initiates a fresh round of kitchen-sink stimulus as Xi looks to cultivate a ‘king maker’ economy ahead of the 100Y anniversary of the communist party while further cementing his imperial stronghold.

In the background, the populist zeitgeist continues to percolate with policy makers, increasingly fretful of the capacity of central banks still mired in ZIRP/NIRP to forestall another recession and heartened by the “American Exceptionalism” experience of 2018 whereby stimulative fiscal policy propelled teflon growth and a positive divergence in U.S. Growth in the face of synchronized ex-U.S. slowdown, the siren song of MMT (or some variant) garners increasingly tangible support, globally. Fiscal policy supplants still active monetary policy as the primary stimulus lever and the present cycle transubstantiates into the Peter Pan Expansion that never grows old.

Or the Fed wastes its ammo on insurance cuts, Trump’s descension into direct FX intervention goes spectacularly awry, entrenched political discord and growing inequality further foment populist fervor, an acceleration in protectionist and trade policy escalations and the terminal end of the long-term debt cycle all conspire to deep six both the economy and financial assets.

And remember, it’s definitely, absolutely, completely binary – either we’re Australia (27 year expansion) or it’s human sacrifice, dogs and cats living together, scorched earth hysteria …. Everyone knows that no one hawks investment research or accumulates master-of-the-universe AUM with a “things will mostly just kind of be okay with some small oscillations above/below trend growth so just hug beta and don’t worry too much” marketing.

Anyway, today we’re purveyors of Panglossian narratives, so let us bask in the warm glow of sanguinity emanating from the medium-term outlook for domestic housing:

We hosted our 3Q19 Housing Themes call yesterday. Below are a selection of dynamics that continue to define the larger, housing cycle backdrop. If you’d like access to the replay and full presentation, ping .

HH Formation | Is The Ball (finally) Underwater?: HH Formation has been growing at a premium to new construction in recent years, raising concerns around a real and growing construction deficit. There is, however, one significant caveat. A large portion of Household Formation growth has been in the form of shared households – the so called “basement dwelling” phenomenon.

From 2007 to 2018 the number of shared households increased by 5.1mn, driving its share of total households up by +250bps, from 17.0% to 19.5%.

In other words, what ostensibly looked like excess demand and a ball under water catalyst for new construction volumes was mostly illusory and a function of the significant rise in shared household formation. The good news is that the rate of shared household formation has slowed meaningfully the last few years (from 2013-2018, the change in shared households as a percent of total households has only been 0.5% … which compares to a share increase of 2% from 2007-2013).

In other, other words, what was an illusory construction deficit in now transitioning to an actual construction deficit.

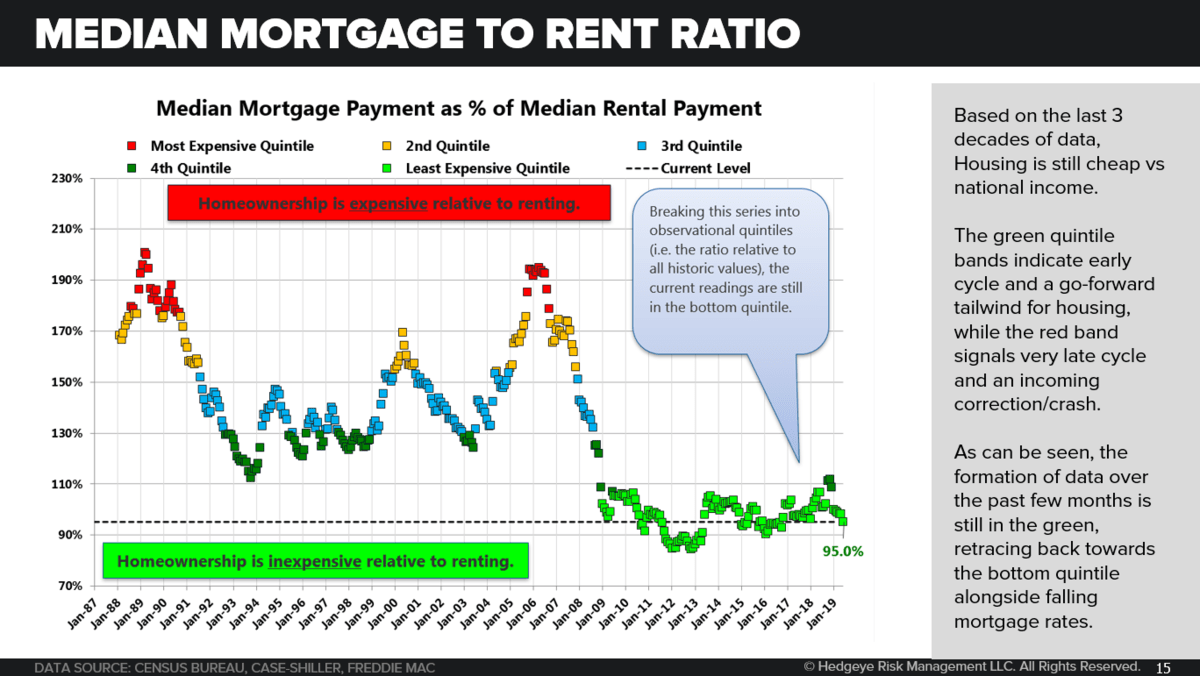

Affordability | Psst .. hey, down here: You may find the chart below remarkable given the headline zeitgeist around the lack of affordable housing or the capacity of many buyers to purchase. You have to live somewhere and all those people who are choosing to live somewhere (HH formation trends above) have the singular choice of purchasing or renting – so any purchase decision becomes a game of relatives with the cost of owning defined relative to income or defined relative to the alternative (renting).

Historically, mortgage payments have peaked around 2x rent payments nationally and troughed near parity, which is where they stand today. In fact, inclusive of the latest move lower in rates, the median mortgage payment sits at 95% of the median rent payment. In other words, the cost to own relative to the cost to rent has literally not been better on a historical basis. From a home price perspective, holding income and interest rates constant, mean reversion to the long-term average ratio of 132% would imply home price upside of 38%.

The ratio of median mortgage payment to median income looks similar – i.e. it also remains in the lowest quintile on a historical basis.

Demographics | Millennial Mojo: Demographics are glacial and we’ve profiled this chart before but you can’t effectively characterize the medium-to-longer term outlook without accounting for population dynamics across housing’s primary consumption cohort. Recall that the average age of first time homebuyers currently is 32-33 years old, while the average age of first time renters is 26-27 years old. As the chart below shows, there are far more 26-29 year olds than 32-33 year olds today (roughly half a million more, each year), meaning that there will be a significant, progressive increase in demand from first time homebuyers over the next five years.

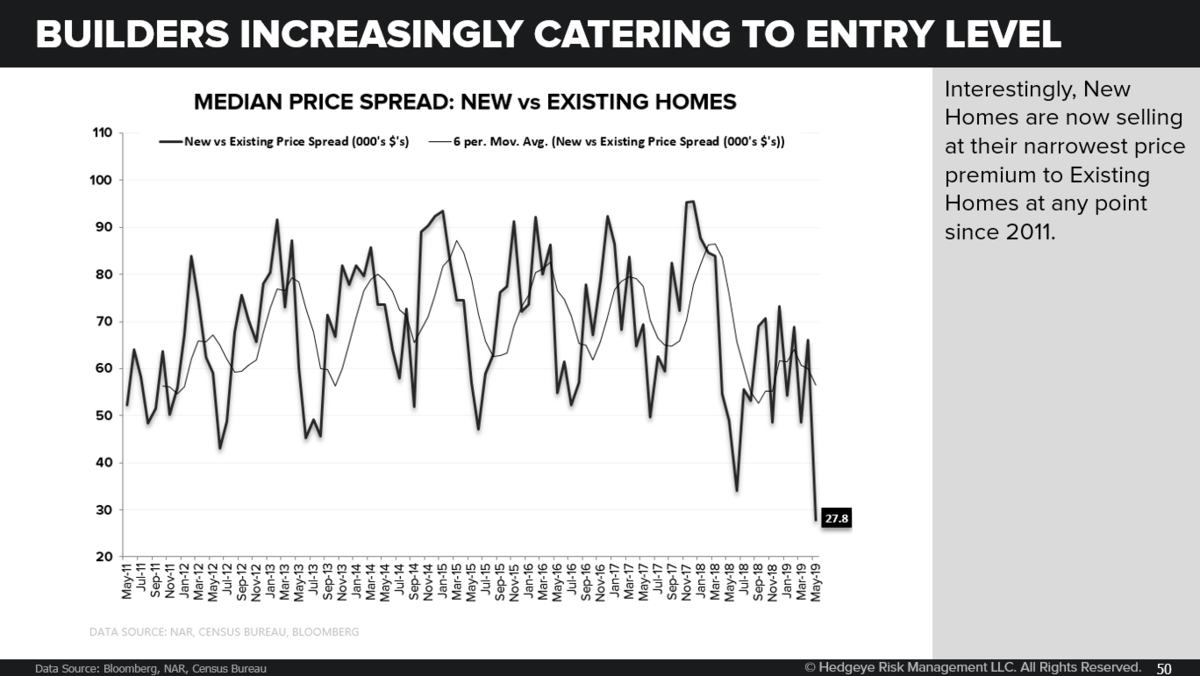

Collapsing … But the Good Kind: The spread in prices between new and existing homes has collapsed to its lowest level of the cycle in recent months. This reflects, in large part, the collective shift by builders towards more entry level construction. All else equal a tightening spread should favor purchase demand in the new market.

A quadfecta of defining secular factors seems about right for a summer Friday, so we’ll leave it there.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 1.94-2.15% (bearish)

SPX 2 (bullish)

RUT 1 (bearish)

Utilities (XLU) 59.21-61.66 (bullish)

REITS (VNQ) 86.99-91.67 (bullish)

Financials (XLF) 27.08-28.34 (bearish)

VIX 12.02-16.37 (neutral)

USD 95.32-97.40 (neutral)

Oil (WTI) 55.71-60.92 (bearish)

Gold 1 (bullish)

To curation, contextualization and quantification ….. the man/woman code of macro process.

Have a great weekend,

Christian B. Drake

U.S. Macro & Housing analyst