R3: REQUIRED RETAIL READING

April 28, 2010

TODAY’S CALL OUT

Whether its coincidental or not, just one day after Wal-Mart lost a critical court decision in its gender bias case that will allow the trial to proceed under “class action” status, an article appears in the Wall Street Journal focusing on smaller format growth for the world’s largest retailer. While this may be eye catching to some, it’s worth taking a few minutes to dig into the Journal’s speculation. Keep in mind that ever since Wal-Mart began operating the Neighborhood Market concept in 1998, there has been continuous speculation that Wal-Mart would eventually roll out the grocery-only format. Fast forward 12 years and there now 150+ units and the company has never addressed the concept as anything more than a test.

The bigger story here is not whether or not Wal-Mart may have something up its sleeve for unveiling come June at the annual meeting or perhaps in October at its analyst day. If anything is announced, even if it’s a concept aimed squarely at the dollar stores (which is doubtful given the sheer amount of boxes Wal-Mart would need to roll out to move the needle), it will likely take years of testing before anything comes to realistic fruition. However, given Wal-Mart’s strength in consumables retailing and price leadership, it would not be inconceivable to expect something centered around this core merchandising capability. Therefore, while it’s easy for us to make light of the Journal’s highly speculative and fluffy article this morning about future growth in new formats, it’s also worth keeping a close eye on any clues that may arise from such initiatives. This could have meaningful implications for companies like SWY, KR, SVU, FDO, and DG at some point. The last time we went through this exercise in a meaningful way, the Supercenter went from test to dominance in a decade and put the supermarkets in a position of permanent defense. For now, the “tell” signs are still unclear.

Eric Levine

Director

LEVINE’S LOW DOWN

- While some may still think of Under Armour as a company that remains heavily reliant on its first product, “compression”, the results paint a different picture. As the company continues to grow its loose and fitted apparel, footwear, and accessories, compression is shrinking as a percentage of the product mix. In 1Q, two thirds of apparel sales were non-compression.

- In a sign that soft-home continues to improve, Iconix noted strength with the company’s direct-to-retail brand, Charisma. Sales of Charisma, which is sold exclusively at Costco more than doubled year over year. Adding to this growth is additional “pallet” space, which was visible during a recent visit to a local club.

- Office Depot noted that while the Florida market continues to lag the overall company averages for growth, it is showing signs of improvement. On the flip side, California is a laggard and “remains a major concern”. Management noted that weakness was consistent in both its consumer and business-direct divisions.

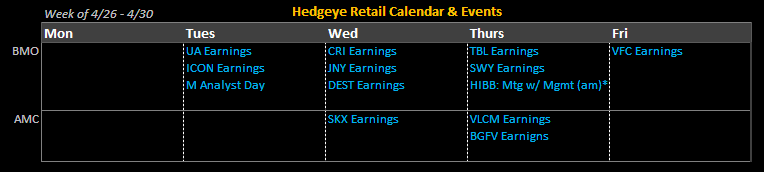

HEDGEYE CALENDAR

MORNING NEWS

Footwear Companies Issue Last Chance Warning to Brazilian Leather Suppliers - Footwear giants Adidas, Clarks, Nike and Timberland have issued a last-chance warning to Brazilian leather suppliers, saying that they will drop suppliers which use cattle farms which are not registered with the domestic government by July. <drapersonline.com>

Spanish Optimism in Footwear Despite Economic Crisis - A report published by the INESCOP technological center confirmed that in Spain 83.1% of businessmen in the footwear sector expect sales to increase or remian stable during 2010. The study carried out amongst 374 companies reflects the fact that there is most confidence in the development of foreign markets. Another piece of interesting data in the survey was that 78% of the participants thought that factory prices would remain the same during 2010 compared to 19.1% who predicted rising prices. <fashionnetasia.com>

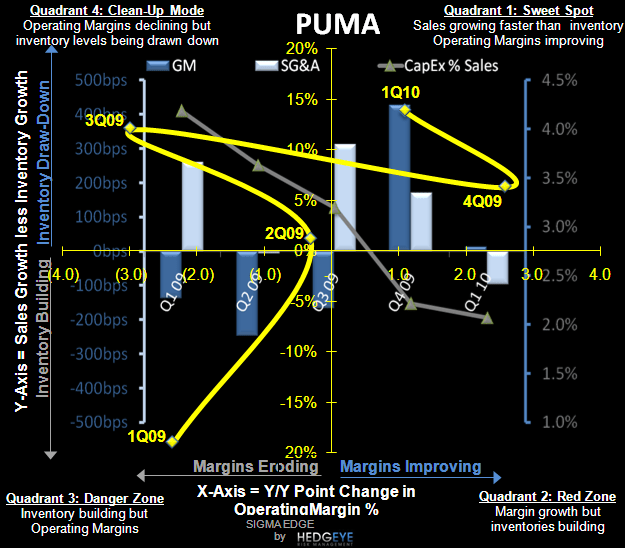

Puma Reports Strong Earnings - Puma AG expects 2010 full-year pre-tax profit to increase by at least 70 percent on an estimated low to mid single-digit sales gain as a cost reduction program and an uptick in orders are expected to work in the company’s favor. “We had a good start into the new year from a bottom line perspective which highlights the effectiveness of our comprehensive restructuring and reengineering efforts,” stated Jochen Zeitz, Puma’s chief executive officer. “We are now looking forward to the upcoming Word Cup and to a successful integration of our newly acquired Cobra Golf business.” <wwd.com/business-news>

US, India, WTO - The U.S. called on India Tuesday to list which export subsidies it would scrap on a range of textiles and apparel products found by the World Trade Organization to be ineligible because they have reached a “competitive” level of world market share. During a session of the WTO’s committee on subsidies, the U.S. asked India to identify the subsidy programs that would be phased out over eight years, trade officials said. The U.S. also expressed concerns about recent reports of new subsidy programs the Indian government is providing to its exporters in the sector. <wwd.com/business-news>

Macy's Upped Guidance at Investor Day - Macy’s Inc. has elevated its outlook for sales and earnings this year and will retrain 100,000 selling associates this summer to help reach its goals. “We have never trained 100,000 people before. This will be a big subject for us,” Terry Lundgren, Macy’s chairman. Earlier in the day, the $23.5 bn, 850-unit Macy’s forecast same-store sales for fiscal 2010 to grow 3 to 3.5 percent, compared with previous guidance of 1 percent to 2 percent. Earnings per diluted share for fiscal 2010 are now projected at $1.75 to $1.80, compared with previous guidance of $1.55 to $1.60. Aside from retraining sales associates, Macy’s expects momentum from the My Macy’s field organization, enabling the chain to get a better read on what consumers want and don’t want at each store, multichannel integrations and exclusive merchandise. The department store is also stepping up efforts to cater to younger demographics. “We don’t discount any area where we are looking for opportunities but definitely in the young area…there is an opportunity,” said Timothy Adams, chief private brand officer. <wwd.com/business-news>

Saks Works with Young Labels - Saks commissioned six youngish labels, including Doo.Ri, Aquilano.Rimondi, Christian Cota, Erdem, Marios Schwab and Gurung. Each designer conceived three new styles — except for Tommaso Aquilano and Roberto Rimondi, who created two dresses — that range from $700 (Erdem) to $7,059 (Aquilano.Rimondi) and will be available in a run of sizes at Saks’ New York flagship, with 10 percent of sales going to the Whitney Museum of American Art, another New York bastion of creative patronage. An in-store party will take place Thursday night to celebrate the dresses and their designers, all of whom, aside from Schwab, whose schedule was compromised by volcanic ash, will be there to toast Saks and hopefully sell some clothes. <wwd.com/retail-news>

Fortune Brands Raises 2010 Estimate - Fortune Brands, Inc. raised the low end of its 2010 earnings estimate Tuesday citing first-quarter results that are substantially higher than the year-ago quarter. The company said its home products and distilled spirits brands drove the growth, but that sales at its Acushnet golf unit also exceeded expectations. <sportsonesource.com>

UPS’ Package Volume, Revenue and Income All Increase - UPS today reported a 2.7% rise in average daily package volume for the first quarter versus a year ago, a 7.2% jump in revenue and a 32.9% increase in net earnings. <internetretailer.com>

Kohl's Extens Elle Line into Home Décor - Lagardère Active and Kohl's have entered into a multi-year licensing deal to expand the retailer's Elle-branded lifestyle products into a range of home décor, inspired by its sister publication Elle Decor. The exclusive Elle Decor range for Kohl's will feature home and domestic products, including decorative pillows, frames, accent items, candles and holders and small furnishings. The line will retail from $9.99 to $149.99 and be available in 350 doors and Kohls.com in September.