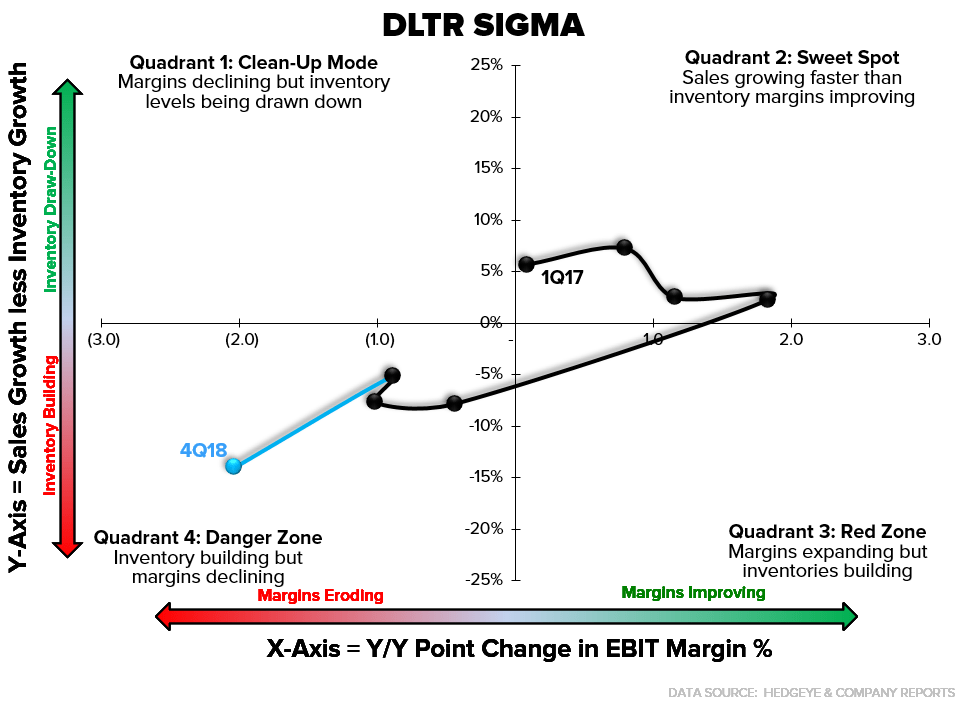

I think we’re in good shape Long side with Dollar Tree on Thursday. We’re at $1.18 vs the Street at $1.14 – keeping in mind that for the quarter the Street was at $1.30 before the company tempered expectations (to $1.05-$1.15), due to moderated comps, announced higher costs associated with store remodels, moving corporate HQ to Chesapeake, tests to ‘break the buck’ and baked in early receipts associated with 25% tariffs (one of the few companies to bake that into guidance). We’re roughly in line with the Street’s comp expectations. While on a stand-alone basis, I’ll be surprised to see anything come out of this print that will derail the bull thesis that breaking the dollar price point at Dollar Tree can add $2-3 per share over a TAIL duration. The biggest risk there is that management tries the buck-break as a token half-baked gesture to shut people like me up – which would otherwise neuter any real reason to own the stock. Though Starboard has sold some of its stock, as of the latest filing it still holds a 4.2% position, and I think that selling out entirely (and so quickly) poses ‘short-timer’ reputational risk that Starboard doesn’t want to invite into the equation. It’s still holding management’s hand as it relates to getting this done – in size – something that will accelerate as the sourcing organizations for the two concepts are ‘pseudo merged’ this summer. I think that comp expectations for Family Dollar of 1% are especially grounded as they bake in very little positive impact from store remodels – something that should provide a comp tailwind starting later this year. So on a quality of earnings basis, let’s make no mistake – this will be a lousy quarter. We’re looking at growth in top line of 4.5%, flattish Gross Profit, and EBIT down MSD%. Definitely a disconnect from the 10.9x EBITDA multiple (though DG – which has far less optionality, trades at 12.3x). But for a defendable late cycle (and Quad 4) name like DLTR with an executable call option for fixing Family Dollar and breaking the buck – each of which are worth $2-3 ps over a TAIL duration – I’m comfortable with the valuation and our Long positioning based on what I see today.