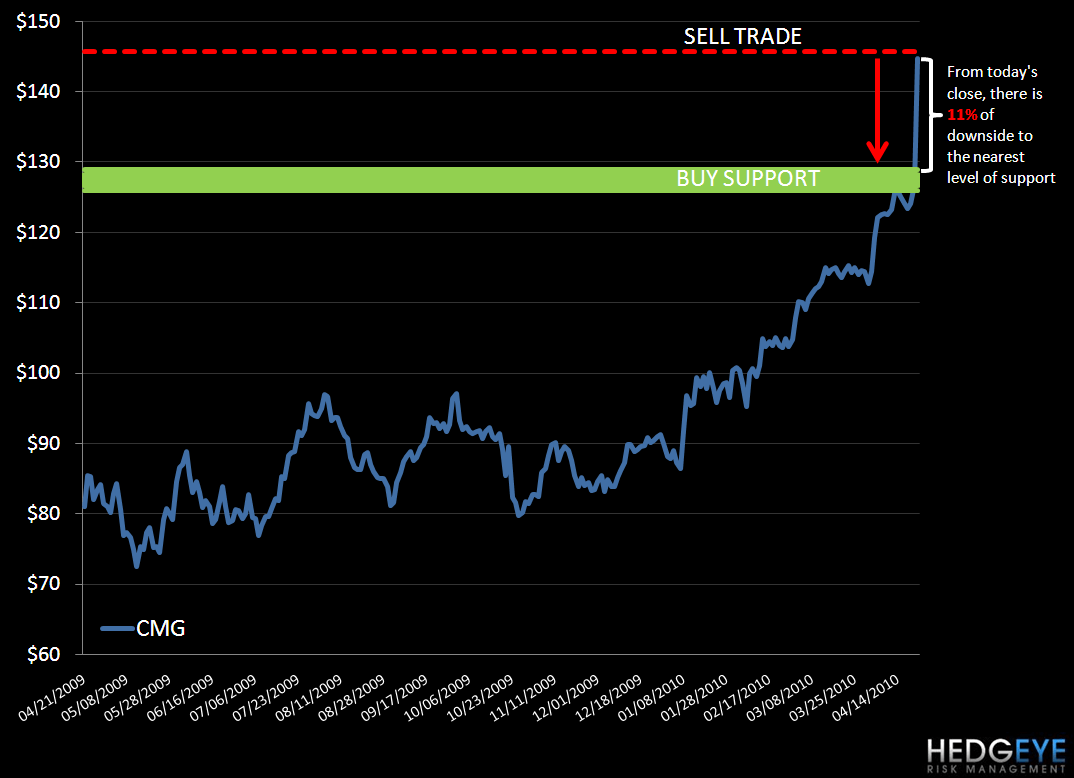

Keith just shorted CMG in the portfolio. Read on for his quantitative levels and a note outlining my thoughts on the name.

The chart below shows Keith's quantitative view on CMG at its closing price.

Chipotle joined the party after the close yesterday. The outlook for the company is strong and price action is reflecting that. Longer term, there are many factors to consider.

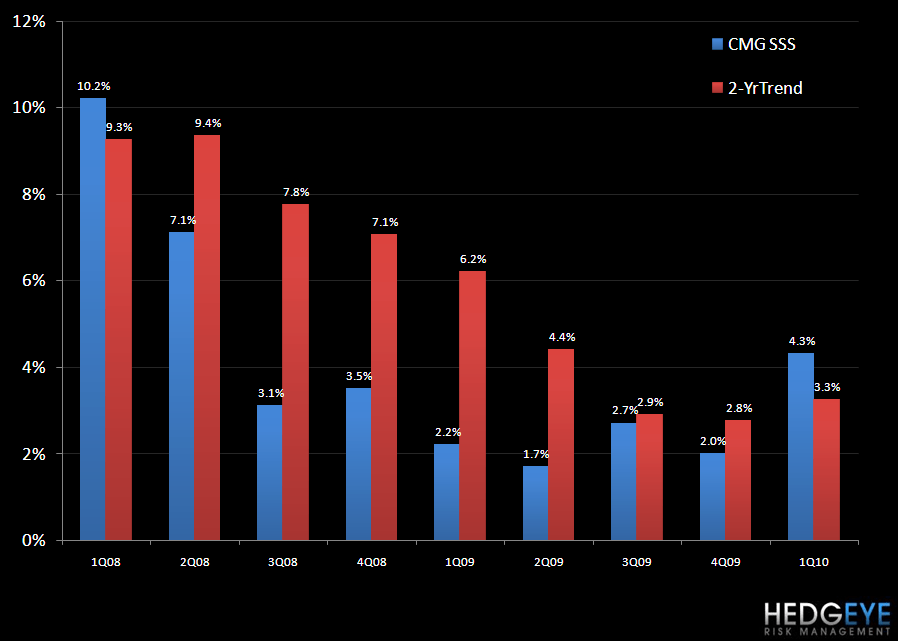

Yesterday’s earnings were, as is the standard this quarter, above expectations for Chipotle. The comparable sales increase for 1Q of +4.3% was mainly driven by traffic; there has been no price taken in the past twelve months. Looking at the top-line, the outlook is strong. On a year-over-year basis, the next few quarters should not be difficult for sales and management said as much on the earnings call, raising their guidance for comparable store sales for the year, “based on improved traffic trends, we’re raising our comp guidance from flat to an expected comp increase of mid single-digits for the full year.”

What will really be interesting will be how margins play out going forward. Specifically, regarding commodity inflation, management stated that inflation outlook for the year is relatively benign and the company only has a few small items contracted for the remainder of the year such as rice, soy oil, corn, and tortillas. Historically the cheese has been locked in but, in line with the company’s high standards for ingredients, it is now moving supply to more pasture-raised dairy. The spot market in cheese was also, to management, “more attractive”. Judging by data from the Bureau of Labor Statistics, the outlook for PPI index for cheese is less-than-benign. At current levels, year-over-year inflation in PPI for “Natural, processed, and imitation cheese” would be 7.4% year-over-year, on average, over the next six months. The move by CMG to buy on the spot market increases the potential for quarter-to-quarter volatility.

In terms of the interaction between grain prices and margins, the chart below shows Restaurant Operating Margins, the CRB Grains Futures Sub-Index, and the CRB Livestock Futures Sub Index. It is clear that the deflationary period of late 2008 and 2009 has helped Chipotle to achieve a higher level of operating margin. In the past quarter, the uptick in sales clearly aided leverage over fixed costs. Whether the company can prudently manage costs in the inflationary periods that we believe are ahead, will be a highly pertinent factor in the intermediate term.

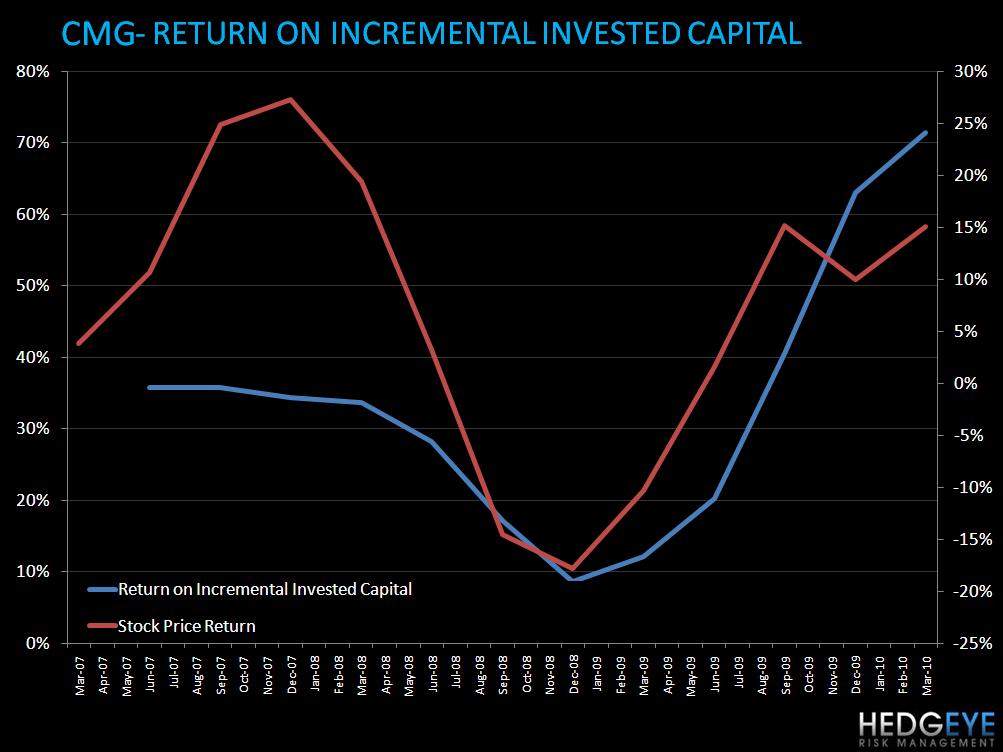

In terms of Return on Incremental Invested Capital, Chipotle is at elevated levels. As they continue into new markets, geographies, and different types of stores, it will also be important to monitor this metric.

NOTES FROM THE CMG 1Q10 EARNINGS CALL:

Proud that during the toughest times, company has maintained standards and service. As the economy improves, more people visiting Chipotle

- First European restaurant is opening in London

- Found good local ingredients

- Taking a fresh look at many aspects of the brand

New advertising

- Pointing out where CMG’s food comes from

- High quality, building awareness will build loyalty

One area of focus is the team

- High performing people culture

- Difficult to articulate but clear that the culture is a factor in driving sales, margins, earnings

- Hiring elite managers and providing incentives for managers to perform and reach “restauranteur” level

- Helping managers understand their role in the overall vision in changing the way people think about fast food

- Special people culture and people are helping the company achieve the goal

New units

- 700k average development cost for 5 new untis this quarter

- They are performing well initially

- On par with traditional new restaurants despite lower opening and investment costs

- New “A” model units have appeal for CMG

- Same experience

- Lower costs

“A” model

- Providing the best customer experience possible

- Growing CMG responsibly

- Increasing shareholder value

1Q results

- Tough consumer environment is improving somewhat

- Efforts have paid off, new and existing customers coming back more frequently

- Unemployment still high, cautious for 2010

- We won’t stray from strategy

- People

- Quality

- Growing

- Did all this while strengthening business model

Highlights for quarter

- Revenue increased 15.6% to $409.7m

- Diluted EPS of $1.19 (vs $0.96 est)

- Comp store sales increased 4.3%

- Restaurant level operating margin was 26.1%

- Increase of 260 bps

- Labor efficiencies and comps drove margin expansion

- Food costs dropped 80 bps

- Rice, avocados, cheese

- Net income was $37.8 million, increase of 49.1%

- Diluted earnings per share was $1.19, increase of 52.6%

- Other operating costs decreased

- Lower promotional and insurance expenses

- G&A declined due in part to increase in stock based comp

- Opening 20 new restaurants in quarter

Outlook

- Raising guidance for comps from flat to up mid-single digit

- 2H food inflation

- Increased commodity costs and consumer demand

- Little or no labor leverage going further

- Marketing at 1.8% for the full year

- No G&A leverage for the rest of 2010

- Holding conference…22m for 2010

- Opening 120-130 new units in 2010. 25% of those will be “A” models

- Better positioned than ever to add to shareholder value

Q&A

Q: Store productivity …thoughput in busier markets…can you update us on throughput?

A: We took our eye off this ball over the past couple of years. Throughput fell off coming into the recession. TCs were lower. Especially at peak hours, less business customers at lunch. They fell more than they should have, though. Over the past couple of years we’ve scheduled better, labor-wise.

Q: Can you talk about comps through quarter and this present quarter so far?

A: In February we were starting to see momentum building in traffic but weather hit that trend in traffic turning. We’re cautious with guidance because this is a new found trend, unemployment is still high, and consumer confidence has improved but not that much. What we saw in March has continued into April.

Once weather is bad we get a couple of over performance for a couple of days when it clears up so we don’t think weather was overly material.

Q: Will commodity inflation in 2H make you consider taking pricing?

A: Seems manageable based on what we know today. Not anticipating taking any price. Seeing food inflation in low single digit range. For the year, wouldn’t expect menu price increases. If things change, we can, but won’t rush.

Q: Growth outlook?

A: in terms of development outlook, two years ago, 70% of restaurants were new developments. Last year it fell off and now it’s around a third. No pick up in new developments yet. There is a substantial lead time. The “A” model strategy tends to go into tier 2 locations and existing real estate. We’re feeling positive about the “A” model strategy. Looking to find as many good locations as we can in 2011 and beyond. This year after the 3Q release we’ll have more concrete details on 2011 unit growth.

Q: Anything in human resources that would make you hesitate in the growth? Or is it real estate?

A: HR is not a problem. We have a good ratio of leaders to stores. Restauranteur growth has been steady.

Q: What kind of competition are you seeing in premium convenient segment and where are you taking market from?

A: It seems like all the news has been positive recently. Seems like consumer is out spending again. We did the best we could while consumers were more timid, and made sure they had the best experience possible.

Q: London team set up?

A: It will be consistent with how it was done in Toronto. Restaurant employees are the only people working there…in London there will be a restauranteur opening the restaurant. There will be two other restauranteurs at the same level that will help with sourcing, hiring, training. That’s unusual but given the success of Toronto, we feel that it is the way forward in London. Germany and France are on longer term radar screen. Sending more talent to London initially. We think it will be easier to find natural food in Europe – there is no RBGH diary in Europe, whereas in the US we have to look for food with integrity.

Sourcing…everything will be cooked from scratch in that restaurant. Going to be able to buy from small suppliers if needed.

The design in London was approached as a chance to do something new – quite like the new ones in NYC.

Q: Clarify marking spend and let us know how broad it will be. How many markets will use radio?

A: Rolling out in 30 major markets. About half of those will have a strong campaign. Marking came in at 1.1% for quarter because new marketing campaign is being rolled out now. Should see marketing budget at 1.75% for year. Marketing now is radio, billboards…radio just started so don’t know what the effect is as yet. Marketing is designed to highlight food with integrity but making message clearer to raise awareness of food with awareness and taste.

Q: Kids’ menu?

A: rolled out in some markets…plan on rolling out the rest of the country throughout the year. June 1st will see another tranche. The teams need to be trained adequately. 2% to 3% of transactions are for kids in the markets so far, without any marketing so far, it has ticked up. Kids menu is priced slightly higher.

Q: Is some of that business incremental?

A: That’s tricky to see right now.

Q: What is your read on restaurant margin differential between “A” model and traditional?

A: It’s really early, we don’t know what the difference would be. If you’re talking about comparable volume, they have opened at typical volume. IF that continues, “A” models will be higher for sure. Too early to tell at this point. Sometime next year we’ll being to open “A” models in new and developing markets. We don’t like new market margins for traditional units. We anticipate “A” models performing better in this respect in new and developing markets.

Q: How do we stand on development of the new units? Backend weighted? Can you tell us where the 25% of “A” models in existing markets will be going in?

A: 120 to 130 this year. Heavily weighted towards 2H. “A” models will be opening throughout that time. 4 next quarter and 12 in the next, 8 in the next, perhaps. They’re going into proven markets…where we’ve been for a long time. Most markets are proven markets. Denver, DC, Dallas, Houston, Chicago, Phoenix…reduced risk of not having success.

Q: Marketing expense…1.8% of sales is for full year…is that evenly going to be expense now for quarters or did 2Q have a few weeks where it wasn’t jacked up?

A: Can’t commit to it being even for the remainder. Remaining flexible. If it were even it would be around 2%.

Q: Average Check?

A: Check was stable. It was perhaps slightly up. Nothing material. Driven by the group size being a little bigger. More group sales, more fax orders, more online. Generally higher check.

Q: Marketing…a year ago the new menu test…is any of the new advertising spend aimed towards educating the guest or is that for the restauranteurs and employees to do now?

A: There are aspects we like, the kids meal is a success in markets so far. Trying to organize the markets in different ways.

Q: Commodity – what was deflation in 1Q? What items are you seeing moving up? What do you have contracted for the year?

A: 80 bps deflation, net. Rice contracted through three quarters, soy, corn, tortillas for full year. That’s it. Not able to lock in much of ingredients. Cheese has been historically locked but we’re changing that, moving towards pasture raised dairy. Spot market was more attractive for cheese also.

Q: Are the stores you opening in the downturn ramping? Comment geographically?

A: comp is broadbased. Only spot that was lagging a bit was Texas, who entered the recession late. Also returning to the comp trends that we saw before recession – new restaurants are comping well and older markets are positive. Comp guidance assumes no menu price increase.

Howard Penney

Managing Director