Starbucks continues to surprise to the upside. The rate of improvement will slow, but margin growth should continue to materialize from here.

Yesterday, MCD reported stronger-than-expected 1Q10 earnings and the best quarterly U.S. restaurant level margin in nearly 16 years. Following those results, I posted MCD’s stock chart, which showed it trading at an all-time high and highlighted that there seems to be some investor concern about where the stock and margins go from here. After the close yesterday, SBUX followed up with another quarter of crazy good numbers. With SBUX’s share price more than doubling in the last year alone and the company reporting record 2Q operating margins in both the U.S. and internationally, my first inclination was to ask the same question about SBUX: where to from here? Call me gullible, but I seem to believe management when it says the “best days are ahead” and that the U.S. business “has not seen its peak.” Apparently, I am not alone as the stock is up 6% today, in contrast to MCD’s muted response yesterday. To be clear, SBUX’s rate of improvement will have to slow (full disclosure: I feared this two quarters ago), but I am now convinced margin growth will continue to materialize.

SBUX is not MCD…

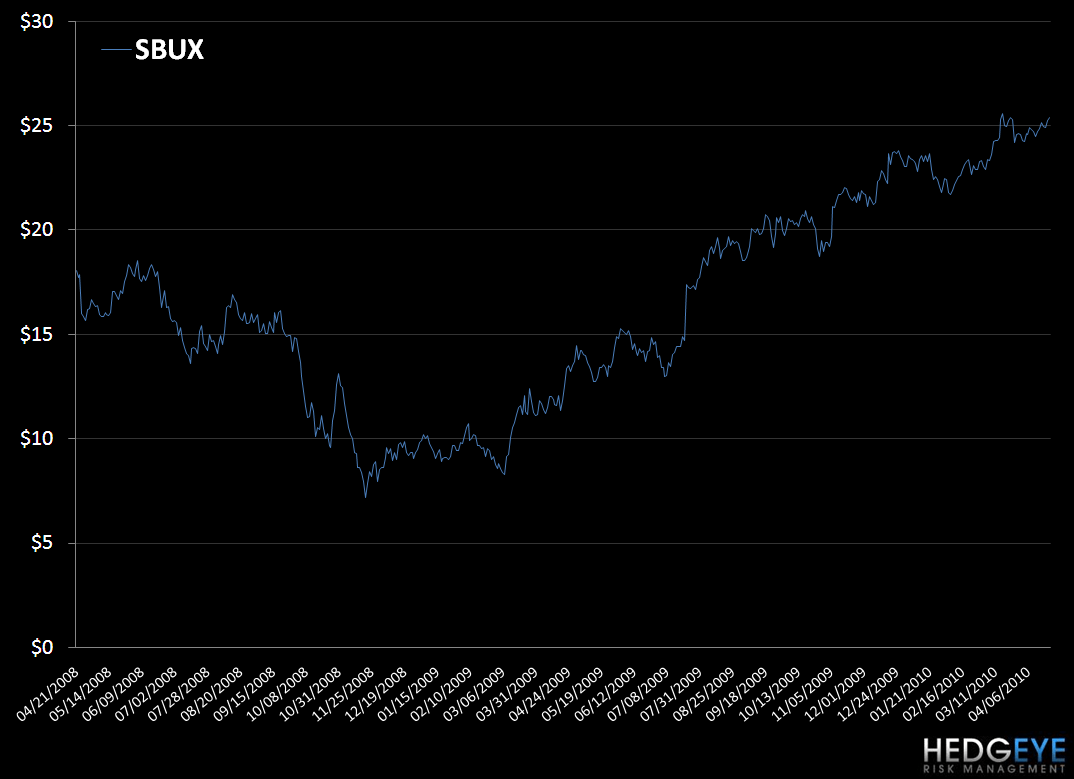

To start, SBUX is not trading at an all-time high; though it has had an impressive 275% move higher since its recent November 2008 low. MCD is consistent. I was concerned with the company’s decision to add the McCafe beverage platform because I feared the company would lose sight of its core business. With March same-store sales up 4.2% in the U.S., the company seems to be charging forward with few issues. The company will continue to refine its business, allowing it to better execute, but I question what the next layer of growth will be for MCD, particularly in the U.S. I do not have the same concerns for SBUX.

SBUX seems to have a lot of momentum right now when it comes to potential sales layers. Additionally, these new avenues of growth will leverage the company’s existing retail store base but also extend beyond it.

Within the retail store base:

- Company transformation – the back-to-basics strategy has enabled the company to improve its customer satisfaction metrics, which has been directly correlated to the company’s improved traffic – Sharing best practices globally

- My Starbuck Rewards – the recently launched rewards program is driving increased frequency with card reloads up 45% YOY in the second quarter

- U.S. VIA – management would not break out VIA’s contribution to the 7% same-store sales growth in the U.S., but did say that VIA was an important driver of the 5% increase in average check – VIA is now expected to be slightly positive to profit in FY10 (had said profit neutral)

- International VIA – the product has been rolled out in Canada, the U.K. and most recently, Japan and has exceed management expectations in each segment. VIA will be launched in additional markets throughout the year

- Remodels – over the next 12-18 months, SBUX will begin an “aggressive phase of existing store remodels and refurbishments in the U.S”

Within the CPG channel:

- Management continues to believe that both VIA and SBC have the potential to become billion dollar brands for SBUX

- VIA – the brand’s distribution will be greatly increased to more than 30,000 points of distribution by the end of 3Q10 supported by a nationwide U.S. advertising and marketing campaign, both print and broadcast

- Regarding VIA, management looks “forward to offering new form factors and other innovations in the very near term for all things VIA.” Management was fairly cryptic about what those other form factors could be but it was clear that it is heavily focused on the at-home market. Specifically, management stated, “We’re certainly well aware as the leading specialty coffee brand of what’s going on around single serve and specifically at-home and have had a watchful eye on what Green Mountain and Keurig have been able to do and they’ve done a fantastic job. We’re looking at this in two ways. One, we think that VIA has an interesting opportunity to position itself in a way against what Keurig is doing at home because there’s no waste, there’s no cost of equipment and you can take VIA anywhere. And the quality of the coffee is significantly better and we’re going to have multiple SKUs and form factors that will create a portfolio of product. However, I think the market needs to stay tuned that we have every intention of understanding what single serve can be. And we’re not going to sit back and just watch Green Mountain and Keurig march their way into 20 to 30% household penetration without Starbucks not doing anything. So just stay tuned.”

- Increasing CPG capabilities globally – recently entered the RTD coffee category in Europe and launched Starbucks Double Shot in the U.K. grocery and convenience channels

- SBC – by the end of the year, the company will have expanded SBC points of distribution to 30,000 from 3,000

SBUX’s ability to identify new sales layers has been impressive, but like anything else, execution will be important. Focusing on the core business has been a significant driver of the company’s recent success in the U.S. and it will be necessary to monitor whether SBUX can maintain this focus while executing these new growth initiatives.

Near-term issues: As I stated earlier, SBUX’s rate of improvement will slow in the back half of the year as the company will begin to lap more difficult same-store sales and margin comparison from last year. Based on the company’s full-year margin guidance, margins will continue to improve in the back half of the year but at a moderating pace from 1H10. Keep in mind that margins in the third quarter will be further pressured by the increased investment behind the VIA launch , which will add an incremental $0.05 per share of marketing expense in 2H10 versus 2H09, which will fall primarily in the third quarter. Management stated that 4Q margin should be higher than the 3Q level.

As management indicated on its call yesterday, same-store sales in the U.S. improved through 2Q10 sequentially on a 1-year basis for five quarters and on a 2-year basis for four quarters. Although I am expecting two-year average trends to continue to get better, it will be a lot more difficult for the company to maintain its trend of posting sequentially better numbers on a 1-year basis in the next two quarters. I was surprised that the company was able to post a sequentially better number on a 1-year basis during the second quarter, but investors cannot count on too many more of these surprises. To that end, management’s full-year mid-single-digit comparable store sales growth does not assume that same-store sales come in better than 7% in the back half of the year.

We included Keith McCullough’s risk management TRADE (immediate) and TREND (intermediate) levels in the chart below:

Howard Penney

Managing Director