Each week we provide an update on initial jobless claims because we think it's one of the best leading indicators for the credit-sensitive names we follow and history has shown there to be a very high correlation. The reality, however, is that there has been quite a divergence that has taken place in the last four to five months.

Let's just get this week's data out of the way first. Claims for the most recent week, out this morning, dropped 24k to 456k from 480k (revised down 4k) in the prior week. This caused the rolling 4-week average to actually increase by 3k to 459.5k from 456.8k.

We hate to be the ones to take away the punchbowl, but consider this. As the charts below show, at 456,000, claims are at the same level they were at on 11/28/09 (457,000). In other words, claims have gone nowhere in almost five months. Compare this with the colossal improvement in claims from April 2009 through November 2009. In stark contrast to recent claims trends, the XLF has barreled higher some 17% over the last 4.5 months, with high-beta Financials rising by multiples of this.

While we've been patient in our weekly posts, waiting for claims to resume their downtrend, we think that enough data (20 weeks now) is in to begin to warrant some caution around prospective performance in the XLF. If claims continue to trend sideways at these levels, it will be difficult, and, frankly, unlikely, for Financials to continue to move higher if the backdrop of further employment gains stagnates. Because claims are a leading indicator, we treat them with greater significance than the unemployment rate. We have other reasons to be cautious heading into the seasonal summer doldrums, namely renewed housing concerns. Couple this with the blowout 1Q10 results so far, and layer on the marked increase in consensus expectations around normalized earnings, and it is starting to feel like the Financials are better positioned for correction than further gains. We don't want to be alarmist with this call, but the reality is that it was the inflection in jobless claims that marked the bottom at the March 2009 lows, and claims are now sending us a new signal so it's time to pay attention.

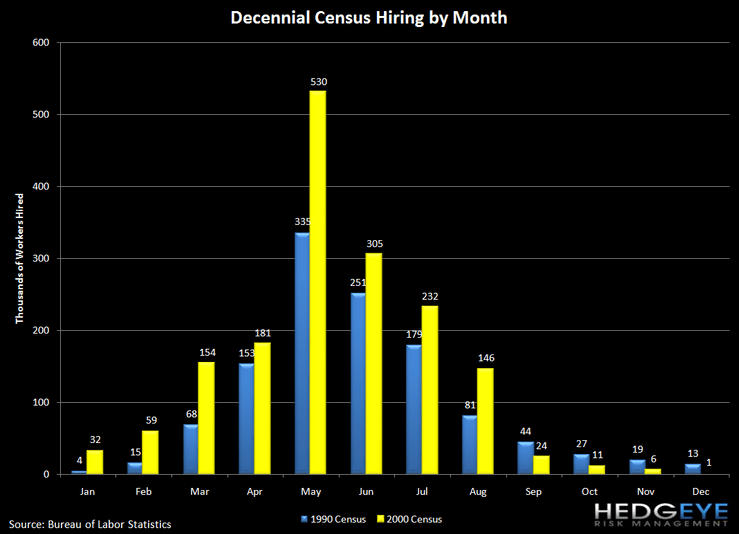

As a final word around the census, we've been bullish on the lift the census would add going into its peak employment months, but we're almost at the point now where it's time to start focusing on the drag it will create on the backside as the peak month of employment, May, is just 8 days away.

The following chart shows the raw claims data.

The following chart shows the census hiring timeline.

Joshua Steiner, CFA

Allison Kaptur