How many restaurant companies have the potential to grow earnings 50% in the next two years?

If I were one of the multiple PE firms shopping around to buy a restaurant company, EAT would be on top of the short list.

(1) National brand in a large category

(2) Underutilized assets

(3) Discount valuation

(4) Global unit growth potential

(5) Strong balance sheet

(6) Stable cash flow

(7) Strong franchise partners

My analogy to a PE company buying EAT is not totally misplaced. First, buying a stock today with a credible (and somewhat proven) plan to double earnings in 5 years with potentially 50% of that growth coming in the first two is not a bad risk reward.

Second, the risks are well known. Brinker and the rest of the industry are lapping severe discounting from last year’s economic turmoil. The good news is the severe discounting is not as needed and the industry is operating in a more “normal” environment. Yes, that makes sales comparisons difficult, but it’s a benefit to margins and cash flow.

The market reaction to earnings today was to sell off the stock. Great, we bought it.

If it goes down tomorrow because someone is concerned about fiscal 4Q10 same-store sales, I’ll buy it again. We are within a six month window where all the bad news is out, and we are now looking down the barrel of potentially the best earnings growth story in the large cap casual dining space.

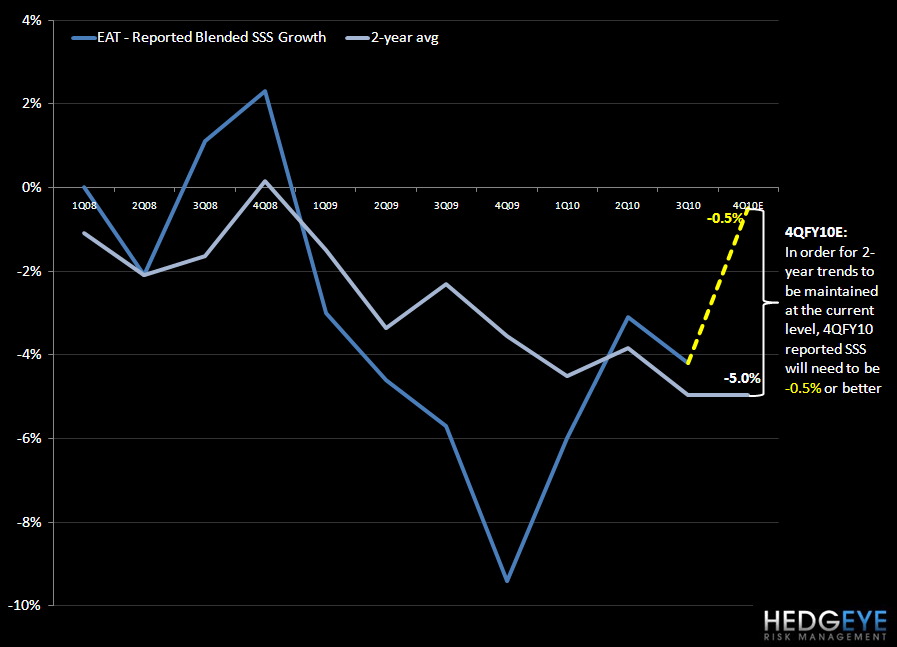

Judging by the dialogue on today’s call, there seems to be a lot of confusion among investors about the timing of implementation for POS, KDS and kitchen retrofits and the subsequent margin benefit. However, management seemed confident about its potential earnings growth in the next two years. EAT’s 5-year target to double EPS by FY15, off of the $1.40-$1.44 base, with 10%-12% EPS growth in FY13-FY15 implies 40% to 50% EPS growth from FY10 to FY12. This two-year target assumes 1% to 2% same-store sales growth, which seems achievable; though it does it rely on sequentially better 2-year trends going forward.

I know things don’t happen in a straight line and there will be bumps in the road, but I want to be a little early on this one. Once it gets going, it’s gone…

With the typical PE firm’s 3-7 year time horizon, the odds are good on this one.

The near-term sales outlook may be choppy but, as I said earlier, negative sentiment will only offer more opportunity for those willing to look past the immediate term.

NOTES FROM THE CALL:

Earnings

- EPS of $0.42 before special items incl OTB

- $0.37 on a continuing basis

Financial takeaways from Analyst Day

- Long-term goal is to double FY2010 EPS pre special items by 2015

- 10%-12% EPS growth for FY2013 through FY15

- In order to double EPS, growth in the next two years must exceed 10%-12%

- Assuming 1%-2% comps

Current FY10 Sales Guidance:

- -1% to -2% incl 53rd week

- 53rd week helped comps by 2%

Margin

- For 500bps improvement:

- 300 bps from kitchen retrofits /POS/KDS

- 200 bps from others

- 100 bps depreciation impact for a net 400 bps impact to margins

- LED lighting and reimage programs also included in 100 bps impact

Cash

- EAT will only continue to invest in incremental capital spending related to kitchen retrofits if it sees resulting margin improvement

- FCF will be invested in business to reduce debt, pay dividends

- Leftover cash will go to share repurchase

G&A

- G&A cost included in discontinued operation

- $3-6m of fees will be received for support services to acquirer to offset support costs associated with OTB (such as centralized accounting and other shared back office costs)

- OTB sales will be $0.03 to $0.05 dilutive to EPS

Expenses

- Lower than normal expenses in 4Q09

- Insurance, property tax, utilities, vacation

- 110 bps favorable impact on margin

Analyst day

- Outlined company’s “Plan to Win”

- During quarter finished rollout of menu transformation

- New items, improved kitchen processes, removed items, changed recipes

Promotions

- Promotional offers are attracting more guests

- EAT’s participation in deals is among the lowest of its peers

- Guest satisfaction has improved since the Analyst Day when it seemed to be softening as changes to the menu were being implemented

Financials

- During 2Q, revenues decreased by 7.8%

- -4.2% decline in SSS, 40 fewer restaurants

- Traffic better than comp, mix worse due to promotional activities

- 5.3% decrease in capacity

- COGs increased 30 bps to 28.5% vs prior year

- 90 bps sequential improvement

- 70bps benefit from commodities

- Offset by margin loss from mix shifts due to promotions and changes at Maggiano’s and Chili’s

- Restaurant operating expense was 54.7% vs 54.1% a year ago

- Labor up due to training for new menu etc.

- Depreciation has decreased due to fewer restaurants and more fully depreciated assets

- G&A decreased by ~$2million per year, 10 bps as % of sales to 4.5%

- G&A for discontinued ops are directly attributable to support costs that are identifiable to the OTB brand. Not included are accounting services and other back office costs. EAT will collect fees that will offset these

- Interest Expense was $1M lower YOY

- Tax rate of 19.7% was lower than 3QFY09 due to resolution of tax positions

- Capex was $32m

- CFFO was $223m

- $182m cash balance

Outlook

- Capex of $84m for fiscal year (unchg)

General

EAT's three businesses are Chili’s, Maggiano’s and Global business development (GBD)

- GBD

- Great growth potential outside the U.S.

- Extending to 425 Chili’s outside the U.S. by 2014

- Maggiano’s

- Gained traction throughout the quarter

- Comps sales +5.2% in March

- Jan and Feb were 3.8% and 3.7% respectively

- Margin improved 200 bps

- KDS/POS testing in Mexico is returning great results

- Chili’s

- Testing initiatives aimed at driving margin

- Rolling out LED lighting

Free Cash Flow

- Short-term debt repayment goals are almost accomplished

- Investment grade rating from S&P

Q&A

Q:

What will the costs be for rolling out new kitchen initiatives?

A:

The initiatives will be rolled out over time, not expecting a big hit to any one quarter, we’ll have more of an idea over the summer.

Q:

For the $0.05 dilution from OTB sale, were you referring to G&A picking up and that being the amount you have to offset with revenue?

A:

No. Some G&A will not be recorded as OTB. There are some proceeds that will be used to buy back shares. After repurchase, net dilution will be 5cents

Q:

How do you see Chili’s navigating the competitive environment? Promotions in July last year, how do we think about promotions versus competitors that did promotions earlier in ’09?

A:

The level of discounting and consumers that are eating on deals is staying strong. There is still a lot of discounting going on.

Q:

In some ways, will it be difficult to figure out how this summer will play out for casual dining?

A:

Yes, it is difficult – the margin play is opportunistic for EAT and we’re balancing all that into plans as we proceed into summer and figure out strategy.

Q:

On share repurchases, will that be an open market repurchase?

A:

Looking into all options, will discuss with the board and decide on a way forward.

Q:

What is ticket time now?

A:

It varies between lunch and dinner…5 minutes is a goal. That will make us far more competitive at lunchtime in particular.

Q:

Talk about the timing of the roll-out, 5 restaurants at the start of 2011FY, by the start, how much of the systems will be POS/KDS operative?

A:

End of this year for POS, early next year for KDS. To finish the retro fits, however, it will take longer, possibly into 2012, 2013.

Q:

Margin improvement timeline?

A:

Margin equipment will come through 2011, 2012, but the full 400 bps will not be realized until 2013.

Q:

Share repurchase?

A:

Not all OTB related, we will have excess cash that we will use for share repurchase. Didn’t receive authorization from board until late in 4Q so haven’t done that yet.

Q:

Commodities will be down for C’10? What do you think for commodities in CY11? Also, how will health insurance legislation affect EAT?

A:

We have gone through a lot of commodity negotiations. We have clarity on those costs out to December (still favorable in all items ex produce through December). 50-60% contracted through December.

Q:

With current levels and outlook, do you have a sense of how they will go in C’11?

A:

Flat from 2010 into 2011 but it’s very difficult to tell. On health insurance, there are still more questions than answers. Most of the requirements won’t take effect until 2014, the couple of things that do (students and pre-existing conditions) are already covered by EAT health insurance.

Q:

Cash balance?

A:

$182m

Q:

On service strategy, can you explain that?

A:

Focused more on team service. It’s a strategy that worked well at Maggiano’s.

Q:

Kitchen retrofit should take 2/3 years. Accelerated depreciation?

A:

As we roll out the equipment, yes, but will be written off over five years.

Q:

What is the lead time for the marketing (fresh pairings)? Is it a couple of weeks or months? Also, sales trends at Maggiano’s being addressed mid week? How are they looking?

A:

We have a national marketing strategy that has media in place. Cost structure benefit comes with that. It’s really about messaging. We’re able to move quickly, it can be done as quick as three or four weeks.

Q:

Promotions…as you switch to fresh pairings, we saw that food costs were down but GM also declined, does this new fresh pairings have enough of an impact that it would have swung to a benefit or is there not that level of margin impact from this promotion?

A:

Biggest issue is the introduction of the menu revolution. The promotion doesn’t have a significant impact on COGs. The difference that we see going forward is from the costs we see going forward rolling out the new menu.

Q:

First question relates to G&A, interest exp guidance. Implied 4Q guidance seems to suggest, ex OTB, that costs are increasing? Are you being conservative or what is going on?

A:

What we might do with our credit facility at the end of the year is still in flux so the interest expense line is difficult to call conservatism. The other two lines, perhaps can be called conservative, but profit sharing initiatives and other variables can move those lines up or down.

Q:

Do these retrofits and margin improvements happen in step or are there different investments or possible hurdles in the way? Do staff adjust quickly in your experience or will it take time for staff to ramp?

A:

POS and KDS are already familiar to most staff. Aloha system already in place in some restaurants. The retro fit is where the big capital dollars come in place. $100k per restaurant. Relatively small investments with pretty quick returns in terms of guest satisfaction and margin performance – 30 to 45 days.

Q:

Advertising…you benefitted from rebalancing, media rates seem to be going up…demand may be a little softer for a while longer, do you expect to have to spend a little more on advertising going forward?

A:

Our media costs are mostly accounted for over the next five months.

Q:

5 minute ticket time is a huge improvement…can you translate that into a comp?

A:

When you put all of the initiatives together, no questions we see an increase in getting guests through, wait times shortened.

Q:

EPS commentary…are we talking about $1.20, $1.24…double FY15 off that number?

A:

Double eps is on $1.40 to $1.44

Q:

What is the comp assumption? 3%-4% longterm?

A:

1%-2% for ’11 and ’12

Q:

How does margin expansion come then?

A:

The initiatives will give us the margin improvements in 2011 and then in 2012 the kitchen benefit will kick in.

Q:

Given that comps came in at low end of the range, did the quarter end softly? There is an industry wide view that things are improving…did Chili’s lag?

A:

We saw acceleration from February to March even on a weather/adjusted basis.

Q:

Maggiano’s numbers by month? March strength continuing into April?

A:

3.8% in January, 3.7% in February, 5.4% in March.

Q:

What does this mean for the corporate spending rebound? Anything that would derail that? Is that something you see as playing out for the remainder of year?

A:

We’re trying to grow the consumer experience? Working on a guest that doesn’t come that often. If we can expand above the banquet/occasion business, we see a lot of growth. Short term we see nothing that would change that.

I would say that business spending is starting to come back. Banquet bookings looking better.

Howard Penney

Managing Director