Best Idea Long thesis firmly in-tact. Revenue prospects are better than ever. Won’t be apparent on the surface of Q1 results – gotta wait til 2Q for acceleration. But expectations have been washed out. Little risk in the upcoming print. We’re facing a low bar with top and bottom-line accelerating as the year progresses.

Customer bankruptcy impact

Gildan provided an update on March 26 ahead of an investment conference and lowered EPS guidance due to the bankruptcy of Heritage Sportswear, the 10th largest supplier in the promotional products industry. Gildan said it expected a $19-23mm charge for the impairment of Heritage’s receivable. On an EPS basis that is a $.09-$.11 impact. Management is including the charge in its adjusted EPS. Gildan confirmed its outlook for revenue in 2019 as it expects the bankruptcy of a distributor to not have an impact on end demand. Gildan expects (as do we) that screen print customers will order from other distributors. The bankruptcy of a distributor should not impact screen print customers as it does the apparel manufacturers.

The following day CFO Rhodri Harries gave a bullish investor presentation at the conference. He said the company is down to about $500mm of spare capacity which is why it will lay out the future capacity plans at the analyst day in the fall. Besides some incremental additions in Honduras it sounds like management is ready to expand outside of its Honduras base, perhaps in Bangladesh. The CFO spent the most time discussing the growth opportunity in private label. He believes the relevant category represents a $1bn TAM for Gildan in the context of a $6-7bn wholesale market. He was bullish on their Amazon business which is growing well with Gildan underwear among the top underwear brands. Rhodri Harries described the overall screen print market as healthy with a good balance between price, cost, and inventory levels although Gildan’s inventory levels could be higher. It would be surprising if the business weakened in Q1 such that management wouldn’t have adjusted guidance when they announced the charge for Heritage Sportswear.

Bankruptcy forecast could be conservative

Last week Gildan filed a counter motion opposing the liquidation of Heritage. Gildan opposed the plan of the liquidator selling its inventory without permission. Gildan had sold to Heritage under consignment. Heritage’s receiver proposes to hold the proceeds from the sale of Gildan inventory separately until an agreement can be made over what is Gildan’s inventory. According to court documents Gildan believes Heritage has $8mm of its inventory and owes it $8mm for inventory already sold. The court documents may not provide the complete picture, but it appears that Gildan could have been conservative when it provided an initial estimate of its exposure to Heritage’s bankruptcy. Investors are likely viewing the Heritage bankruptcy as a non-recurring event, but it appears it will be included in adjusted EPS.

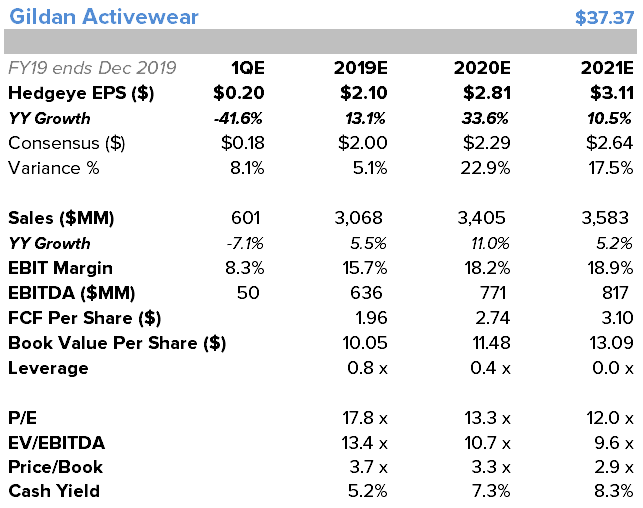

Our model vs. consensus

The Q1 consensus EPS estimate is $.18 while I am two cents higher.

- I am expecting revenue to decline 7% vs. the mid to HSD% guidance and consensus of a 7.4% decline. The decline reflects lapping a distributor restocking period last year and the drawdown of inventories at Walmart for the merchandising transition to the new private label brand. The headwinds will reverse later in the year, but it causes a weak Q1. That’s widely telegraphed.

- I am expecting gross margins to contract 380bps vs. consensus expectations of a 340bps decline. The COGS pressure is from higher cotton and oil costs. Gildan offsets raw material inflation with price increases, but there is a lag in timing as customers’ orders before price increases are still honored at the original prices.

- I’m a little higher on EPS than consensus, because I think SG&A can continue to be down YY due to continued cost savings from the consolidation of divisions last year.

- It's also possible EPS could be slightly above $.18 if the receivable for Heritage is revised down to $16mm from $19-23mm.

Don’t wait for the bears

Bears will have to explain how their financial models do not have the company filling all of its new capacity from RN6 in 2H and in the out years. At the same time management is saying that the company is already down to only $500mm of spare capacity less than a year after opening the latest factory. We think it’s already signed more deals than the consensus is modeling.

GIL remains our Best Long idea, with a clear roadmap to a $60 stock over a TAIL duration, and a de-risked near-term earnings trajectory.