“It was one of those March days when the sun shines hot and the wind blows cold: when it is summer in the light, and winter in the shade.”

-Charles Dickens

We’d be remiss if we didn’t mention either the Masters or Game of Thrones in the Early Look. After all, most of America yesterday was watching one or the other. Or in many cases both.

On the golf side, Tiger delivered an epic victory in the face of many critics and a stiff field of competition. Not to worry though, Keith and I won’t be leaving our day jobs to make one last run at the Stanley Cup. While Tiger’s victory was motivating for many of us middle aged athletic “has beens”, we still need to be practical about the reality of time.

At Hedgeye, our macro team has the four-quadrant model for economies and our demography team, led by Neil Howe, uses the four turnings for his analysis of historical cycles. So, no doubt, you can understand why we might like these seasonal analogies. To understand what winter feels like in the Kingdom of Stock Markets, you really don’t have to go back past December 2018.

From late November to December 14th, the SP500 was down 12%, the VIX was up more than 60%, and many areas of the fixed income market went no bid. As winters go, that was a cold one, albeit also a short one. That said, memories are short and we need to look no further that last week’s Barron’s cover, “This Bull Market Has No Expiration Date”, to see that.

So, what do we do with the game in front of us? Is Winter coming? Is Winter here? Our best recommendation is to set the crystals balls to the side and stick to the data driven process. What is here is #Quad3 and it will have its requisite winners and losers.

Practically speaking though, if you are going to ride the dragon like Jon Snow, and get long and levered of equities, our best advice is to hold on tight!

Back to the Global Macro Grind…

Other than the aforementioned weekend highlights, the economic highlight of note was likely from our Tweeter-In-Chief who once again took aim at the Fed. According to President Trump, “if the Fed had done its job properly” the Dow would have been up an additional 5 – 10K points and GDP would be plus +4%. That sure would have made the “Dow Bros” happy!

Trump is of course missing a few points in begging for more cowbell. Most importantly, cutting interest rates has a meaningfully negative impact on that growing percentage of Americans that live off fixed income. As our Demography team recently wrote:

“We are entering this decade-long “super trough” of working age population growth. And it looks like, for the rest of our lives, we will never again see the working-age population growth we experienced as recently as 2011.”

So, while interest rate cuts in the short run may buoy asset prices, the impact on the growing cohort of retirees could be devastating. Not to mention, a few cuts is unlikely to dramatically re-accelerate economic growth and if we go into negative rate territory (i.e. a lot of cowbell) there is that sneaky unintended consequence of inflation. On that note, oil, one of our favorite asset classes in #Quad3 was up again last week and has now been up 12 of the last 15 weeks . . . and the XLE is up almost 18% YTD.

This of course jives with our Q2 Macro Themes that we presented a few weeks back. The first theme was “USA: Three Quad 3’s”. In this scenario we would expect “a more stagflationary environment that is characterized by multiple compression and the outperformance of inflation hedges” through the duration of 2019. It’s probably no surprise then that our now-cast model for the U.S. economy into Q3 and Q4 of 2019 has growth below consensus and inflation above consensus.

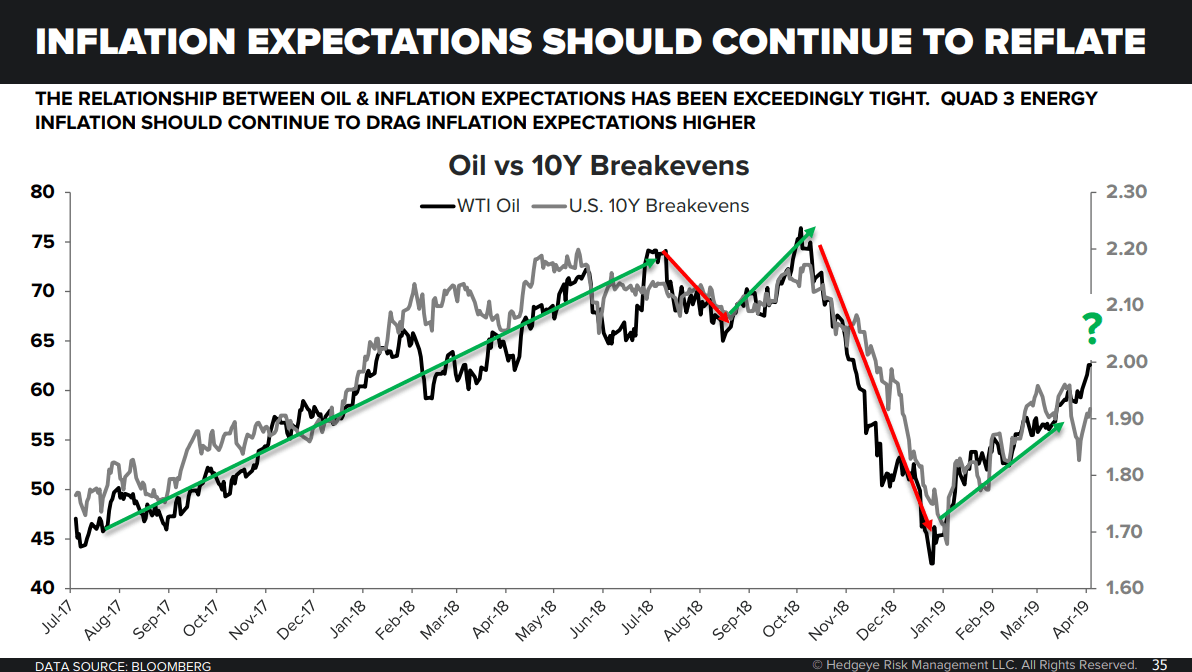

In the Chart of the Day, we highlight a key slide from Q2 Macro Themes deck that looks at Oil v. 10Y break-evens. As the chart quite obviously shows, there is a tight relationship between oil and inflation expectations. The implication is that #Quad3 Energy Inflation will continue to drag up inflation expectations. This path will only accelerate with a weak dollar in the second half of 2019. Simply: more cow bell = weak dollar = rising inflation.

The beautiful thing about America, aside from the Grand Canyon of course, is that innovation doesn’t stop. With successful innovation, eventually IPOs arrive. The LYFT IPO has been a bit underwhelming to say the least with the stock currently trading at sub-$60 and well below its issue price. It seems investors aren’t crazy about a company that may never make money, who would’ve thunk!?!

The next two major IPOs on the horizon are UBER and Pinterest (PINS) and we will be doing pre-IPO deep dives on both. The upshot of having no investment banking conflicts is that we can call these as we see them. The PINS presentation will be today at 12:30 and the UBER presentation will be on April 22nd at 12:30. If you are an institutional level subscriber and would like access, please ping .

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 2.42-2.57% (bearish)

SPX 2 (bullish)

RUT 1 (bearish)

NASDAQ 7 (bullish)

Utilities (XLU) 57.24-58.50 (bullish)

REITS (VNQ) 86.12-88.31 (bullish)

Energy (XLE) 65.80-68.42 (bullish)

Financials (XLF) 26.07-27.29 (bearish)

VIX 11.75-15.99 (bearish)

USD 95.70-97.25 (neutral)

EUR/USD 1.11-1.13 (bearish)

Oil (WTI) 60.77-65.21 (bullish)

Gold 1 (bullish)

Copper 2.88-2.96 (neutral)

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research