J. Crew is on the tape finally talking about a potential Madewell IPO in 2H19 – which is right in line with our thesis when we added the J Crew Term Loan to our Long Bench earlier this week. The term loan trades at about 80 cents on the dollar. J. Crew’s debt load along with weak execution have deterred investors, but we think there is real a value opportunity in Madewell. With Madewell optionality and recent demonstation of IPO value for quality basic apparel, we think the JCrew Term Loan is attractive.

Madewell is a hidden gem suffocating under J. Crew’s debt load

With $1.7bn of net debt and a terrible year of inventory management, J. Crew’s leverage is 15x. What keeps its debt interesting is the retail concept that has quietly and significantly grown during J. Crew’s LBO.

Madewell’s revenues have more than doubled to >$500mm since 2014. Its store count continues to expand at a Mid-High SD% pace. Its same store sales have been one of the strongest in retail industry over the past two years with comps of 25% last year.

Madewell as a fashion basics apparel retailer is on the lower end of spectrum in terms of fashion dependence. We like denim as a core category at 1/3 of the overall mix. In the past year Madewell has expanded assortment adding extended sizes and men’s.

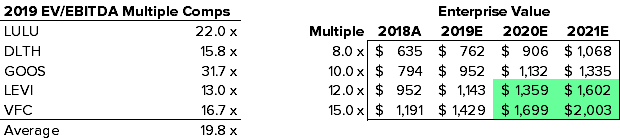

The company, however has not disclosed much detail about Madewell’s profitability. With the strong sales trends it is unlikely that Madwell has low profitability. Using a reasonable or conservative EBIT margin of 12% in the out years shows the potential value of Madewell.

Madewell estimates using a 12% EBIT margin.

Madewell could be a $2bn company in two years

- Using a selected peer group for a multiple comparison it becomes readily apparent that Madewell is worth more than its parent and likely more than the debt.

- A valuation range of 8-15x EBITDA is the most appropriate for a growth company like Madewell.

- On the one hand it has more than 2x store growth potential while on the other hand it is not a luxury retailer with luxury margins.

- We used a range of apparel companies growing the store base by at least MSD% to find the range of multiples.

2018 was a terrible year for J. Crew banner and it’s not over

- The J. Crew brand had many issues in 2018. The new CEO was subsequently fired as he introduced sub-brands, aggressively sought growth, and committed to large inventory purchases.

- Inventory was up 33% at the end of 2018 despite a $39mm writedown of excess goods.

- With excessively high inventory levels to begin the first quarter in which most apparel retailers have seen slow traffic trends due to colder weather and tax refund volatility J. Crew has likely seen further drops in profitability.

- The two entities should be separated before J. Crew potentially drags down a quality asset in Madewell. There is potential for a J. Crew turnaround with the right leadership and strategy. Last night the company named an interim CEO – though prior rumors were around Stefan Larsson as CEO – which would be a home run.

Recent public/debt market action highlights optionality

- The IPO of Levis and valuation at 13x forward EBITDA highlights the scarcity of growth companies (even 160 year old growth companies) in retail.

- The recent debt restructuring of Neiman Marcus using its MyTheresa growth asset as a negotiation tool.

- The IP of Madewell is not secured by the $250mm senior secured bonds like J. Crew’s IP is.

- With the robust growth in Madewell J. Crew could pursue its sale, spin-off, or use as a carrot in the renegotiation of its existing debt.