R3: REQUIRED RETAIL READING

April 15, 2010

TODAY’S CALL OUT

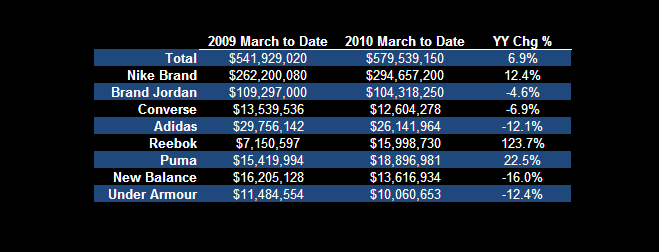

With the Easter holiday falling a week earlier this year, it’s easy to be jolted by the considerable sequential deceleration in footwear trends reflected in this week’s data. While optically striking, it’s important to keep a few things in perspective as one week never a trend makes.

For starters, when looking at March-to-date trends in an effort to negate the calendar shift, industry sales are up 7%. Importantly, this is consistent with the rate of growth we’ve seen since early February. Additionally, it’s important to be mindful that beginning this week, the ‘tough compare’ argument becomes less credible-as footwear embarks on a 5-month stretch of easing compares. In the near-term the most difficult compares and the calendar noise are now behind us, which gives us continued confidence that strength will persist across the athletic footwear space. Oh, and don’t forget Nike’s big product push is still on the horizon.

LEVINE’S LOW DOWN

- In an effort to keep Ralph Lauren’s new flagship store in Paris true to its American roots, the in-store restaurant has been crafted with guidance from New York restaurant icon Danny Meyer. The menu is entirely American, cooked by French chefs, trained by American chefs. The goal was to offer a truly authentic American menu and one with little French influence. The menu includes burgers, fried chicken, and beef flown in from Ralph Lauren’s Colorado cattle ranch.

- Genesco noted that its top priority for use of cash is to make an acquisition, grow a new concept, or to make a niche-acquisition. However, if opportunities in those areas do not present themselves, the company would then look to share buyback as a means to enhance shareholder value.

- Consistent with its track record for beating expectations, PVH confirmed that business trends remain robust and there’s a high likelihood of exceeding full-year guidance at a conference earlier today. Assuming a margin of conservatism with Tommy related synergies, additional upside is likely to come from better than expected growth in southern European markets. Despite being highlighted by other retailers as a challenging market, Italy is a pocket of strength for not only PVH, but WRC as well.

- In a prime example of chasing the trend, management of GCO mentioned that while their merchants don’t sense toning is going to become a fashion item for teenagers (their primary demographic), the category has become such a compelling trend that they are currently testing it. Sounds like the makings of a new Rock ’n Roll line.

HEDGEYE CALENDAR

MORNING NEWS

Long Beach Container Traffic Slows in March - March container traffic growth slowed to 13% growth from 30% in February. The monthly container cargo count at the Port of Long Beach increased 13% in March to 422,774 twenty-foot equivalent container units compared to the same period last year. It is the fourth consecutive month of volume increases at the Port in the year-to-year comparisons. A total of 206,652 TEUs were imported through the Port last month, a 10.8% increase over March of last year. Empty containers, mostly bound overseas for refilling, was up 22.3% to 85,627 TEUs. <polb.com/economics/stats/tonnage>

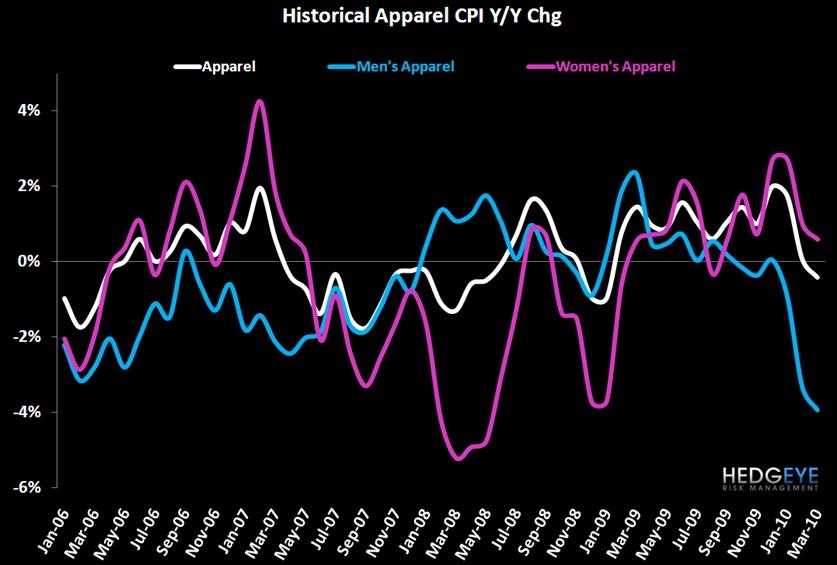

CPI Growth Slows for Apparel - Retail apparel prices declined a seasonally adjusted 0.4% in March compared with February, and dropped 0.4% from a year earlier, the Labor Department said Wednesday in its Consumer Price Index. CPI growth has been sequentially slowing since December 2009. Men's CPI growth has been declining at a faster rate, ending March down 3.9% while women's CPI growth is slowing but holding positive at 0.6%. <wwd.com/business-news>

LTD Expanding Globally - The company on Wednesday said it is creating Limited Brands Canada, a Montreal-based company that will support all Limited Brands retail stores and strategic expansion in Canada, including La Senza, Bath & Body Works, Victoria’s Secret Pink and Victoria’s Secret, which is launching in Canada later this year. LTD will consolidate the creative and merchant leadership of its international businesses at its corporate headquarters in Columbus, Ohio. Also on Wednesday, Limited Brands unveiled a franchise partnership with M.H. Alshaya, Co. to operate stores in the Middle East. Plans are to launch BBW stores later this year in the region. <wwd.com/business-news>

Quiksilver Sells Swim Brands - Quiksilver Inc. agreed to sell its Raisins portfolio of swim brands to AOM Holdings, LLC. The brands, which Quiksilver has operated since 1994, include Raisins, Raisins Girls, Leilani, Island Soul an Island Escape. <sportsonesource.com>

ANF Pays CEO to Not Use Corporate Jet - Abercrombie & Fitch is paying its chief executive $4m (£2.5m) to compensate him for curbing his use of the company’s corporate jet. <drapersonline.com>

Peru Foresees a 16% Increase in Textile Exports - Peru's textile exports are expected to grow by 15% to 16% for this year, beating the industry's estimates of 10%.

Drawback rates might be reduced from 8% to 6.5% from the month of June, in case of an effective recovery of general exports. <fashionnetasia.com>

Target is Busy Launching Collections - The ink is barely dry on the signage for Zac Posen for Target’s Go International collection, and the retailer is unveiling the next limited edition designer for its Go franchise. Gaby Basora will launch a collection at most Target stores and target.com on Sept. 10 featuring the Tucker brand known for its exclusive offbeat and charming prints. Target is partnering with fine jewelry designer Temple St. Clair Carr to launch a limited edition jewelry collection. <wwd.com/retail-news>

Brooks Sports Partners with Docs for Running R&D - Brooks Sports, Inc. announced partnerships with Prof. Dr. Gert-Peter Bruggemann and Prof. Dr. Joseph Hamill, two of the world's leading running biomechanics researchers. Both Hamill and Bruggemann will join forces with Brooks' award-winning footwear team to conduct large retrospective and prospective studies, each intended to garner information that will influence footwear design. <sportsonesource.com>

ColdwaterCreek.com Leads Large Retailers in High Broadband Availability - ColdwaterCreek.com ranked first in high broadband availability tests among large retailers for March, says Gomez. Last month online shoppers could access the apparel and accessories retailer’s site 94.37% of the time. <internetretailer.com>

MW's K&G Fashion Superstore Steps It Up - Mary Beth Blake, president of the off-price K&G Fashion Superstore, has revamped the merchandise mix, increased the percentage of women’s wear, launched a designer showcase, upgraded the presentation and adjacencies in the stores, and launched a new image-centered advertising campaign. <wwd.com/retail-news>