MARKET WATCH: What’s Happening? Cigarette consumption is down in most developed markets, a trend driven by declining smoking rates. For years, rising per-pack prices have masked the decline. But a strategy built on endless price-hikes has a shelf life. Increasingly, Big Tobacco is bracing itself for a smokeless world by investing in alternative products like e-cigarettes, tobacco-heating devices, and even cannabis.

Our Take: Betting on alternative products is no sure thing. Big Tobacco brings no core competencies to, say, cannabis provision. And such a high-risk, high-reward proposition is out of character for an industry valued for its defensive style and stable dividends. A more viable strategy would be to establish a foothold in low- to middle-income economies with rising smoking prevalence and strong population growth. British American Tobacco is the best-positioned in this respect—and its relative affordability makes it the clear choice for willing investors.

If you can’t beat ‘em, join ‘em. That’s what Altria Group executives must have been thinking when they decided to buy a 35% stake in Juul, a market-leading e-cigarette company, late last year.

This was an unwelcome development for Altria analysts and investors. Citi Research analyst Adam Spielman downgraded the company’s stock from “neutral” to “sell,” sending shares tumbling –2%. Spielman sees the Juul investment as a clear sign that Altria is “doubtful about the future of its core business.” Likewise, analysts at Independent Research, Stifel, and Morgan Stanley have all slashed their Altria price targets since news of the deal broke.

Moves like Altria’s are becoming commonplace within the Big Tobacco space. For years, tobacco companies have offset declining volumes with higher unit prices. But this strategy has an expiration date. Increasingly, the industry is hedging its bets by investing in so-called tobacco “alternatives,” from e-cigarettes to tobacco-heating products to cannabis.

While new products and devices may help Big Tobacco at the margins, cigarette revenue will remain the industry’s driving force for years to come. Thus, the most important factor distinguishing winners from losers is global positioning—an issue that will have an existential impact on the long-term future of the industry.

BIG TOBACCO’S BIG PROBLEM: FEWER SMOKERS IN THE DEVELOPED WORLD

In the popular lexicon, “Big Tobacco” refers to the six largest global tobacco companies by revenue: China Tobacco, British American Tobacco, Philip Morris International, Imperial Brands, Japan Tobacco International, and Altria Group. For our purposes, we will focus only on U.S. exchange-traded companies (taking Japan Tobacco and China Tobacco out of the equation) that derive most of their earnings from tobacco sales (taking Imperial out of the equation). This leaves us with three firms: British American Tobacco, Philip Morris, and Altria.

How have these firms fared lately? While the headline revenue growth figures appear relatively strong, they mask a dramatic decline in cigarette consumption. Data from the World Health Organization show that the annual number of cigarettes smoked worldwide peaked in 2012 at 6.1 trillion. This figure has receded in each subsequent year, hitting 5.6 trillion in 2016—the fewest cigarettes smoked since 2003.

In reality, the industry’s troubles far predate the 2012 inflection point in global cigarette consumption. As we noted in our previous piece on the subject (see: “How (and Where) to Bet on Big Tobacco”), more than the entire increase in the number of smokers worldwide since 1980 has been driven by population growth. Declining prevalence (smoking rates per 100 population) in most regions worldwide means that, as population growth slows, we will begin to see a steepening decline in the number of smokers. This is great news if you’re a public health official. It’s terrible news if you’re a Big Tobacco executive or investor.

Nowhere is the issue of declining prevalence more evident than in the United States. CDC data show that the share of U.S. adults who “currently smoke” hit a record-low 14% in 2017, down more than one percentage point from 2016. (This measure refers to adults with a history of smoking who reported doing so “every day” or “some days” at the time of the survey.) In fact, the U.S. smoking rate has been on the decline for half a century, having registered only two YoY increases since the CDC began tracking it in 1965.

Over the past two decades, the decline in U.S. cigarette smoking has been driven in particular by Millennials. This generation has brought about a decline in risk-taking behavior of all types, whether it’s cigarette smoking, alcohol consumption (see: “Where the Wild Things Aren’t”), or violent crime (see: “What’s Behind the Decline in Crime?”). Data from the biannual Monitoring the Future survey show that, since 1997, daily cigarette smoking has plummeted by 85% among high-school seniors; 90% among 10th graders; and 91% among 8th graders.

THE OLD STRATEGY THAT WORKED: PRICE HIKES

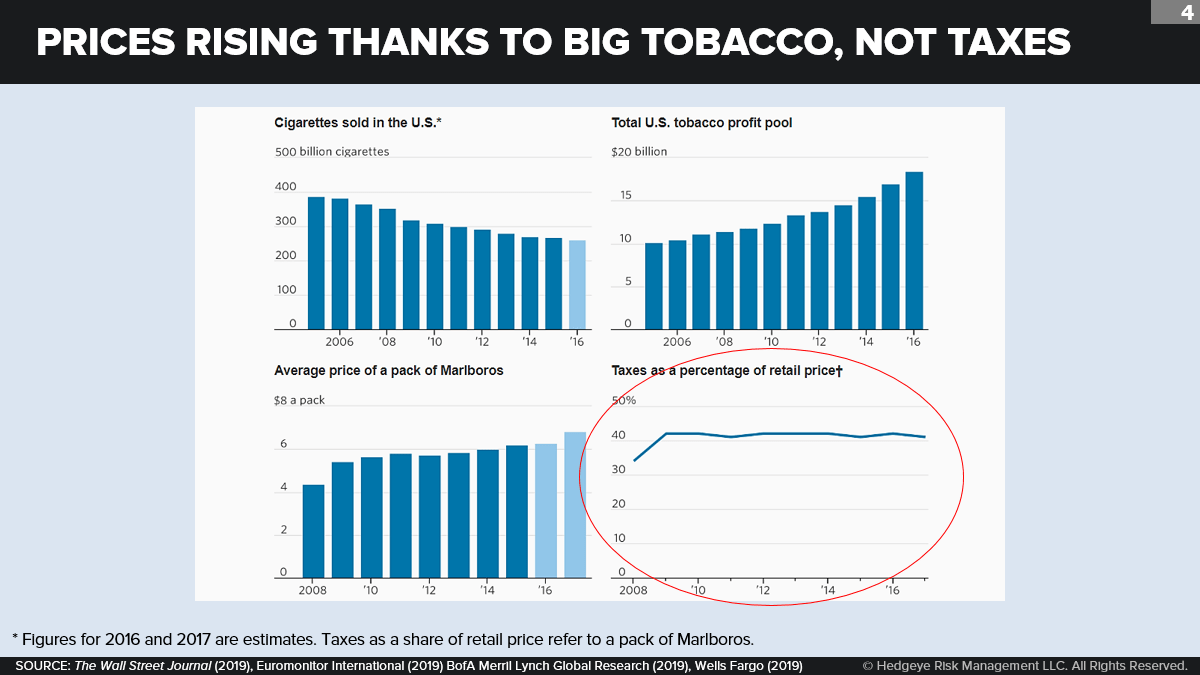

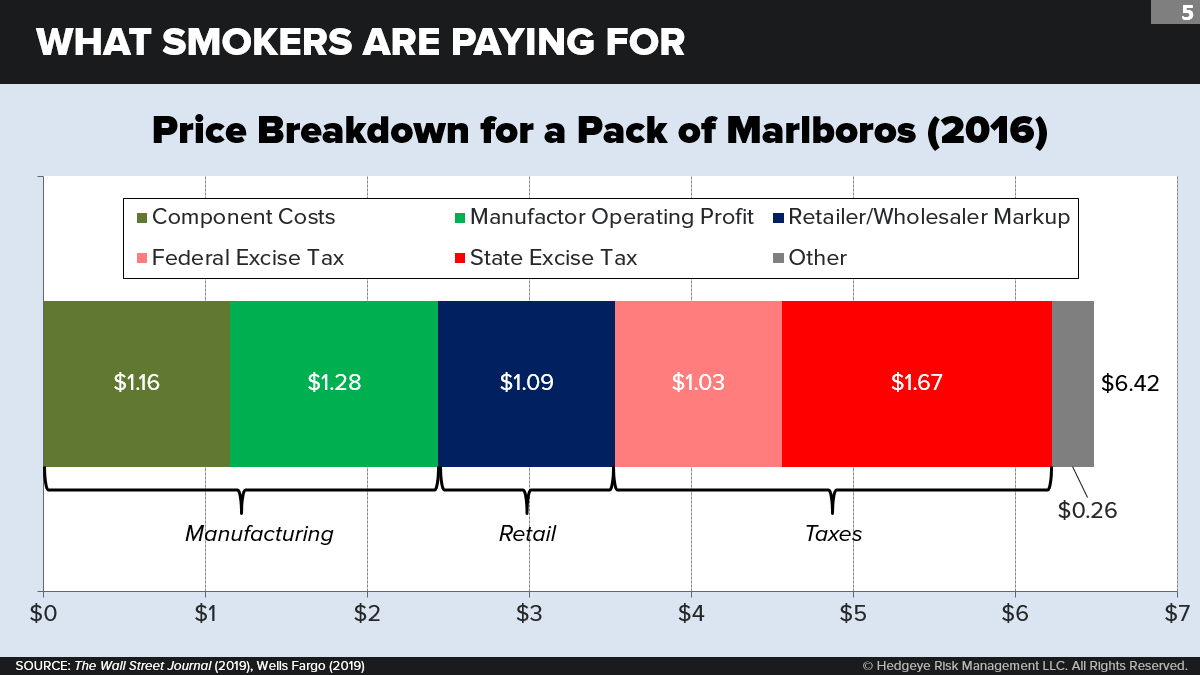

For years, Big Tobacco has been compensating for the decline in smoking prevalence within the U.S. market by raising its prices. In 2001, an average pack of cigarettes cost $3.73 in the United States. By 2016, that same pack cost $6.42, a 71% rise.

Contrary to popular opinion, this rise has been driven mostly by pre-tax, not post-tax, prices. Since 2009, in fact, the increase in total per-pack cigarette prices can be entirely attributed to companies raising their pre-tax prices; taxes have been flat at around 40% of the retail price.

Why has Big Tobacco been raising prices? In a word, because it can. A cigarette smoker is the very definition of the price-inelastic consumer—which has always given cigarette producers enormous potential pricing power. Historically, however, that power has been restrained by interfirm competition. Through most of the postwar era, there were as many as seven major producers, each fighting to gain market share and often cutting prices in order to do so.

No longer. After fifteen years of successive mergers and acquisitions, the industry is today dominated (over 80% of sales) by just two firms: Altria and British American Tobacco. The former was founded as Philip Morris Companies in 1985 before splitting into two businesses in 2003: the U.S.-only Altria Group and the non-U.S. Philip Morris International. The latter, British American Tobacco, was a relatively minor player in the United States before its 2017 acquisition of Reynolds American, which gave it access to U.S. brands such as Newport and Pall Mall.

As the competition declined, the pricing power grew.

This favorable environment (for the survivors) did not emerge by accident. Rather, it was the result of a deliberate plan by Philip Morris Companies that worked out brilliantly. In the early 2000s, facing billions of dollars in punitive damages and the prospect of 1,500+ additional lawsuits, the company made the decision to invite, rather than fight, regulatory oversight. Nicknaming this pivot “Project Sunrise,” the company began throwing its full weight behind a proposal by Senator Ted Kennedy to place the industry under FDA oversight. While the move confused and infuriated competitors, it proved to be a huge win-win for Philip Morris itself.

In exchange for having Congress limit its product and tort liabilities and thus hedge its downside political risk, the company agreed to buddy up with government regulators and allow the FDA to gradually kill off the cigarette market with advertising bans and mandatory product warning labels. The first part of the deal was an obvious win for Philip Morris. Yet so too was the second part. It knew that the stranglehold on future industry growth would come mainly at the expense of smaller competitors. And with them out of the way, it could raise profits faster than the market was shrinking. Smaller firms like Lorrilard recognized the threat, complaining that the Kennedy bill would “virtually eliminate our ability to communicate with adult consumers, thereby locking in Marlboro’s dominant position.”

Philip Morris also recognized that a government partnership would be self-perpetuating. In time, states hooked on easy tax money would be motivated to let Big Tobacco survive, even thrive. States view cigarette excise taxes—which automatically increase as the firms raise their cigarette prices—as a win-win for them: They get more tax revenue at the same time that higher prices discourage consumption. This essentially makes government “a financial stakeholder in smoking.” Excise taxes also help Big Tobacco in another, less obvious way—by making it impossible for consumers to bargain-hunt. It’s easy to mask your underlying price when your product is subject to more than 600 different tax rates across localities nationwide.

All told, Big Tobacco’s pivot toward regulation has served the industry well. But price hikes are not a sustainable strategy for long-term growth. And for a very simple reason. At some point, the price-elasticity of demand rises above negative one: A combination of less consumption plus consumers turning to substitutes (everything from nicotine gum to bootleg smokes) starts to bend the revenue curve down.

Big Tobacco may already be reaching that point. One key bit of evidence is that, state by state, the final price may already be self-defeating in terms of revenue. In the eleven states where the tax per pack is over $2.00, higher cigarette tax rates are actually negatively correlated with cigarette taxes as a share of total state revenue. Keep in mind that the demand curve for state tax revenue is tied at the hip to the demand curve for tobacco firm revenue.

At some point in the very near future—perhaps already—the per-pack price required to turn a profit in the face of declining U.S. smoking prevalence will be too expensive for most consumers.

THE NEW STRATEGY THAT WON’T WORK: ALTERNATIVE PRODUCTS

With cigarettes falling out of favor in most regional markets, Big Tobacco has opted to hedge its bets by investing in “alternative” products. Most of these cigarette alternatives fall into the bucket which the industry likes to call “reduced-risk products” (RRPs), including e-cigarettes, heated tobacco products, and smokeless tobacco products.

Altria’s acquisition of Juul is the latest example of Big Tobacco’s investment in the RRP space. The company also touts a number of profitable e-cigarette products, including its flagship MarkTen and Green Smoke brands. For its part, British American Tobacco has invested $2.5 billion in RRPs since 2012.

But if one company has staked its future on RRPs, it’s Philip Morris. The company owns one of the leading tobacco-heating devices on the market, the iQOS—which enjoyed early success in Japan before cooling off. André Calantzopoulos, the company’s chief executive, is quoted as saying, “We are crystal clear where we are going as a company: We want to move out of cigarettes as soon as possible.” Those are strong words for an executive whose company earns just 14% of its revenue from RRPs (according to Philip Morris’s latest 10-K report). To be sure, Calantzopoulos wants this share to rise to 40%, or “hopefully much more,” by 2025.

Investing in RRPs—particularly in the United States—is thus no failsafe. The space looked like a good bet when the FDA announced its new anti-smoking plan last year, which would lean on RPPs to help wean smokers off of cigarettes. But public health officials point to a mounting body of research showing that e-cigarettes are being used as a “gateway drug” by teenagers. (See: “Is Vaping Creating a New Generation of Cigarette Smokers?”) Everyone from the U.S. Surgeon General to the FDA Commissioner has raised the alarm over e-cigarette use among minors.

As a result, a bevy of new regulations have hit the U.S. RRP space over the past year. Last September, FDA chief Scott Gottlieb called on manufacturers of five leading e-cigarette brands to submit plans that would prevent minors from using these devices. (See: “FDA Tackles the Teenage Vaping Epidemic.”) Then, in November, Gottlieb announced plans to ban most flavored e-cigarette sales in convenience stores on the grounds that these products are used disproportionately by minors. To be sure, Gottlieb’s abrupt decision to resign his post throws these initiatives into question.

Some industry watchers are portraying Gottlieb’s departure as a boon to Big Tobacco in general, and to the RRP space in particular. But we’re not so sure. Remember that RRPs were originally a major part of Gottlieb’s anti-smoking push. Gottlieb even served on the board of an e-cigarette retailer prior to his FDA appointment, a fact that caused plenty of consternation among consumer advocates at the time. In short, Big Tobacco could do much worse than Gottlieb. A replacement appointed by a President Warren or a President Harris, for example, would surely be less inclined to play nice with Big Tobacco.

Given the uncertainty of the RRP space, Big Tobacco has set its sights on other alternative products, ones that are so far outside Big Tobacco’s core competencies that they aren’t even yet classified as such.

One emerging dark horse is cannabis. Back in 2016, Philip Morris invested $20 million in Israel’s Syqe Medical, which is developing a medical cannabis inhaler. Global conglomerate Imperial Brands invested $13 million last year in U.K. biotech company Oxford Cannabinoid Technologies, which works in the medical marijuana space. The largest Big Tobacco-cannabis transaction belongs to Altria, which spent $1.8 billion on a 45% stake of Canadian cannabinoid company Cronos Group. Cannabis seems to be an attractive proposition for beleaguered industries looking to resuscitate their growth: Constellation Brands, maker of Corona beer, staked its own claim in the cannabis market last year with its investment in Canopy Growth.

But here we must ask: What differential advantage does Big Tobacco have in the cannabis space? Sure, they know how to roll cigarettes. But that skillset may be of little use in a world of legalized cannabis: In states that have already legalized, most cannabis products are eaten or vaped, not smoked. What’s more, high-margin cannabis use is associated with a high-SES customer—nothing like the low-SES customers than now dominate cigarette use. There also the likelihood that Big Cannabis may not even want a Big Tobacco partnership. After all, cannabis is trying to win the battle of public opinion in pursuit of national legalization, a battle that Big Tobacco lost long ago. The mere association with Big Tobacco may be enough to give consumers—and regulators—pause.

What should investors take from all this? Sure, alternative products, whether RRPs or cannabinoids, have plenty of upside. But it would take a huge leap of faith to bet on Big Tobacco to engineer a seamless transition to a smokeless future. And even if the industry does manage to accomplish this daunting feat, there’s no guarantee that it is equipped to lead that future.

At the very least, such a transition will involve plenty of growing pains, and may very well destroy one or more firms. At the most, regulators will see through Big Tobacco’s veneer of trying to change the world through reduced smoking prevalence (see: “Big Tobacco Funds Anti-Smoking Research”) and will impose heavy restrictions, even bans, on RRPs. Investors would be forgiven for not wanting to take such a leap of faith. Above all else, Big Tobacco is known for its stability—its consistent performance during recessions and its steady dividends. A high-risk, high-reward bet on alternative products is out of character.

A BETTER NEW STRATEGY: THINKING GLOBALLY

As much as Big Tobacco talks about its vision of a future dominated by e-cigarettes and tobacco-heating devices, the industry is still beholden to its flagship product: cigarettes. It will be global positioning, not RRP innovation, that will determine the industry’s long-term winners and losers.

In our previous piece on the industry, we pinpointed three criteria for a thriving Big Tobacco market:

- rising smoking prevalence;

- strong population growth; and

- low- to middle-income grouping.

Let’s now evaluate global markets based on these three criteria. Once we do so, we will be able to compare relative company valuations on the basis of global positioning.

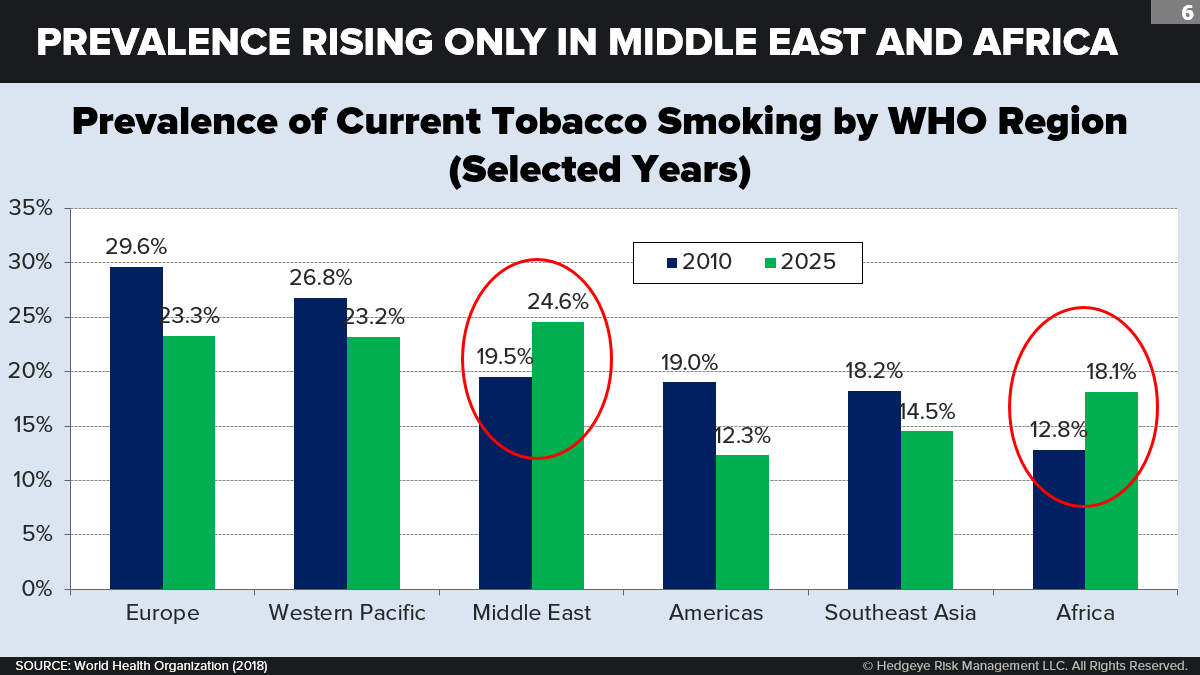

Our first criterion is rising smoking prevalence. The World Health Organization tracks data on smoking rates, both historical and projected, by country and broader region. What we see is that today’s heaviest-smoking regions are not necessarily tomorrow’s. The Middle East (which WHO calls the “Eastern Mediterranean,” a region which also includes parts of North Africa) has the highest projected 2025 prevalence at 24.6%; in 2010, that figure was just 19.8%, third-highest among all regions. In fact, the Middle East is one of just two regions where smoking prevalence is on the rise. The other region is Africa, where prevalence is expected to rise from 13.9% in 2016 to 18.1% in 2025.

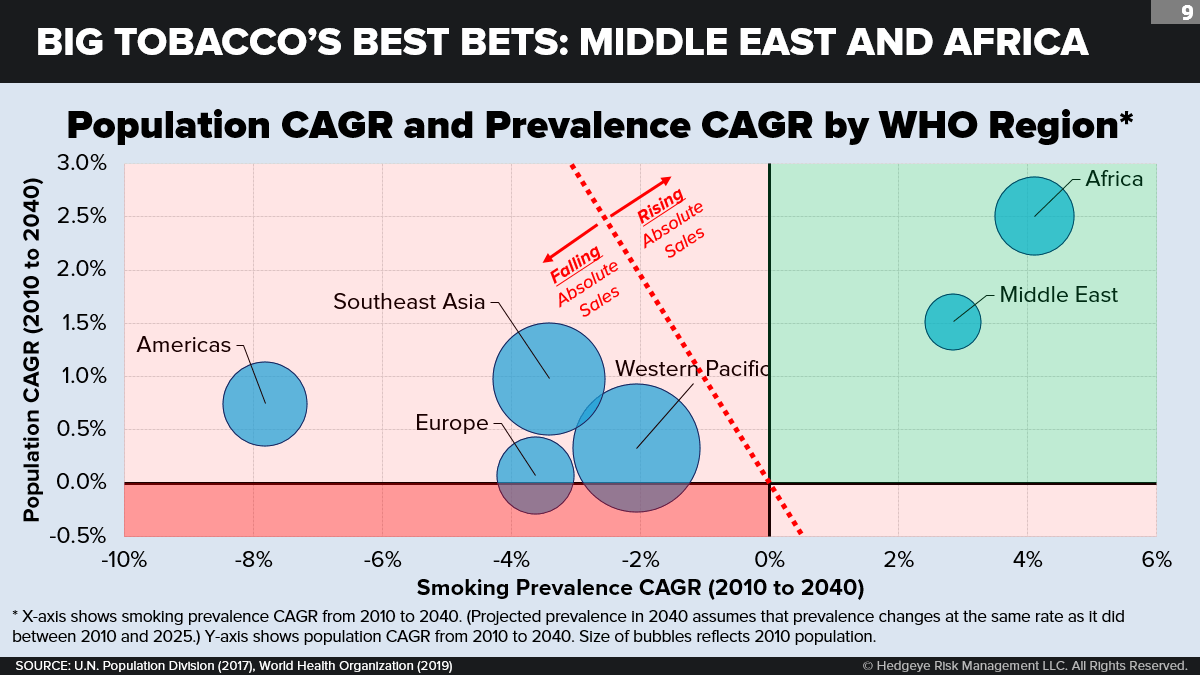

Our next criterion is strong population growth. We can look a little further into the future here using the U.N. Population Division’s medium-fertility projections. These data show that Africa is expected to register the strongest overall population growth from 2010 to 2040, with a CAGR of 2.5%. As in prevalence growth, the Middle East ranks second in expected population growth, with a CAGR of 1.5%. These two regions are the only ones in which total population is expected to grow faster than 1% per year.

These first two criteria are the most important ones for Big Tobacco, because together they can be used to quantify the growth of the number of smokers in each region. After all, population growth times prevalence growth equals consumption growth. Our next chart shows just how important geographic positioning is for Big Tobacco. The number of cigarette smokers in Africa can be expected to nearly triple from 2010 to 2040 (up 284%). The number of smokers in the Middle East will more than double (up 139%). In every other WHO region, consumption will register a net decline.

Let’s look at the data another way. Imagine a scatter plot with prevalence growth along the X-axis and population growth along the Y-axis. The northeast quadrant, or “Quad 2,” would be the most desirable region—rising prevalence and rising population growth. Africa and the Middle East are the only two regions in this quadrant. Moreover, they’re also the only two regions with expected rising absolute sales to 2040.

One final criterion to consider is low- to middle-income grouping. Research has demonstrated that cigarette smoking prevalence has a negative correlation with income. Big Tobacco thus stands the best chance in low- to middle-income societies that will likely take decades to reach the higher-income stage at which prevalence begins to decline. Of the six regions we’re investigating, Africa is the one with the highest share of low-income countries, followed by Southeast Asia and the Middle East.

In aggregate, the most promising markets for Big Tobacco over the next two decades are Africa and the Middle East. It’s not particularly close. In the middle are Southeast Asia and the Western Pacific. The least promising markets are Europe and the Americas.

WHO IS BEST PREPARED FOR THIS NEW STRATEGY?

Now that we’ve pinpointed the Big Tobacco’s growth markets, we can look at which firms are best positioned within these markets.

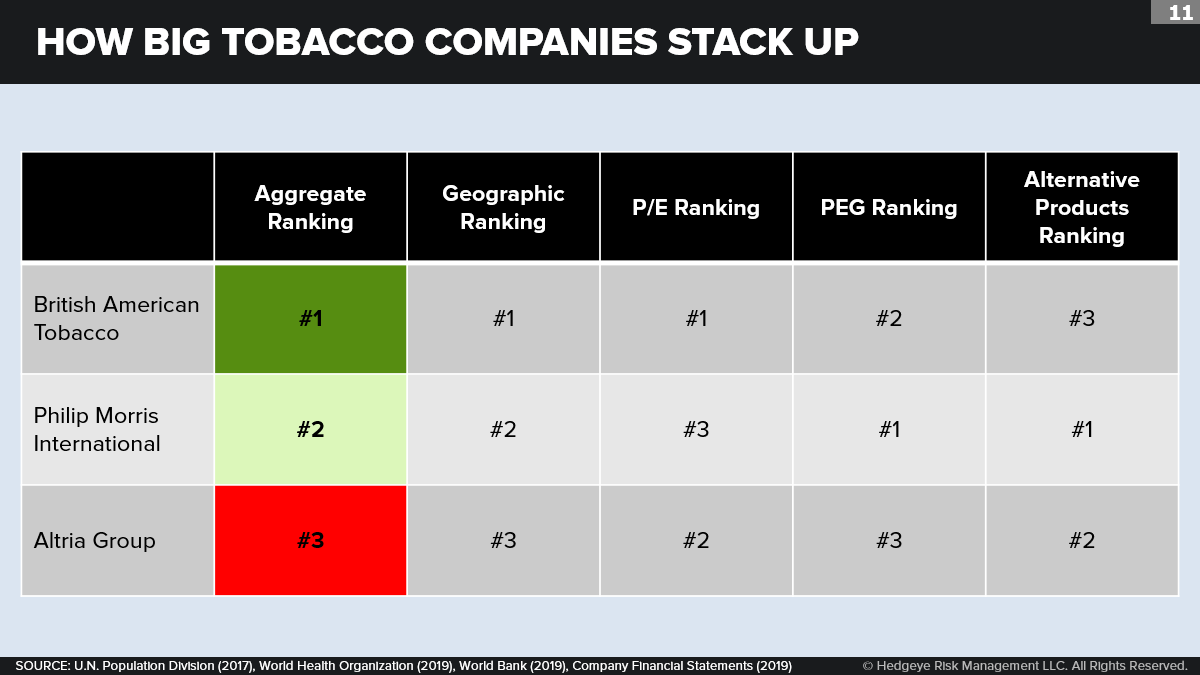

Unfortunately, tobacco companies don’t break out their revenue into regions that exactly match the WHO definitions. But we can make some valuable observations nonetheless. In 2018, Philip Morris earned 13.9% of its revenue from what we would consider strong markets, the Middle East and Africa. What about British American Tobacco? In 2018, the firm earned 19.9% of its revenue from its “Asia-Pacific & Middle East” region, and another 16.8% from its “Americas & Sub-Saharan Africa” region. If we divide each of these regions in half to get a rough estimate of the firm’s “Middle East and Africa” share, we come up with a figure of 18.4%.

Going by these figures, British American Tobacco enjoys the best geographic positioning of the big three firms. But it’s close between them and Philip Morris. If not for British American Tobacco doubling down on a weak U.S. market in 2017 with its purchase of Reynolds (for which the company paid a 26% premium, no less), its geographic positioning would have been far and away the best of any Big Tobacco firm.

Altria is the odd one out. The company earns the entirety of its revenue from the United States and has no exposure whatsoever to growth markets. It’s little surprise that the firm has posted YoY revenue growth of less than 1% over the past two years.

The question investors will ask at this point is: To what extent have these relative strengths and weaknesses been priced into the stock? Let’s look at some of the key valuation ratios of these firms to find out.

British American Tobacco is by far the most affordable on a price-to-earnings basis, with a P/E of 11.9—compared to 14.8 for Altria and 17.9 for Philip Morris. Adjusted for growth, British American Tobacco looks just as attractive: The firm has a PEG ratio of 2.6, virtually tied with Philip Morris (2.7) and ahead of Altria (2.1). Also important to investors: British American Tobacco pays out a higher dividend yield (6.7%) than either of its competitors.

What about investors who are willing to pay a premium for Philip Morris because it has the best “vision”? The firm leads the way in the growing RRP space. That has to count for something, right? Let’s look at it another way. If this were any other sector, would you really want to invest in a company that openly disparages its own flagship product and vows to abandon the strategy that made it a billion-dollar company? We think not.

THE PROS AND CONS OF “SIN STOCKS”

Let’s be clear here: Big Tobacco is not for everyone. A growing number of investors want to feel good about what’s in their portfolios, and many “ESG” portfolios rule out “sin stocks” (traditionally defined as tobacco, alcohol, and gambling) no matter how affordable they may be. Other investors disagree, saying that they prefer to separate what they do to improve the world from how they invest their money. The daunting challenge for the ESG investor is figuring out how to take all the infinitely diverse activities encompassed by global GDP—from the firing of weapons to spinning of windmills—and rank them all by levels of virtue. Some investors are up for this challenge. Others are not.

A question more relevant to investing per se is how membership in the “sin stock” family affects equity alpha. Investors must keep in mind the negative aspects of sin stocks—including less analyst coverage, less liquidity, and smaller representation in “norm-constrained” institutions such as pension funds than otherwise comparable stocks. Sin stocks are also more vulnerable to unpredictable changes in the legal and regulatory environment.

On the other hand, sin-stock investors probably benefit from a “boycott risk premium”—in other words, they are likely to generate an excess return that can only be explained by their bad reputation. As a rising number of mutual funds and hedge funds join the ESG-style stock-screening movement, a few others (like VICEX) have done very well by leaning hard the other way with a relatively small AUM. In the words of VICEX manager Gerry Sullivan, “If you wrapped these stocks in white paper and couldn’t tell what they were, people would love them.”

Bottom line: For investors looking for a long-term and defensive dividend machine that is well-positioned globally, British American Tobacco and, to a lesser extent, Philip Morris are worth a look.