This was a respectable quarter for KSS in light of the fact that it was comping against a monster 4Q17. It seems odd to call a decline of 3% in revenue, 4% Gross Profit, and 6% EBIT ‘respectable’. But hey, we’re talking about KSS. The company’s flaw this quarter was with the guide. Simply put, it’s too aggressive. We’re coming in $0.06 below the current Street estimate in 1Q, and $0.57 lower than the guide for the year (about 9%). Biggest delta is Gross Margin, should start to show weakness after 18 months of being near bullet-proof, as well as credit, which appears to have reached the end of its rope. Also let’s not forget about cash flow. I know nobody ever asks about it on the call, but it’s pretty critical from where I sit. With the sharp increase in capex, lack of runway to liquidate inventories via store remodels, outsized charges to close stores due to lease inflexibility (a big part of our call), and pressure on credit revenue (100% margin) we could see free cash flow down 50% in 2019 on just a small earnings miss. No matter how I slice it, KSS trading at 14-15x EPS and 8-9x EBITDA is in no way pricing in any potential for missing the company’s bullish guide. Being expensive is not a catalyst, but missing earnings is – and in 2019, KSS is likely to miss. Not the kind of name you want to be long as we transition from Macro Quad 4 to Quad 3 – where we’ll be sitting for the next two quarters. I’m comfortable shorting more on today’s pop.

The print:

- The quarter was solid, $2.24 vs $2.18, each line slightly better than expected after holiday was pre-announced (though its hard to tell where the actual street comp was with shifted vs unshifted). -1% reported comp, +1% shifted comp on top of +6.3% last year is good top line performance. Transactions were up, also a positive.

- KSS is raising the dividend 10%, now about a 3.8% yield at current price.

- EPS guidance for the year is bullish up 6%, with comp up 0-2%, gross margins positive +10bps, and flattish SG&A rate with 1-2% growth. Company plans to buyback $400mm-$500mm in stock.

- The quarter’s guide was bearish. Basically 0% comp against the easiest underlying comparison of the year would imply a 2 year slowdown of 350bps, with a 100bps hit last year from winter storms. Compares get way harder for the rest of the year.

- With that weak comp GM% is guided flat to down vs the year up. That means 1Q EBIT decline and potential earnings decline even with the likely stock buyback and lower interest expense.

Callouts:

Beware the Lease Inflexibility

- We’ve talked about how the 20 year lease duration for KSS (about 3x that of the typical strip anchor) limits its flexibility and optionality with store locations.

- This print the comments around charges on the 4 planned store closures sheds some light. The company guided to $50-$55mm in charges in 2019 with “most of the 2019 charges will be related to future lease commitments at the 4 stores that we'll be closing”.

- That’s a big price for 4 store closures. Recall last week when GPS noted ~80 stores would cost $250-$300mm.

- ~$3.2mm per store for GPS closures.

- ~$12.5mm per store for KSS store closures.

- What if KSS wanted to close 100+ stores, could it afford it? Don’t forget about the leverage optics when the leases come on balance sheet next quarter as well.

Gross Margin Runway

- Company is guiding gross margin up 10bps for the year, with 1Q flat to down. That makes sense in terms of the gross margin comparisons starting harder and easing throughout the year.

- What makes less sense is that margins still go up when the driving force behind margin upside was “standard to small”, which around mid-2018 hit its target of 500 stores the company saw an opportunity to execute it in.

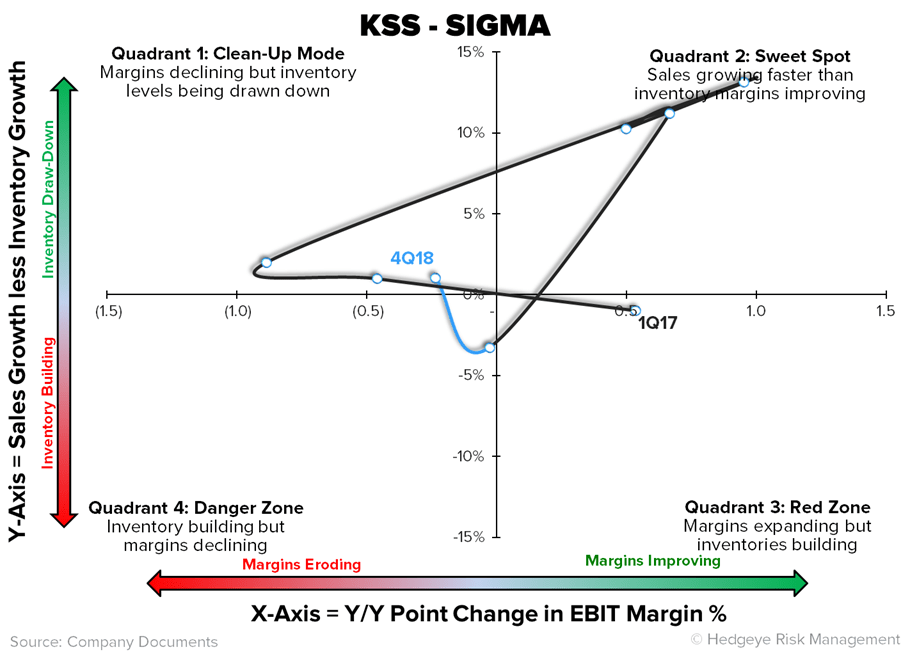

- Ecommerce dilution has to start showing its face soon with double digit growth contributing nearly 3 pts of comp this Q. Inventory is relatively clean for KSS, but the industry is now facing some inventory problems, that was not the case 12 months ago.

Active

- Active comped mid single digits this quarter, with high single for the year. The means active can account for all comp growth in 2018.

- The company’s 30 store pilot has led them to expand the initiative to 160 stores. It’s somewhat funny that Golf was cited as a success in the Active expansion, after all, it’s just a polyester collared shirt, and its doubtful those shirts are purchased/used primarily for golf. Expanding in the active category makes sense for the near term, as it’s adding more of things people actually want to buy. But we think we are towards the tail end of an active growth cycle, and the brands are innovating and investing in ways to go around traditional retail in getting its product to customers.

- KSS noted it is expanding its plus sized offering with Nike, strangely at the same time its launching its own plus sized brand EVRI. Notice Nike has recently been putting out new marketing campaigns to highlight product being worn by plus sized models/athletes/individuals.

Free Cash Heading the Wrong Way

- The company just had its best free cash flow year since 2009, the stock looks very cheap on trailing free cash, but looks like 2018 might be a cycle peak of cash generation.

- Capex is guided to $850mm after just $578mm in 2018. Plus there’s the $50-$55mm in charges from store closings. Inventory likely only gets worse with standard to small seeing diminishing returns.

- We could see free cash flow down 50% in 2019 on just a small earnings miss.

Traffic & Partnerships & New Brands

- Kohl’s and CEO Gass are trying hard to drive traffic. Transaction growth has been underwhelming even in this great consumer environment of the last 18 months. However it’s not due to lack of effort or testing.

- Here are some of the partnerships the company is talking about. Scott Living (the guys from HGTV’s Property Brothers) collection, Planet Fitness collaboration (PLNT planning to go in next to 10 KSS stores, Amazon returns and shop in shop, Weight Watchers wellness collection, Aldi store (~10 Aldi going in KSS leased space), Nine West brand launch, revamped beauty with new brands (prestige brands, including Polo Ralph Lauren, Philosophy and Dolce & Gabana), Active expansions, among others.

- KSS is trying many things, and most make a lot of sense. The one we think is a huge mistake is its dealings with Amazon.

- The Amazon partnership is changing the shop in shop model, to more of a traditional wholesale model that is expanding into 200 stores that will carry an Amazon product assortment. We argue that putting any Amazon devices into your core customers’ hands is a big mistake. They are all designed to make people shop more on Amazon. Meanwhile, after nearly 18 months, the company still cannot point to upside in traffic from the Amazon returns initiative. Gass teased some sort of change happening here saying: “The big question, of course, at hand is, how will we go forward. And we continue to be in conversations with Amazon. It really needs to be a win-win for both. So I'd say, stay tuned on that front.”

Credit and Rewards

- The company grew credit revenue in 2018, 4Q was down due to the 53rd week. We think we’ll see credit revenue down in 2019. The company chose not to guide to it, but did note that it consolidated its Dallas call center, implying that the SG&A cost side was brought down (interesting change now that the portfolio revenue is reported rather than EBIT pre-606). The company is talking about being hopeful to convert new customers to card members. However if you look at the new rewards program structure (below), it seems pretty clear that the credit card is not needed to get the perks.

- The new Kohl’s Rewards pilot is being expanded to more stores in 2019, planning nationwide rollout in 2020. We’ll see if that is able to drive comps. Yes2You failed in being a traffic driver over the long term.

Source: Kohl’s Website