Position: Long Germany (EWG); Short Euro (FXE)

Following the European Central Bank’s decision today to keep its main interest rate on hold at 1%, ECB President Jean-Claude Trichet held his usual follow-up press conference. Notably, the media pressed him in the Q&A session to explain the economic conditions (parameters) that will initiate the EU and IMF to inject funding for Greece, or conversely the market conditions that should initiate the Greek government to request capital. In typical Trichet fashion he was tight-lipped on such questions, but did express that “a default is not an issue for Greece”.

So what did we learn from today’s ECB release?

- The ECB has decided to keep the minimum credit threshold for marketable and non-marketable assets in the Eurosystem collateral framework at investment-grade level (i.e. BBB-/Baa3) beyond the end of 2010, except in the case of asset-backed securities (ABSs).

- As of 1 January 2011, a schedule of graduated valuation haircuts to the assets rated in the BBB+ to BBB- range (or equivalent), which will be announced at the ECB meeting in July 2010.

- This graduated haircut schedule will replace the uniform haircut add-on of 5% that is currently applied to these assets.

- Marketable debt instruments denominated in currencies other than the euro, i.e. the US dollar, the pound sterling and the Japanese yen, and issued in the euro area will no longer be eligible as collateral as from 1 January 2011.

One main take-away here is that with Greece’s sovereign debt rated at BBB+ by Standard & Poor’s and Fitch Ratings, further ratings downgrades will put in jeopardy Greece’s ability to borrow from the bank as stricter collateral obligations are imposed. We’ll know more about this latter point when the ECB presents its schedule for haircuts in July, but considering Trichet’s determination of the European community to assist Greece (or other PIIGS), it wouldn’t surprise us if exceptions were made to said measures.

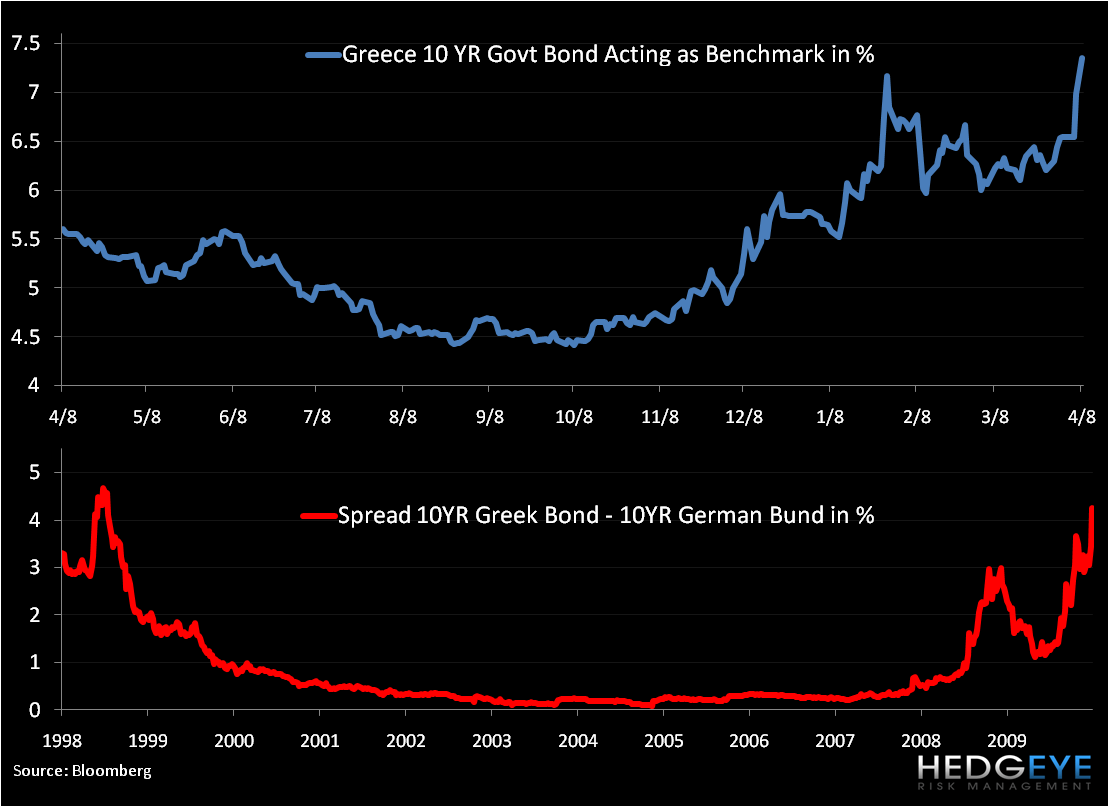

The recent spikes in Greek bond yields, rising Greek CDS prices, and a plunge in the Athex equity market have furthered investor doubts that Greece can meet its debt obligations. The chart below shows the recent spike in the 10YR Yield and the lower chart gives historical perspective on the Greek spread over the risk-free 10YR German Bund. As Greece looks to issue more debt in the coming weeks, rising current yields will put upward pressure on future rates; as we’ve said numerous times, kicking the debt “can” further down the road does not end well. For now, without EU policy to deal with sovereign debt issues of its member states, this game of “wait and see” from Trichet and EU leaders will prolong the underperformance of Greek bond and stock markets.

Matthew Hedrick

Analyst