A strong quarter for Ruby Tuesday, trends may slow from here.

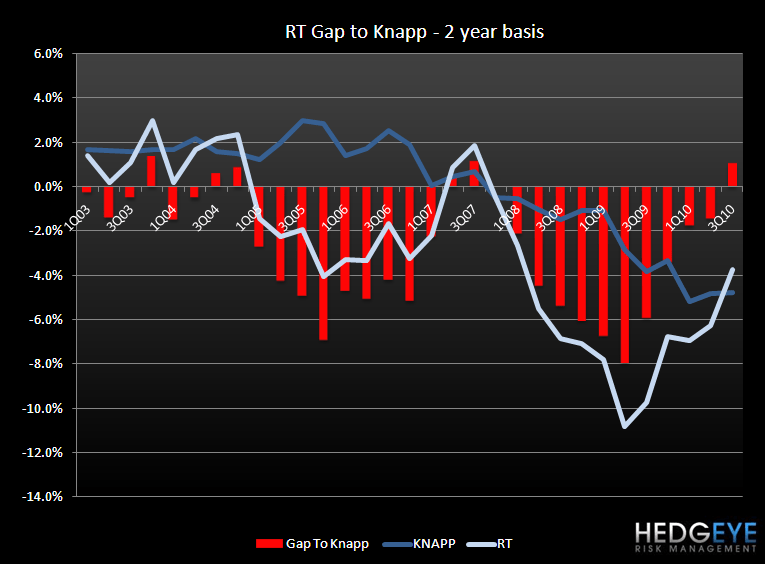

3Q SSS came in at -0.7%, slightly better than the preannounced range of -0.8% to -1%. RT has outperformed Knapp now for 4 quarters, partly attributable to easier comps. This was the first quarter RT outperformed Knapp on a two-year basis in over two years. The two-year “Gap-to-Knapp” was 1%. RT raised FY SSS guidance to -1% to -2% from -1% to -3% and raised FY EPS to $0.60-$0.65 from $0.50 to $0.60 (street was already at $0.63).

It was good quarter for RT, but it looks like this could be the last quarter of accelerating trends. RT is partially benefiting from better overall industry trends and renewed focus on profitability. In addition, it appears that RT is taking some market share from its larger rivals Chili’s and Applebee’s.

At 15x NTM EPS and 7.6x EV/EBITDA, RT has made a full recovery and the associated benefits to the company are now in the past. Presently it seems that Q4 will likely be the first quarter in five where EBIT margins could be down year-over-year. With Brinker setting the stage to be more competitive the big market share gains for RT could be a thing of the past.

The industry outperformance yesterday has put the group in a precarious position.

RT Earnings Call 3QFY10 - SUMMARY

3Q was the best sales quarters in three years.

- Despite weather

- Lapping difficult comps

- Closed underperforming stores

- SSS were down 0.7% in the quarter

- Bad weather impacted that by 1.5% to 2%

- SSS were slightly positive in January and February even with the weather impact which was significant in February

- Sales outperformed Knapp on a 1 and 2 year basis

Focus on brand strategies has paid dividends despite lapping last year’s 3Q which was 4 points better than 2QFY10.

- Getting people in to see the new RT and they are coming back

- Introduced mid-year menu update in November:

- Variety with a focus on quality and differentiation

- Consumer’s responded well

Primary corporate goals were:

- Increase SSS

- Max cash flow reduce debt

- Strengthen brand by providing guest with providing value

- Long term strategies are helping create additional value

Price increase was 1-2%

- Want to increase average check from $13.50 to $14.50

- By managing promotions RT achieved good sales and good profits

- Traded some check for profitability this past quarter

Financials

Earnings

- $0.28 vs. $0.09 last year

- Last year included impairment charges of $0.17 vs. closure and impairment charges of $0.02 this year

- Restaurant margins were 19.5% for the quarter versus 18.8% last year

- Food costs flat at 28.5%

- Continue to experience favorable commodity costs

- Labor costs declined to 32.7% from 33% as a percentage of sales

- Store closings, initiatives outweighed higher payroll taxes

Other

- Depreciation was down 50 bps as a percentage of sales because of closures last year and assets becoming fully depreciated since the prior year

- Higher G&A, up 70 bps, was due to bonus accrual and other minor factors

Interest expense declined

- Lower interest rate

- Lower spread to LIBOR

- Less outstanding

Tax rate was 20.1% versus 5.3% last year

Balance Sheet

- Book debt was $322 million, down $43 million in the quarter

- YTD paid down 171 million of debt so far and $200m paid off in the last twelve months

- Book debt to capital was 38% at end of quarter. Book debt to EBITDA was 2.2x

Guidance on new stores openings

- No company operated restaurants in 4Q. Closing one

- Franchisees opening between 1 and 4, up to two of which are international

- For the full year, intend on opening none and closing 14, franchisees are anticipating opening five to eight, including three to five international

Company operated SSS will be down 1-2% for the year - down 1.9% YTD. 4Q comparison represents the most difficult comparison of the year

ROP down slightly because of compelling value strategy

D&A will be 63-65m

SG&A down 12% yoy

Increase in marketing expense from last year’s low level

- Newspaper

- Internet

Bonuses are expense expected to be up

Interest expense - $16-$17m

EPS diluted - $0.60-$0.65c

CAPEX - $18-$20m

Pay down $20-$25m of additional debt this year, bringing down the total debt for the fiscal year to $190-$195m.

Excess liquidity of 175m after draw down of revolver to pay off 70m loan with an interest rate of 6.44%

Sales:

Marketing strategy

- Internet

- Media

The strategy has been effective, used in a way that supports high quality position.

- Consumers cited the food over the promotion when asked about the advertising

New Dinner entrees, new brunch entrees, being introduced

- Brunch is developing well

Liquor sales

- $5 all day premium cocktail program

- After 9pm, anyone getting a $3 drink gets a free mini

Offering or testing new products throughout this quarter

- Increases guest frequency

- More variety maintains traffic

Goal is to increase check from the $12 area where it is up to $13.50 to $14.50

Compelling value

- Strengthening brand by increasing frequency, trial, average check

- Improving guest experience

- Surveys are doing well, intent to revisit/recommend all well over 90%

- 70% of customers rate the experience as a 5 out of 5

- Large sample size – 250k people

New management structure

- Assistant managers are now either guest service specialists or culinary specialists

- In March, all bartenders received second round of training to help increase bar sales

- Guest satisfaction in the bar is a new survey

- Scores are higher than overall which is encouraging

Turnover levels are in-line with objectives

Questions and Answers:

Q:

How are you thinking about reinvesting versus returning cash to shareholders?

A:

Just got off the defensive and are now on the offensive. First objective is to invest in the business but no great demands right now. In 12 months, give or take, we’ll have the extra cash and make that decision closer to the time

Q:

What’s driving the guest satisfaction? Something relative to what your competitors are doing? The bar? Freshness?

A:

First quarter we’ve tracked bar guest satisfaction…encouraged with the scores. Should be higher than the dining room – higher server to guest ratio. Teams positioned as a premium bar product. Great food products at the bar. Entertainment also, with the big screens etc. Innovation.

Q:

Considering how fast margins have turned, guidance implies that margins have to come back down. Is it initiatives that are going to drive that back down?

A:

Whether it’s food costs, lobster, or extra labor on Saturday nights, during promotions, we will incur more costs. We continue to invest in the brand.

Q:

How have franchisees done in managing costs?

A:

We run better costs than they do

Q:

New company restaurant growth?

A:

Way down the list of priorities. No meaningful emphasis on that. As far as franchising partners where it makes sense, you’ll see some of that but probably in line with the couple per year we’ve seen recently.

Q:

Is there a need for TV advertising to help franchisees?

A:

This year we’ll invest in overmanaging them so they can adopt what we’re doing in the company stores. We have them lag typically, when adopting new programs, to make sure they’re good.

Q:

Food cost experience year-over-year? What kind of deflation in your basket?

A:

Flat on the basket. Our investment has been adding lobster to it. Not seeing decreases. Chicken could be up slightly but it’s a pretty benign market.

Q:

Traffic and check flipped this quarter. You’ve been very traffic focused, can you talk about that?

A:

Tougher quarter with weather. Still beat Knapp Track, still one of the best performers out there. On a two year basis, we continue to improve by 2 points on the second quarter. What we’re spending to drive traffic, and the return we’re getting, is satisfactory.

Q:

What’s the targeted impact on guest experience with new management structure?

A:

Focusing on better food, better service. More focused assistant managers. We’ve gotten as much quality as possible out of the old structure. Now changing to a Capital Grille type structure and that will help us improve quality of food and service.

We’ll also have two managers in the building rather than one. Offset the cost by focusing managers hours only when guests are in the building.

Q:

On the increase in marking dollars in 4Q, is that going to be split between OpEx and SG&A?

A:

All in SG&A line

Q:

Increasing trial and frequency…is frequency up or is the increase just trial?

A:

Frequency has to be up some, we are creating trial too but don’t know the exact numbers. 2.9 visits from those that came in during the 90 days.

Howard Penney

Managing Director