Our call today: new M&A negatives reduce extent of upside potential that we can see at this juncture.

We are bullish on CLDR execution within their standalone platform. The company continues to execute on adding new logos against easy sales comparables. New logos translate to material revenue contribution over the NTM, and then add to net revenue expansion dollars on the following 12 months. Funnel growth is at least a ~24 month virtuous cycle. We also see easier comparisons in the coming quarters off lowered net revenue expansion rates. All of this is bullish.

In the long run, call it 6-24 months, the combination of CLDR + HDP is also bullish. The combination will make new logo capture easier, will add a certain amount of data gravity, with further upside on conversion of HDP to use case value proposition, etc. (CLICK HERE to access the replay of our December Best Idea Long CLDR Call). But in the next 6 months the realities of a weakening HDP business model come into full view, and macro concerns regarding slower Europe/International growth rates will hurt overall growth, which has been supported nicely by international penetration.

Translation (as we had noted from the start): Long CLDR, Short HDP. Can't do that anymore, so patience is needed to transform HDP to productive CLDR asset.

But now the Longs have to get slapped in the face with M&A negatives. Can you handle it? Here goes:

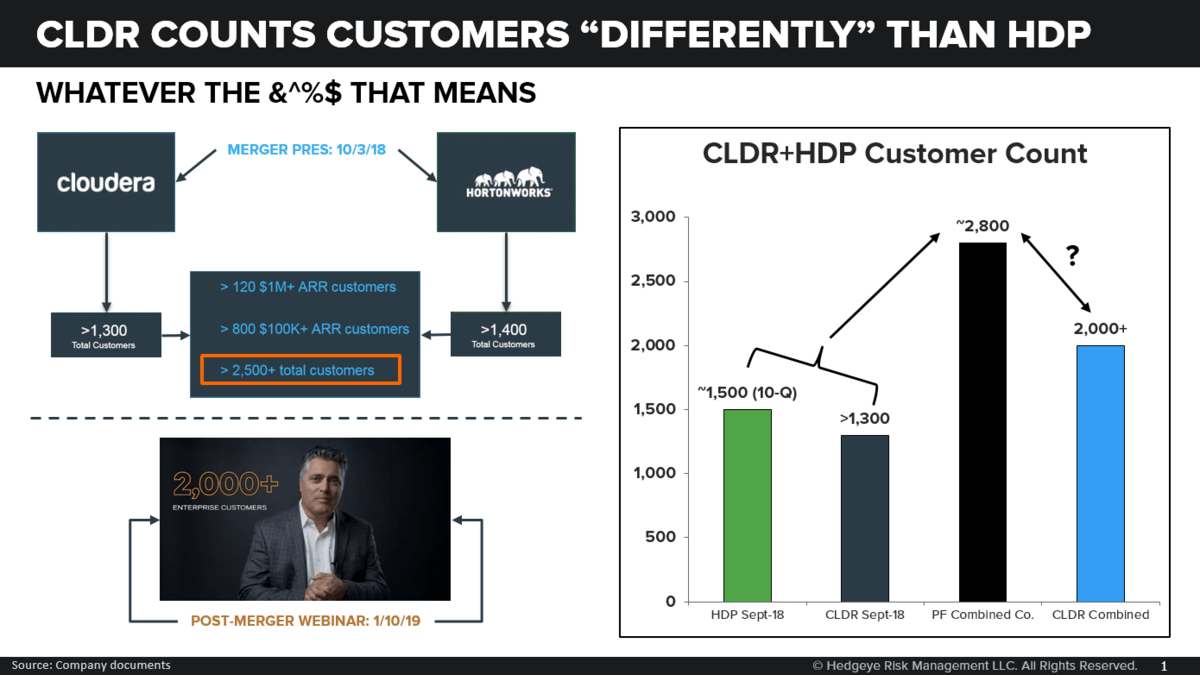

- It turns out that math isn't math when it comes to counting customers. 1,300+ CLDR customers plus 1,400+ HDP customers (as of merger announcement, and 1,500 as of Nov 10-Q filing) does not equal 2,700+ joint customers, in fact it equals 2000+ customers (as revealed in last week's webinar), because CLDR counts customers differently than HDP. Was there some kind of - ahem - problem in counting HDP customers before? This is important because it lowers the range of upside potential on up-selling the combined customer base.

- CLDR just scrubbed down 9mos ending 10/30/18 HDP revenue by $56MM mainly due to crushing down deferred revenue by $177MM ($136MM net, but $177MM gross of the $41MM deferred revenue increase related to the ASC606 to ASC605 backward HDP transition). Yes, using the great power of math, that implies ~$75MM for full year F19 and ~$82MM for F20. Translation: unless you are ready for non-GAAP revenue, expect a disappointment on pre-promised combined F20 revenue guidance. This is important because it puts combined GAAP revenue at ~$890MM in FY20 (CY19). Grow that by your preferred 18-22% growth range and then use 15-20% OCF margins...and you fall short of the promised $225MM of unlevered FCF in F21 (CY20). Yecch.

- The transition of HDP revenue backward from ASC606 to 605 for the 9mos ending 10/18 credited subscription revenue by $6MM and debited services revenue by a similar amount. Which means that when we re-fast forward the tape to F20, you have to take ~$8MM out of subscription and put it back into services. Neutral for revenue, negative for valuation.

- CLDR Co-founder Mike Olson is no longer chairman of the board and in fact is no longer on the board at all. Don’t ya think that should have been disclosed upfront rather than in a filing (HERE) footnote?

- Well-liked HDP CFO Scott Davidson, supposed to be CLDR’s new COO, has resigned and is gone. Disclosure? Lacking.

- Reading between the lines on Mike Olson's message to employees (HERE): "Many of you are naturally curious and concerned about your own jobs […] We're actively looking at ways to preserve jobs where it makes business sense to do so […] In cases where we must terminate positions, we will put reasonable plans, including severance packages, in place to ease the transition for those affected […] Most of you are no doubt targeted by recruiters regularly. I hope that you'll turn down those approaches and stay focused on Cloudera, and on what you're doing for us. Your focus and commitment mean we can better focus on planning quickly, and communicating those plans clearly." Translation: 'please wait until we can fire you. Don’t take any job offers.' This is a reminder that merger integration will be messy for a first-time merging management team.

- Qatalyst got a rich 2% commission for an 11th hour blessing of the model ($34.5MM cash on $1.7B sale of HDP – why?? They did not source this acquisition and were only brought in when the basic terms were already on their way towards finality). This is a reminder that both HDP/CLDR have lived off of VC-monopoly money and are not careful with cash. The transition to self-funding cash growth will not be perfectly smooth.

All this stuff is red meat for the Bears. Good feasting, boys and girls.

For us Bulls we take to heart: a) the positive inflection in new logos captured, b) the increased relevance of CLDR together with HDP in a big data world, c) the upside from HDF into CLDR and cloud data warehouse into HDP, and d) that the stock is unusually cheap for an enterprise growth software company trading in the teens on F21 FCF.

The Bears will further counter that competition in the world of IoT – big data – analytics is heating up and that CLDR is further boxed in by Snowflake, Elastic, Splunk, and others, and that CLDR is busy with M&A execution rather than on beating competition. This is true. But we don’t need a lot of winning for CLDR to be a Long.

Please call or e-mail with any questions.

Ami Joseph

Managing Director

Yosef Vaitsblit

Analyst