Wynn Macau (1128.HK) released its annual audited results on March 24th. There were no surprises but a few interesting tidbits.

While there were no surprises in Wynn Macau's annual filing, there were a few interesting tidbits and details. Below is what we thought was incremental.

- Cash split between the various "WYNN" entities:

- Wynn Las Vegas: $66.4MM

- Wynn Macau: $674MM

- Wynn Resorts: $1,251.4MM (wasn't explicit in the 10K filing since the cash was still at the Cayman subsidiary at Dec 31, 2010. The cash has since been moved to Wynn Resorts)

- Table mix at Feb 10th 2010: VIP: 196 and Mass: 198. Wynn increased their VIP table count by 53 and decreased the number of Mass tables by 30 since 2008. Once Encore opens in April, Wynn will have 233 VIP tables, 222 Mass tables, and 1,200 slots.

- Mentioned the Cotai site but no real update on timing and scope. Only detail was that they have submitted an application on a 52 acre site under their wholly owned sub “Palo Real Estate Company.”

- Junket structure detail: all junkets are on a revenue share agreement and additionally receive a monthly allowance based on % of turnover which they can use towards rooms, food and beverage and other discretionary expenses for their clients.

- Credit exposure: Wynn typically advances commissions at the beginning of each month to provide junkets with working capital. At December 31st, Wynn’s aggregate exposure to their junkets, comprised of the difference between the advances and commissions payable, was HK$127.7MM ($16.5MM USD).

- Wynn’s adjusted EBITDA was $418MM after royalty fees and corporate expenses paid to the Wynn Resorts, but before any preopening or share based compensation. Wynn Resorts reported Wynn’s Macau’s EBITDA as $502MM.

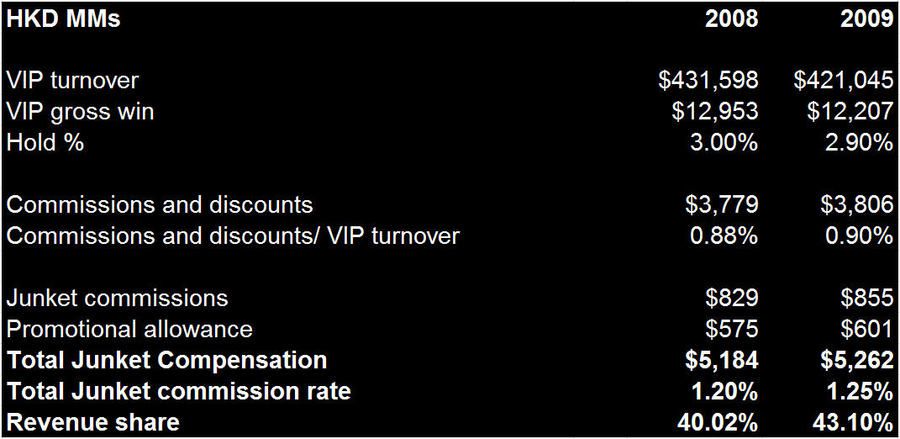

- Junket commissions: Wynn’s all in commission rate was 1.25% or a revenue share percentage of 43.1% in 2009 compared to a commission rate of 1.2% or 40% in 2008. The all in commission rate is calculated as the sum of reported commissions and discounts recorded as a reduction to revenues, junket commissions recorded as an operating expense, and the promotional allowance for non gaming revenues over VIP turnover. Revenue share % is calculated as the commission rate divided by the hold percentage.

- As we've written on several occasions, we are concerned that junket commissions may be headed higher. Commission caps only regulate fixed commissions but not revenue share agreements. We've heard that SJM is being aggressive on this front, albiet using a different franchise model, to go after market share and that MPEL is increasing commissions as it struggles to grow its VIP business at CoD.

- Cash Flow: Wynn generated $583MM of cash from operations (HK$4,517.2MM). Wynn had a large working capital benefit that helped 2009 cash flow.

Below is a summary of Wynn's Macau's valuation and our updated estimates.