R3: REQUIRED RETAIL READING

March 25, 2010

This is the most important company in global (and US) apparel by a long shot. They’re backing off of rev targets, but sticking to EBIT goals. Costs matter more. Inventories rising, sales falling. Chinese labor is more accessable, but more expensive. For those concerned about retail in 2H – this confluence of factors will not ease your fears.

TODAY’S CALL OUT: Why L&F Matters!

First off, most US Consumer/Retail investors we hear from could care less about Li&Fung – at least as it relates to a factor they need to focus on real-time. “Hey, I have a US mandate and can’t buy it, so I’ll save it for weekend reading – at best.” Are you kidding? Think about it like this. L&F generates around US $14bn in sales. That’s the same size as Gap Inc, almost 3x the size of Ralph Lauren, and equal in size to the entire teen-retail specialty apparel space. Of that $14bn, 60% is in the US, with 27% in Europe. But keep in mind that this is not gross revenue at the US consumer level, nor is it gross wholesale revenue, but rather the COGS equivalent for these players. The point is that We’re talking about a company that directly touches between $25bn and $35bn of a $280bn industry. No one else comes remotely close – by a long shot. Even if you can’t buy Li&Fung, pay attention to what they say, and more importantly, what they do.

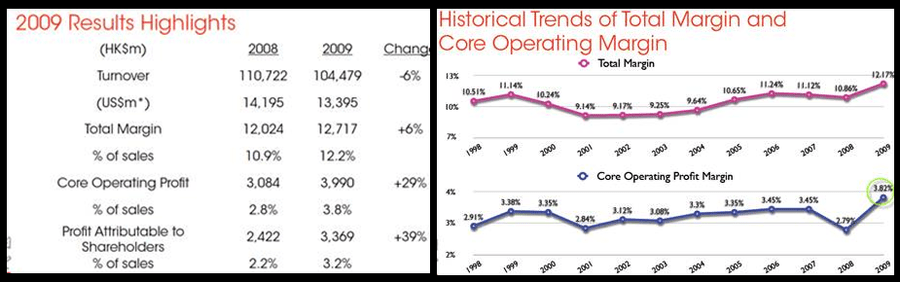

The bottom line here is that last night’s results were not good. Inventories are rising, sales falling. They’re banking on a new deal with Wal*Mart to save the day. They’re also backing off of revenue targets, but are sticking to EBIT goals. That tells me that they’re going to get tighter with costs. Not good. Maybe better availability of Chinese labor will help (a notable Macro point), but out of the other side of their mouth they discuss higher labor costs.

For people concerned about what 2H in retail could look like, this report should not be inspiring.

Here are some details on the print:

Conf. Call Highlights:

- turnover by market, we're still about 60% something for the United States. That hasn't really changed. And Europe is about 27%. And the rest of the world is the balance.

- Turnover by product was still one-third hard lines and two-thirds soft goods. So that hasn't changed much. But with the Walmart deal, I could see that in the future, because I believe the Walmart deal, because of the way their business is - it's slanted towards hard line - that should start to increase the percentage of hard line in our business.

- We expect more than $2b US in shipments in the first full year

Outlook:

- We're expecting the business environment to be increasingly positive. We see a lot of positive signs. Things have changed. I think that when you -- we start to see the numbers in the United States, we're probably coming out of the recession, at least number-wise. We don't expect a double dip. But we're planning our business based on a neutral environment, without going anything more negative, but actually not going more positive than it is today. But the expectation is it will increasingly get better.

- We expect the total year to be flat on inflation.

- We're also continuing to have a number of deals in work. I expect that over the next months ahead of us that we'll be able to announce certain deals. We're focused really on the health and beauty area, footwear, European onshore. And I expect some new deals in the US onshore as well. But I would say just watch this space.

- And finally, on our three-year plan, those targets were formulated in 2007. We're not going away from them. We're committed to it. But I would say that they're challenging. But I would say that there's two targets, $20b top-line target and a $1b core operating profit target. Our focus -- if I had to say, the biggest focus is on our bottom line, basically, for 2010, to get as close as possible to the $1b mark.

Concerns:

- We're watching the US dollar very carefully. We see many issues with the currency. I think it's very volatile against many currencies, including the euro and renminbi and a number of Asian currencies. And that's something that we're managing.

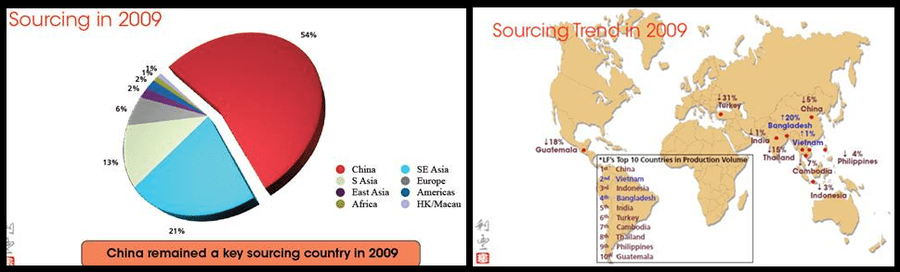

- We're concerned about trade protections between the United States and China. We're watching it very carefully. We think it's real, although we think we're in a pretty good position because of our global network to make changes for our customers if things turn out to be a problem.

- Another area that is -- I think a lot of people have been concerned about is the labor situation in Southern China. I think people have read that there's been a lot of labor shortages. And quite frankly, what we see right now is it's not really a labor shortage anymore. There's definitely enough laborers to go around at the right price. So there is definitely an increase on wages going forward, to get workers. But I think the availability of workers is much better than it was a few months ago.

LEVINE’S LOW DOWN

- It’s good to be a “junior anchor tenant” (15k-60k sq/ft) looking for new locations. According to CoStar, there is currently 200 million square feet representing 8,900 units available for lease across the US. Approximately 75% of the property is actually vacant and about one third of the locations are the result of major closings from retailers including Circuit City, Linen’s ‘n Things, Goody’s, Steve and Barry’s, and CompUSA. While leasing activity is picking up, 72 million square feet of property has been on the market for 22+ months, 79 million square feet for less than a year, and 50 million for 12-21 months.

- In an effort to boost brand awareness and reach new customers, Wolverine World Wide is looking to boost spending on its Merrell brand by reallocating marketing spend. A study by NPD suggests that despite substantial growth over the past decade, Merrell ranks 79th out of 100 footwear brands in terms of brand awareness. The overall awareness number is just 8%. Interestingly, Merrell’s conversion rate ranks second to Nike. Intent to repurchase also ranks number two.

- Given the recent pick-up in sales at PVH’s retail/outlet stores, the company is no longer expecting to close as many as 150 doors over next 4-5 years. Plans now call for closure of 100 to 120 units, or about 20-25 per year for each of the next few years.

- If 3D televisions (which recently hit Best Buy shelves) are going to take off, consumers will need a much bigger offering of 3D content. It appears that Cablevision is trying to take a lead position on 3D broadcasting, with the company airing the first NHL hockey game in 3D last night. It’s no coincidence that the game was between the Rangers and Islanders given that the Dolans control the cable company, the network, and the Rangers.

MORNING NEWS

Indonesia: Govt withdraws technology upgrade scheme for textile firms - Indonesia's Industry Ministry has decided to pull back the subsidy scheme for textile companies to upgrade their machinery due to a lack of interests over the last three years. The cost of manpower was higher in administrating the scheme due to the low number of applicants. However there is still a similar scheme in place and put forward by the Directorate General for Small and Medium Industries offering soft loans to SMEs which intend to replace their ageing machines with new technology and equipment. <http://www.fashionnetasia.com/en/IndustryNews/DailyHeadline/Detail.html?id=1387>

China: The authorities shut down dirty tanneries - The mainland Chinese government has begun the process of forcibly shutting down tanneries that have little or no pollution control. However, tanneries with a low production capacity (less than 30,000 pieces per annum) but have acceptable waste treatment controls are allowed to remain in business. Such actions have shown the Chinese government's goal of irradiating polluting tanneries and moving towards a leather manufacturing sector focused more on high quality as well as high output production. There are approximately 700 tanneries operating in the country which are considered to be medium and large sized operations which have adequate pollution control and turn over more than 5 million RMB (US$732,000) a year. <http://www.fashionnetasia.com/en/IndustryNews/DailyHeadline/Detail.html?id=1386>

China: Textile, garment exports surge 89.3% in February - China's textile and garment export value reached US$12.64 bn in February, up by 89.3% from the same month of last year but down 18.8% month on month. The export value of textile products was US$4.57 bn in February, up 78.2% year on year but down 18.2% month on month. The value of garment exports was US$8.07 bn , up 96.3% from a year ago but down 19.2% from January. In the first two months of this year, the country's exports of textile and garments increased 29.0% year on year to US$28.24 billion in total. As the relatively low base figure in the first half of 2009, a possible appreciation of RMB and higher labor costs, analysts estimated that the exports of textile and garments in the first half of this year will be more than those in the second half. <http://www.fashionnetasia.com/en/IndustryNews/DailyHeadline/Detail.html?id=1384>

Vietnam: Footwear exports reach US$6.2 bn despite February slump - The value of Vietnam's footwear exports edged up in the first two months of the year on an annual basis, but exports for February alone slumped 32.7% month-on-month. The Leather and Footwear Research Institute predicted that the country's leather and footwear exports can increase from US$5.3 bn last year to US$6.2 bn this year. There are more than 700 firms operating in the sector, employing 700,000-750,000 workers, of whom 80% are women. Vietnam ranks fourth globally in footwear exports, selling its products to 50 countries and territories, with the EU, US, and Japan being the main buyers. The main export items are sports, canvas, and leather shoes and sandals. <http://www.fashionnetasia.com/en/IndustryNews/DailyHeadline/Detail.html?id=1382>

Peru: New tanning and footwear industrial park to be built - Peru has officially approved plans to build a new industrial park for leather and footwear in Trujillo in the northwest of the country. Covering an area of 102 hectares, the new facility will house small and medium-sized companies involved in producing leather and footwear. The plan is also to include manufacturers of leathergoods, and to produce leather and finished products to meet the demands of the domestic and the export market. <http://www.fashionnetasia.com/en/IndustryNews/DailyHeadline/Detail.html?id=1385>

Hermes Declines - Hermes International SCA, the French maker of luxury handbags and silk ties, said full-year profit declined as distributors cut inventory.

Hermès International reported flat net profits and beat its initial forecast for operating profits as a recovery in sales in the fourth quarter helped it outperform its luxury peers in 2009. The operating margin fell by 30 bps to 24.2%. <wwd.com/business>

Takashimaya Scrap Merger Plans with H20 Retailing - Japan’s Takashimaya Co. said Thursday it has scrapped its plans to merge with H2O Retailing Corp., the parent company of Hankyu and Hanshin department stores. In 2008, the two retailers announced plans to integrate their operations within three years. The combined group would have rivaled Japan’s largest department store retailer Isetan Mitsukoshi Holdings. It also would have become the latest example of consolidation in Japan’s retail industry, which is struggling with sluggish consumer demand. <wwd.com/business>

Men's Specialty and Independent Stores Struggle - One of the country’s premier men’s specialty stores which has been in business for 101 years, and at one time operated three units, will be closing the doors of its last remaining store permanently. Atributed the closure to the recession. Aggressive promotions from Jos. A. Bank and the Men's Wearhouse make it difficult for independent specialty shops to stay in business. Jos. A. Bank Clothiers Inc. has been running aggressive promotions on suits and dress shirts, even offering the eye-popping deal of buying one sport coat or blazer and getting two pants and two sport shirts free. The Men’s Wearhouse Inc. felt the heat and answered with its own set of giveaways, which have included buy-one-get-one-free deals on suits. According to the National Retail Federation, retailers and restaurants lost more than 470,000 jobs in 2009, which is twice as many people as the entire workforce of the Big Three automakers. And since January 2008, retailers and restaurants have lost more than 1.1 million jobs. The NPD Group Inc. reports specialty stores still account for the largest share of the U.S. apparel business, with 30.8% of the dollar volume share in February, a number that declined from 31.1% of the market in February 2009. But those figures also include the big players such as Men’s Wearhouse and Jos. A. Bank. <wwd.com/retail>

New CEO for Sports Authority - Sports Authority on Wednesday announced the promotion of David Campisi to president and CEO. Campisi succeeds Doug Morton who stepped down from the top position last October, though he remains as chairman at the company. After joining the sporting goods chain in 2004 as president of merchandising, Campisi was named as president and chief merchandising officer in 2005. In his new role, Campisi told Footwear News he planned to refocus the organization around the customer experience and delivering value. “We’ve done a lot of research, and it tells us our customers look not for discounting but for great brands and value,” he said. “We’re also about to launch a new training program for our associates, and you’ll see [the effects of] that in our stores at the end of May. You’ll clearly see a change in style and enthusiasm.” <wwd.com/footwear>

Geox Innovator of the Year - Geox founder and chairman Mario Polegato was named Innovator of the Year Wednesday at the CNBC European Business Leaders Awards.

The panel cited his Italian firm for having broken new ground in developing a “fashionable brand with new technology.” (Geox’s line of men’s, women’s and children’s footwear and apparel focuses on breathable materializations.) <wwd.com/footwear>

WMT is poised to Sell $2 bn of 5-, 30-Year Bonds as Spreads Narrow - WMT may sell $2 billion of 5- and 30-year senior notes, tapping the U.S. bond market for the first time in eight months, according to a person familiar with the transaction. <bloomberg.com/news>

WMT Expands in China - A new wholly owned subsidiary has reportedly been set up by Walmart in Hebei, China, in an effort to further expand and localize its operations. The new subsidiary, according to China's Ministry of Commerce, is an addition to more than 10 others in the country that Walmart began forming in 2009. Those efforts last year supported the opening of 40 new Walmart stores. Walmart arrived in China in 1996, launching a supercenter and Sam's Club in Shenzhen, followed by neighborhood markets. In February 2007, the retailer invested in hypermarket chain Trust-Mart, which operates more than 100 retail units. <licensemag.com>

Fashion Sales rise 6.5% in UK in February - Clothing, textile and footwear store sales rose 6.5% by value and advanced 4.4% by volume in February, the Office for National Statistics reported. <drapersonline.com>

Williams-Sonoma’s web sales fell overall in 2009, but rebounded in Q4 - Home furnishings retailer Williams-Sonoma’s web sales fell 8.4% last year as store sales slumped by 7.7%. But after a Q4 sales upturn, chairman and CEO Howard Lester sees better results ahead in 2010. <internetretailer.com>

Annual web sales rose slightly for dELiA*s, but ebbed in Q4 - Internet sales fared better for dELiA*s in 2009, but declined slightly in the fourth quarter. E-commerce revenue increased 4.1% for the full year, but fell 1.9% in the final quarter. <internetretailer.com>

Web sales were harder to come by for New York & Co. in 2009 - E-commerce revenue and comparable-store sales at New York & Co. declined 2.4% and 11.8%, respectively in 2009. <internetretailer.com>

Staples’ new web site caters to small and medium businesses - Staples Advantage, the business-to-business division of office supplies retailer Staples, has launched a new web site to meet its customers` demands for supplier consolidation and reduced procurement costs. <internetretailer.com>

Blue Nile says a competitor illegally copied its web site product images - Blue Nile has sued Victoria’s Diamonds for allegedly illegally copying photographic images on BlueNile.com. A pre-trial hearing is set for April 26 in federal court. <internetretailer.com>

Tiffany has major e-commerce expansion plans for Europe - Tiffany will begin selling online on the European continent this year, says CEO Michael Kowalski. In the U.S. Tiffany will also begin selling a new line of designer bags on its e-commerce site. <internetretailer.com>

Apparel retailers are still posting the best site response time - Apparel and accessories merchants continue to deliver the best response time to shoppers with a high broadband connection—for the 10th consecutive month, says Gomez, a division of Compuware. <internetretailer.com>

Social Media Making E-mail Marketing More Powerful - In 2009, e-mail marketers started to get social, but 2010 will be the year social media makes e-mail marketing more powerful, according to eMarketer. Social media is a partner, not a threat, to e-mail marketing because it provides new avenues for sharing and engaging customers and prospects. Even though people are spending more time using social media, they are not abandoning e-mail. The two channels can help each other, offering the opportunity for marketers to create deeper connections.