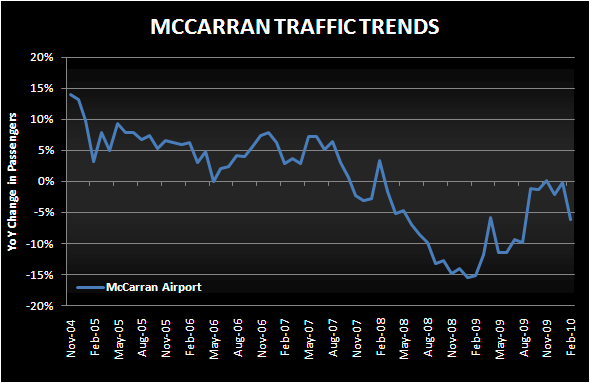

McCarran Airport released bad traffic numbers - down 6.2% in February. However, a Feb CNY and the easiest comparison of the year could contribute to positive growth.

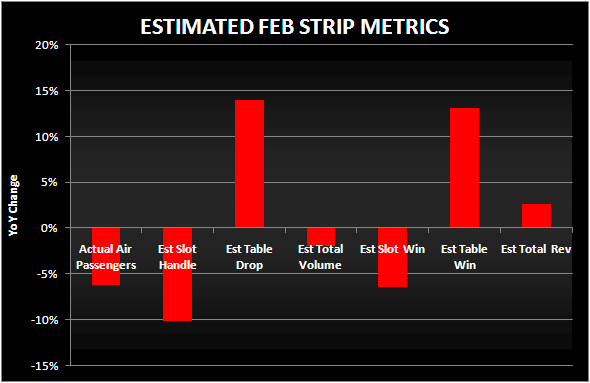

Enplaned/deplaned passengers declined 6.2% y-o-y in February 2010. The comparison was easy as air traffic declined 15.2% in February 2009. Nevertheless, we believe revenue, assuming normal hold percentages, could actually grow over last year.

Due to the shift of Chinese New Year from January last year to February this year, the table game comparison is ridiculously easy. Table drop and revenue declined 37% and 35%, respectively, in February 2009. Slot hold percentage was a little low last year as well, easing the comparison.

In total, we think revenues could grow in the low single digits, again assuming normal table and slot hold percentages. We would caution that due to the inclusion of the Chinese New Year in this month increases the volatility, substantially reducing the predictive power of our model. In any event, we believe revenue growth anywhere near flat or higher will be viewed favorably.