Below are analyst updates on our eight current high-conviction long and short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

UNFI

Click here to read our analyst's original report.

No update to our short thesis on United Natural Foods (UNFI) this week.

We continue to think investors shouldn't be blinded by strong top-line growth driven by Whole Foods representing roughly 37%, because there is immense risk embedded within the margin lines. The company is under pressure to manage operating expenses while gross margins deteriorate, we expect their ability to do so going forward will be challenged by labor costs and capacity constraints (additional capacity not coming until the Fall).

Strong sales performance continues to be dampened by rising cost pressures that we contend will not abate anytime soon, leading to further deterioration of the operating model. Given our bearishness on the independent segment and some other issues UNFI may face going forward, we are not buyers of this new CapEx cycle.

This current and continuing price competitive environment is tough for smaller players (independents represent ~25% of sales) to compete in given their lack of scale versus the larger retailers.

Also, as we've highlighted in recent weeks, we view the SVU acquisition as very troubling, that could cause problems for the company going forward.

SGRY

Click here to read our analyst's original report.

On Friday, Healthcare analyst Andrew Friedman discussed the short thesis on Surgery Partners (SGRY) on The Macro Show. Click here or the image below to watch.

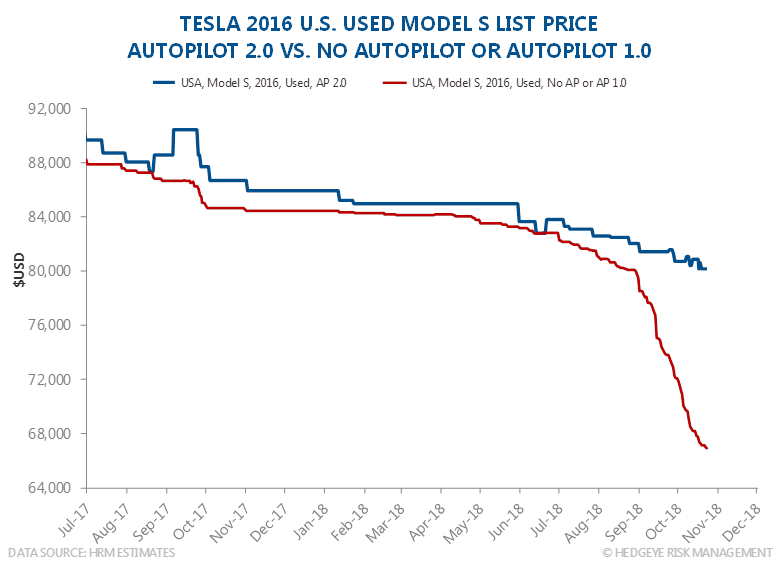

TSLA

Click here to read our analyst's original stock report.

We continue to see evidence that Tesla's (TSLA) brand is weakening given the controversy in the name. Test drive utilization is falling again in our data, and previously impervious Model X used prices have been dropping. A key risk remains the potential for an extension of the EV tax credit, potentially undermining our ‘first loser disadvantage’ downside catalyst.

Below are some key charts based on our research...

DE

Click here to read our analyst's original stock report.

"One of our favorite shorts in our INVESTING IDEAS product (weekend research from my analyst team) remains Deere (DE)," writes CEO Keith McCullough earlier this week.

Why?

In addition to our fundamental short thesis on Deere, we have been bearish on the Industrials sector for much of 2018. Are we heading towards another recession in that sector like the one that hit in 2015 and 2016?

Hedgeye Industrials analyst Jay Van Sciver sees rough going for Industrials, at least over the next 3 to 6 months, partly caused by difficult comps up against the spending spree the sector went on ahead of tax reform.

“There was this expectation in the sector that everybody was going to go out and buy a backhoe for Christmas and expense it and bring their taxes down,” Van Sciver explained in a recent edition of The Macro Show from this week. “That’s not really the way it played out. And now you’re facing much harder comps.”

Overall however, the drop-off does not look like it will be as steep as the one a few years ago – for now.

“We remain data dependent,” Van Sciver says. “Could we see a real blow-up in a more specific sector like the ag space? Sure. But we haven’t seen it yet, and we don’t see a ton of really dramatic downside like in 2016.”

Click here to watch this entire edition of The Macro Show hosted by Van Sciver.

DRI

Click here to read our analyst's original stock report.

The acquisition of Cheddar’s is a problem for Darden Restaurants (DRI)! This is an example of the issues the company faces as the CEO said on the most recent conference call “Dave George, our Chief Operating Officer, will continue to dedicate a significant amount of his time working side-by-side with the Cheddar's team to improve the performance of the business.” Is it a great use of the COO’s time to spend that much time on a small part of the business?

Meanwhile, in the most recent quarter...

- Food and beverage costs were favorable 40 basis points as pricing of 1.9% and continued cost savings initiatives more than offset continued investments in food quality.

- Restaurant labor was unfavorable 70 basis points despite continued productivity gains and sales leverage. The increase was driven by hourly wage inflation of approximately 5%, previously announced workforce investments and headwinds related to mark-to-market expenses for General Manager and Managing Partner equity awards.

- Restaurant expense was favorable 30 basis points as sales leverage more than offset inflation and marketing expense was favorable by 20 basis points.

- Restaurant level EBITDA margin of 18.2% was up 20bps YoY.

FL

Click here to read our analyst's original stock report.

Adidas reported earnings on Wednesday and there are several bearish data points to highlight in relation to Foot Locker (FL).

First, and most notably, is the prioritization of digital sales being conducted through Adidas’ owned channels.

|

“Two years ago, we would do updates maybe monthly or quarterly. Now we do updates, software updates to the site on a weekly – on a daily basis to continue to look upon increasing site speed, making checkout easier.” |

This initiative, being deployed by NKE and ADS is central to our Retail team's long term bear thesis on FL, that over time FL suppliers will continue to move more direct and away from the traditional retail channels (i.e. Foot Locker). Adidas ecommerce was up 76% this quarter! That’s a lot of incremental sales that are being kept by the brand and not shared with retail.

Adidas also discussed on the call the strength in its wholesale partnerships with Kohl’s and Dick’s Sporting Goods as they continue rolling out a greater product assortment with these partners. This was not overly optimistic commentary for FL in terms of where they stand on the list of partners for Adidas given Foot Locker was not even mentioned on the call.

FL reports 3Q earnings on November 20th, we will update you with more information into the print.

MCHP

Click here to read our analyst's original stock report.

Below are some takeaways from Microchip Technology's (MCHP) earnings report:

- Confusing short-term signals as orders re-accelerated in October after the September quarter cleanout of inventory, although some of the October strength might be excess shipment ahead of the feared increase in tariffs from 10% to 25%.

- On the long-term side, no one asked about the lawsuit or the risk that Steve might have to recuse himself from the CEO role. The company is fixing MSCC operationally but the ongoing evidence of excess inventory (over 8 months for high-reliability products) only buttresses our view that real growth for MSCC was even worse organically than the feeble numbers we had scrubbed to. In other words, the point of buying MSCC…is to hurry up and buy another semi company. Steve even noted that his strategy is to buy underperforming semiconductor assets, which is a fine strategy, but does not come with a premium or high performance analog multiple.

- If there is a risk to our Short thesis it probably comes from the s-t signals with maybe a very brief trade into year-end before it collapses in February.

KSS

Click here to read our analyst's original stock report.

An often overlooked risk for Kohl's (KSS) is its exposure to its credit card portfolio.

Kohl’s has its private label credit card partnered with Capital One. Sales through this card account for 60% of the total company’s sales. And the EBIT from the shared revenue and costs of the card partnership equates to about 35% of EBIT or $2.30 in earnings.

The unappreciated risk is that investors don’t realize how much sales and earnings are reliant on the health of the credit cycle. When the credit cycle rolls over (often around the time of a recession) the credit EBIT can easily go down 25-50% or more, meaning EBIT goes down about 10-20% just from the portfolio impact.

Then you have to think about what the impact will be when cardholders accounting for 60% of sales start to default, meaning they have no money to shop.

Since KSS switched its partnership to Capital One from JP Morgan in 2011, the credit quality of cardholders has fallen, so we think there is a material amount of subprime customers that are driving comps today. That means significant comp pressure when the economy weakens.

So in the next credit down turn we think there is a high probability that we could ultimately see KSS EBIT down 25-50% or more, and with the stock at $80 the market is saying that risk doesn’t exist.