Editor's Note: Below is a chart (and excerpt) from today's Early Look written by Hedgeye Macro Analyst Ben Ryan.

|

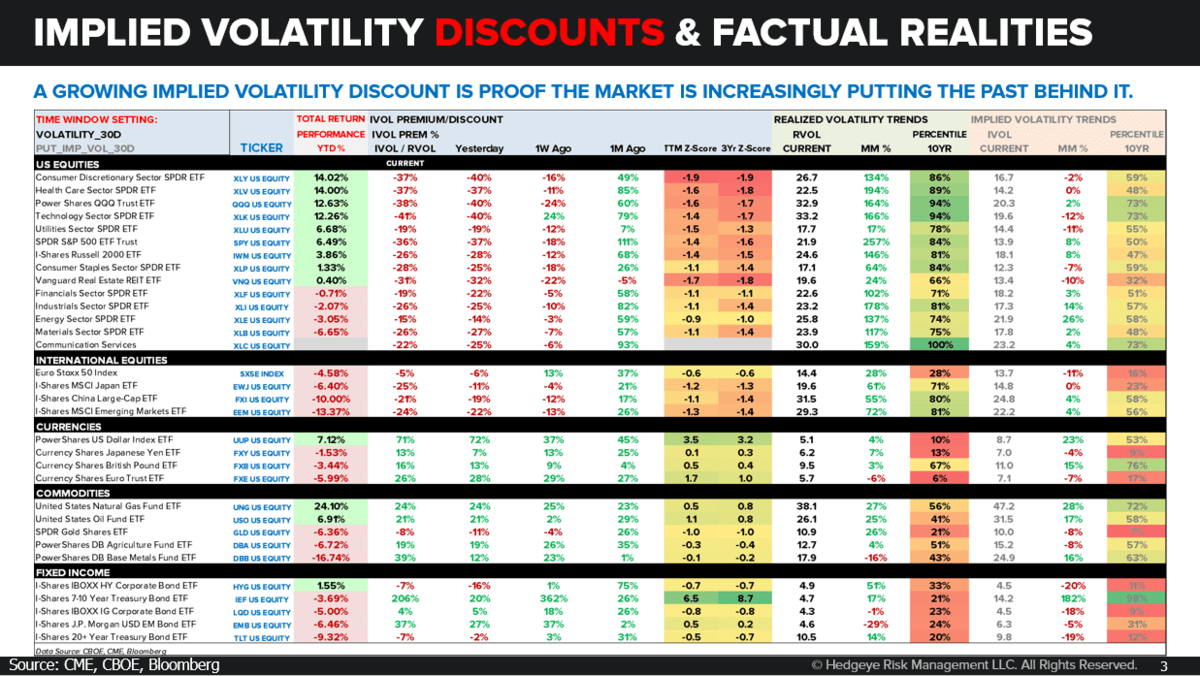

That point is emphasized because it’s exactly what we’ve seen the last two weeks after a very rare environment from a hedging cost and volatility surface perspective. As we show in the Chart of the Day, the U.S. equity market vehicles that:

Here’s What We Know For Sure about the future vs. past comparison gleaned from the widening implied volatility DISCOUNTS: A growing “implied volatility DISCOUNT” is rate-of-change proof that the market is increasingly putting October’s volatility environment in the rearview. |