Last I checked, when a company generates more revenue, profits should go higher. Wayfair didn’t get that memo. This is a classic example of a company growing because it could, not because it should. I can’t justify an $8bn EV – or 3x RH, which is the most defendable model in the Home Furnishings space with the greatest white space. I think management is far better at selling stock than selling furniture, and can’t mathematically get to a point where this company ever earns a red cent. Needless to say, I’m still comfortably short this name even after today’s sell off.

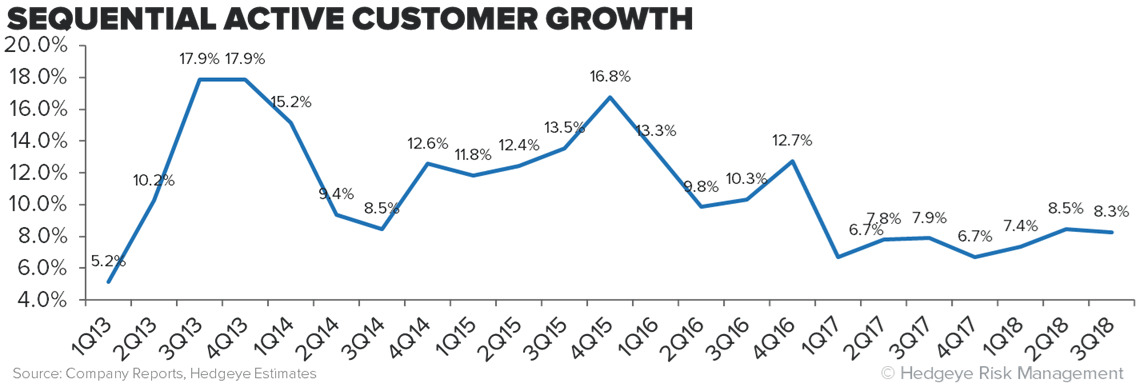

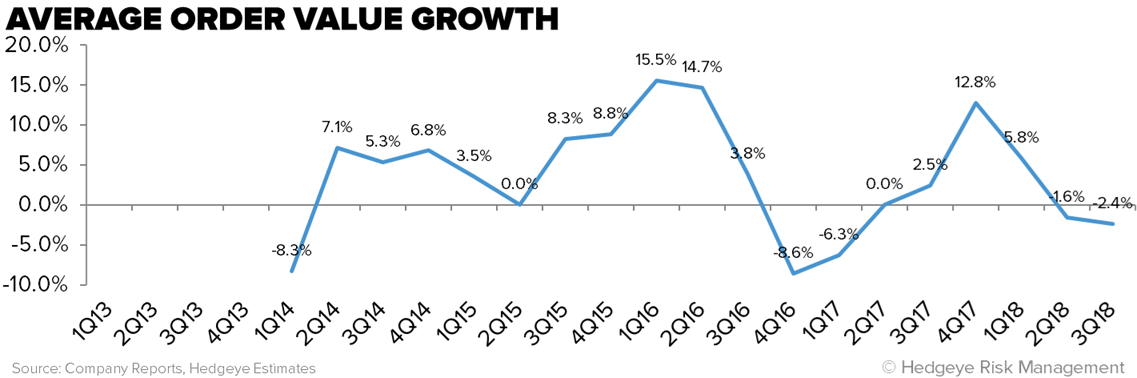

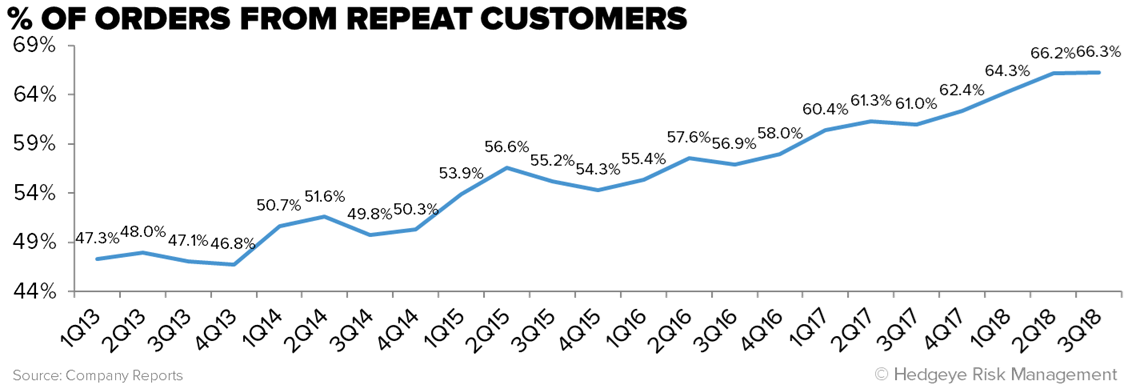

I can’t shake a stick at the customer acquisition metrics…they’re respectable by any means. Is the percent of orders from repeat customers getting frothy at 66%? Yes. But still, revenue growth is like a freight train – clocking in at 43% on top of 39% last year. Slight sequential deceleration from 2Q – but that’s splitting hairs.

The issue for me is that this is a 23% gross margin business with a 27% cost structure. The Gross Margin structure will never improve. Incremental growth is coming from items that increasingly compete with Amazon (note AMZN’s announcement this week of a premium ‘bed in a box’) as well as the Wal-Mart’s, Target’s, Kohl’s, and Bed Bath & Beyond’s of the world. That competitive set won’t lose on price. They cant. Their survival depends on it.

So without merch margin opportunity, it comes down to the cost structure for W. There’s a direct correlation between the rate of SG&A growth and the top line. Add that to the fact that W will ultimately need to either build or acquire a store base. The day SG&A growth slows is the day the top line hits the skids, and we’re looking at a slower-growing business that is structurally unable to ever earn a penny.

Wayfair’s greatest asset is its cash conversion cycle, which is one of the most efficient in retail – cash cycle is negative -- entirely funded by vendors. But at its current size, you need to keep a close eye on whether the vendor network can scale with Wayfair. That’s a tail risk that doesn’t appear to be on management’s radar, but should be on anyone who is comfortable being long this losing business model.