The S&P 500 was little changed on Friday after trading in a relatively narrow range, while volume improved 7% day over day. On the MACRO front, last week ended with mixed signals from the February retail sales (slightly better) and the March University of Michigan Confidence data (disappointing).

On Friday, February Retail Sales were +0.3% vs. consensus (0.2%); ex-autos +0.8% vs. consensus +0.1%. Rising gas and food prices, accounted for nearly 60% of the monthly gain in February sales and over 100% of the revised January sales data. We continue to believe that inflation issues that the consumer faces are real and are supportative of our belief that the FED is behind the curve on its interest rate policy.

The inflation the consumer feels in his wallet is being played out in the lack of confidence. The March preliminary University of Michigan Confidence came in at 72.5 below consensus of 74.0 and a final February reading of 73.6. Despite a 70% move in the S&P 500 since the lows last March, Americans don’t trust the rally.

Despite the stalled confidence figures, Consumer Discretionary (XLY) continues to be the “pain trade.” The XLY was the third best performing on Friday, last week and year-to-date. The better than expected February retail sales helped retail overcome an unexpected drop in confidence and a downward revision in January Retail Sales.

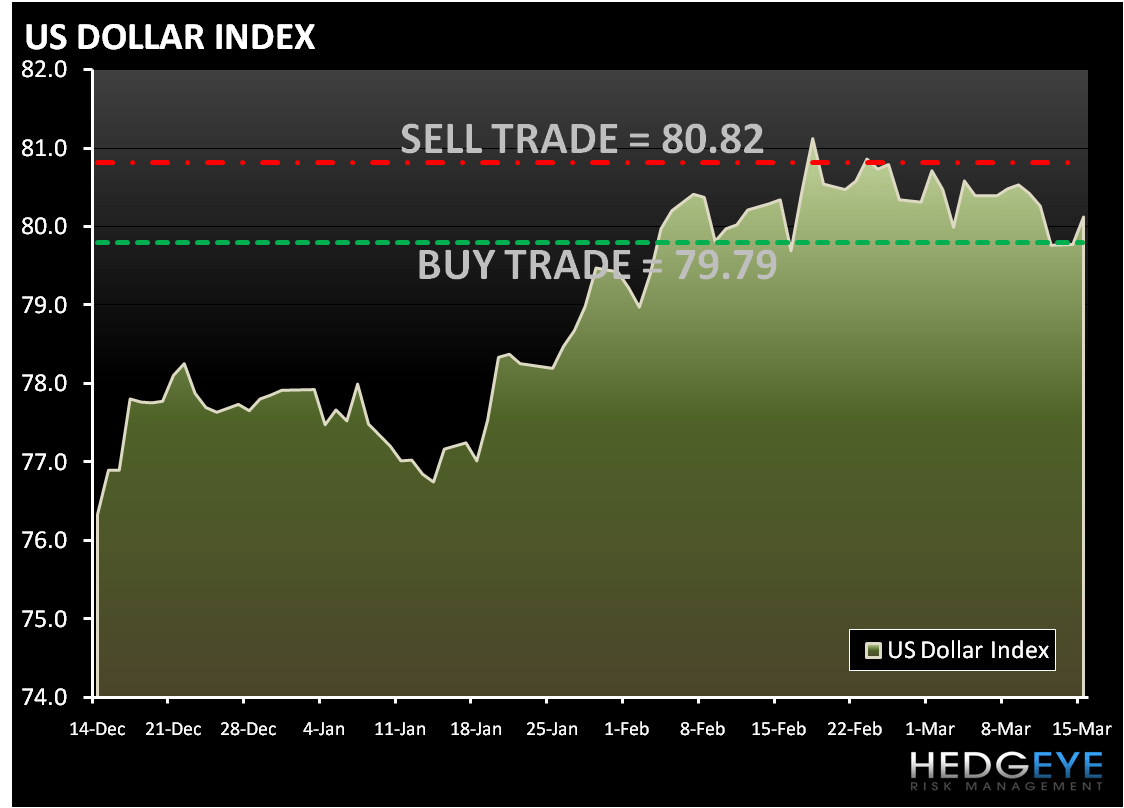

The Dollar index traded down for three straight days last week, declining 0.6% on Friday. The Hedgeye Risk Management models have levels for the volatility Index (DXY) at: buy Trade (79.79) and sell Trade (80.82). Dollar weakness provided a tailwind for Materials (XLB) and parts of the REFLATION trade.

Volatility lost 2.7% on Friday, but gained 0.9% for the week. The VIX continues to be broken on TRADE, TREND and TAIL. The Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (17.10) and sell Trade (19.22).

As we wake up today, equity futures are trading below fair value ahead of a week which includes a number of key MACRO data points on inflation, housing, and industrial production reports and a FED policy meeting. As we look at today’s set up the range for the S&P 500 is 25 points or 1.3% (1,135) downside and 0.8% (1,160) upside.

Today's MACRO highlight will be:

- Empire Manufacturing

- TIC Flows

- US Industrial Production for February

- US Capacity Utilization for February

- NAHB Housing Market Index for March

In early trading, copper is trading lower, extending the decline from last week’s loss on concerns that China will continue to slow growth after inflation rose to a 16-month high. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.23) and Sell Trade (3.39).

Gold is trading higher in early trading higher after hitting a two-week low last week. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,097) and Sell Trade (1,122).

Crude oil is trading lower for a second day ahead this week’s OPEC meeting in Vienna. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (79.57) and Sell Trade (83.10).

Howard Penney

Managing Director