“The love of money grows as the money itself grows.”

-Juvenal

That quote is almost as old as quotes get about money. It’s actually a quote that the WSJ guys used in The Age of Cryptocurrency (pg 120). If you’re going all-in on a “new” currency idea, you gotta go all Roman-poet on people.

Ex-CNBC-guys pumping it at literally every lower-high this year, most people haven’t been losing money during Bitcoin and Ethereum’s 2018 crashes. If you thought having your clients long Emerging Market currencies has been bad, try those alternatives.

At a time and price (more interested in the economic timing as there really is no “fair market value” in our model for either the Brazilian Real or Lite-Coin), I’ll be excited to get long some of these things. That’s probably not happening anytime soon.

Back to the Global Macro Grind…

Did I mention Brazil? The damndest thing happened as Darius Dale and I were going door-to-door meeting with Institutional Investors in New York City yesterday. Some people were simply not happy that we remain bearish of Brazil.

So I got in the car and reviewed why so many hedge funds got pro-cyclically long of Brazilian Credit and/or Equities during 2017 and the double-damndest thing became glaringly obvious in our 4 quadrant GIP (Growth, Inflation, Policy) model:

- Brazil’s economy was in either Quad 1 or Quad 2 for a record 8 straight quarters going back to 2016

- Brazil’s economy slowed into Quad 4 in Q1 of 2018 (stocks collapsed)

- Brazil’s economy is now trending in Quad 3 (and her currency is crashing)

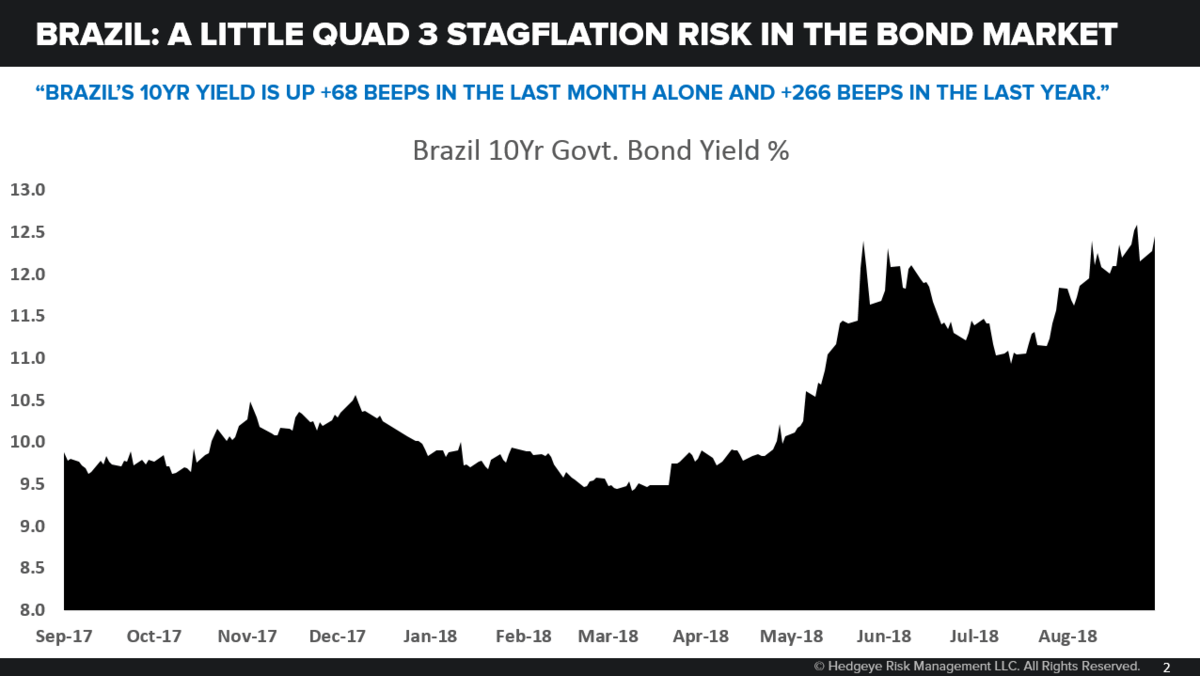

Amongst other things, if you’re looking at a multi-country (multi-factor) and multi-duration dashboard of rate of change risk this morning, you’ll note that the only major country 10yr Yield that is UP by more than a few beeps is Brazil’s.

You see, Brazil’s 10yr Yield ramping +9 basis points (beeps) to 12.51% this morning isn’t a new @Hedgeye TREND. Brazil’s 10yr Yield is up +68 beeps in the last month alone and +266 beeps in the last year.

This is precisely what happens to a cross-asset class country exposure when Mr. Market starts to front-run trending Quad 3 economic data. Quad 3 is also commonly called Stagflation. That’s when:

- Your currency is crashing

- Inflation is accelerating in that local currency

- Real consumption growth slows (so real GDP slows)

Some hedge fund PMs can get mad at my forecast or stop losing money by understanding it. The high probability economic scenario in our Brazil GIP Model is that Brazil is in Quad 3 (stagflation) for 5 quarters (starting Q218) in a row.

I get that people get upset when they are losing money. What I don’t get is some people getting so upset that they stop learning what made the people on the other side of the trade right. Rather than getting mad, why not get smarter?

Imagine I walked into every meeting (and we do a lot of them!) just downright mad at dine-and-dash compensation cuts we’re getting from some “because of Mifid 2”? I don’t get mad. I just focus on innovating, taking share, and moving up the ranks.

Moving along…

Shorter-term another way to lose money was to short the NASDAQ:

- AFTER it went down for 6 straight days …

- Towards the low-end of the @Hedgeye Risk Range

- Registering an implied volatility PREMIUM (vs. 30-day realized) of +69%

Remember, I was born and raised as a short-seller on the buy-side. Oh do I want to short Tech (haven’t done it in years!). But I don’t want to lose all my money shorting it at the wrong spot!

What a difference a 1-2 day bounce makes in terms of risk re-pricing in futures and options terms: Tech’s (XLK) implied volatility PREMIUM just got smoked from +69% to +13%, in a day.

The other big thing in my PRICE, VOLUME, and VOLATILITY model that jumps off my notebook page this morning is that Total US Equity Market Volume (including dark pools) was DOWN -12-13% on the 2 days of the SP500 bouncing from #oversold lows…

So, we’ll see where the sellers come back first on #accelerating volume. USA vs. Brazil? I’m betting it’s Brazilian stocks and currency more so than in US stocks and US Dollars. We’ll see if that’s right.

Across durations, my #1 goal in risk management remains not to be losing money when the crowd is. If more macro hedge funds had been short of EM, Brazil, and Bitcoin in 2018, some new client prospect meetings would be a lot happier!

Our immediate-term Global Macro Risk Ranges (intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.83-2.98% (neutral)

SPX 2 (bullish)

NASDAQ 7 (bullish)

Utilities (XLU) 53.00-54.98 (bullish)

VIX 12.02-15.34 (bullish)

USD 94.35-95.79 (bullish)

EUR/USD 1.15-1.17 (bearish)

Oil (WTI) 66.88-70.95 (neutral)

Gold 1190-1211 (bearish)

Bitcoin 5 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer