“Being invited once doesn’t mean you get to come back.”

-John Feinstein

That’s how Feinstein explains the ground rules of being invited to weekly lunch at the China Doll with one of the greatest coaches in pro basketball history, Red Auerbach. If you haven’t read Let Me Tell You A Story, I recommend it – best book I read on vaca.

Ironically enough, a New York City client gave me the book (I think he was tired of me writing about hockey). While Auerbach was from Brooklyn, NY, his 9 NBA Championship titles came as the Head Coach of the Boston Celtics.

Since I’m in Boston for Day 2 of meetings with Institutional Investors today, I’m feeling the Beantown love this morning. This is one of my favorite cities to do business. You don’t get invited back if you don’t call it like it is and make/save people money.

Back to the Global Macro Grind…

Buy US Treasuries? Yep. That’s the call I’ll be spending the next 2 days making. Boston isn’t exactly the town of bond kings btw. Fully loaded with some of the biggest Emerging Market Bulls in the world, this is one of the epicenters of Global Equity investing.

Since I’m asset class and investing style agnostic, I’m cool with that.

In fact, teaching myself how to buy the right exposures (and get out of the wrong ones), across Global Equity markets, when I’m bearish on growth and/or inflation is one of the most important things I’ve learned in the last decade.

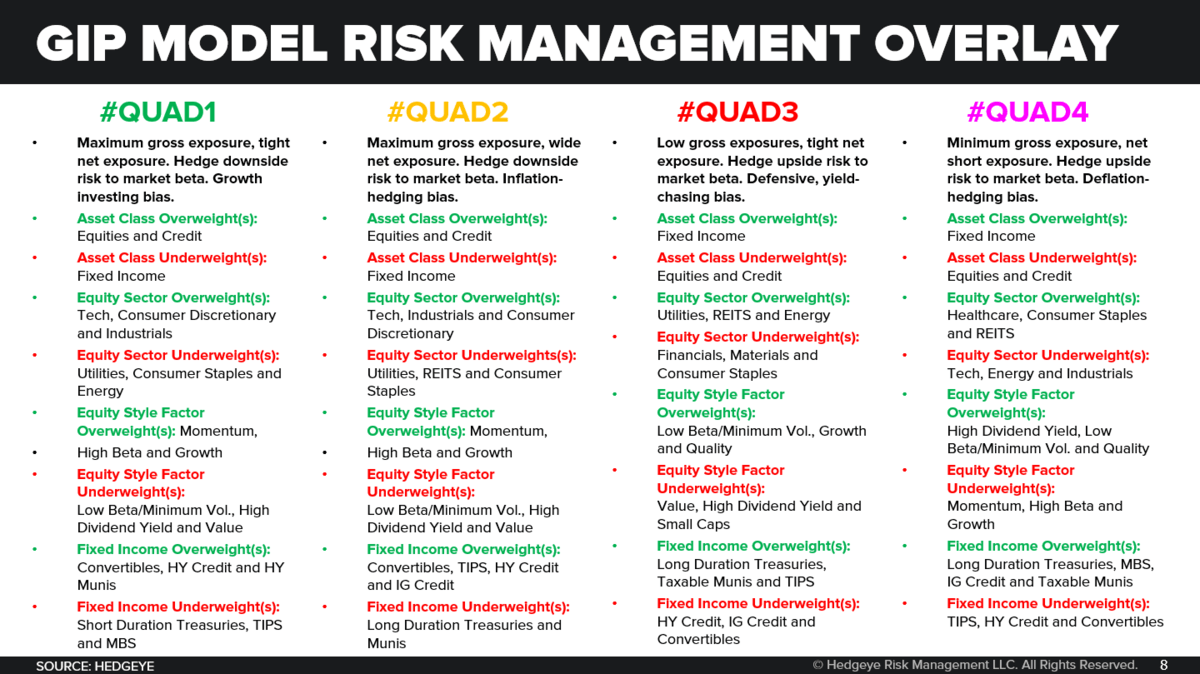

Put simply, when an economy is headed into Quad 3 or 4, we always have a slice of an equity market we like.

We also have slices and sub-sector exposures we don’t like! I’m not going to spend the rest of this note reiterating our #StrongDollar call and/or our under-weight (short) Emerging Markets views. I’m going to reiterate short US Financials (XLF).

In Quad 3 in particular (economic stagflation), here’s one of the most important stocks vs. bonds tilts:

- Long long-term US Treasuries (TLT)

- Short Financials (XLF)

There are, of course, equity tilts within that top-end tilt, which include being long Bond Proxies in the equity market like:

- US REITS (VNQ)

- Utilities (XLU)

No, that setup didn’t work yesterday. And no, it didn’t work for the better part of the last year mainly because the US economy wasn’t in Quad 3 – it was in Quad 2.

As a reminder on #process (Auerbach had awesome #process btw):

- Quad 2 = rate of change (TREND duration) of growth and inflation #accelerating

- Quad 3 = rate of change (TREND duration) of late cycle inflation #accelerating; real growth #slowing

Since we’re going to get what we think will be the peak of USA Quad 2 on Friday (our headline GDP forecast = +3.73% and it can easily be higher than that) I know what the risk is of being early in shifting from Quad 2 to Quad 3.

There’s a bigger risk of being late!

I don’t come to Boston to make day-trading calls (if someone wants me to help them risk manage ideas within the immediate-term @Hedgeye Risk Range, I’m happy to do so). I come here to lay out our views of major economies for the next 6-12 months.

On that front, “let me tell you a few stories”…

- European Stocks (especially “cheap” Financials) – if you bought them 12 months ago and shorted “expensive” US growth exposures against them, you got crushed

- Emerging Market Stocks – if you bought them alongside the consensus crowd 6 months ago and kept shorting US Dollars for the last 3-6 months, you got crushed

One of my goals in starting this firm wasn’t to “nail the quarter” on Netflix (NFLX) and Google (GOOGL). If my analysts do that, great. For me, the most important thing is helping CIOs, PMs, etc. get out of major macro exposures before the consensus does.

Do I get why the biggest Consensus Macro position of short US Treasuries (across durations) remains? I hope so. I’ve only be writing about it for the last 7 going on 8 quarters (a new US record of consecutive Quad 1 or 2 = #GrowthAccelerating).

Does Consensus Macro get that headline US inflation should drop at least 100 basis points (in year-over-year rate of change terms) from the July-Aug 2018 peak to Q1 of 2019? I don’t think so.

Otherwise I wouldn’t be the only one with a Buy US Treasuries headline in your inbox from Boston this morning.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.78-2.97% (bearish)

SPX 2 (bullish)

NASDAQ 7 (bullish)

REITS (VNQ) 80.38-83.01 (bullish)

Industrials (XLI) 72.47-75.08 (bearish)

DAX 122 (bearish)

VIX 11.60-14.61 (bearish)

USD 93.90-95.25 (bullish)

Oil (WTI) 66.36-71.52 (bullish)

GOOGL 1186-1275 (bullish)

NFLX 343-385 (bullish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer