“Learn from yesterday, live for today, hope for tomorrow. The important thing is not to stop questioning.”

-Albert Einstein

Yesterday, I was forwarded an article from a subscriber that made the statement “Politicians are the only people in the world who create problems and then campaign against them.” The author of that article and Albert Einstein are right: “we can't solve problems by using the same kind of thinking we used when we created them.” Therein lies a structural problem we need to deal with. Washington has dug a very big hole and there is no real insight on how to deal with the issues, and now the politicians and Washington’s “groupthink” is begetting speculation that is potentially unhealthy.

For the third day in a row the S&P 500 moved higher by 0.23%. While volume was up 10% day-over-day, it was an uneventful day given the light MACRO calendar. Some MACRO headwinds subsided as another round of austerity measures in Greece is making headlines. Greek Prime Minister George Papandreou announced an additional $6.6 billion of deficit cuts as he tries to appease the balance of the EU.

Additionally, the year-long M&A tailwind is gaining momentum, which is now includes takeover speculation rumors, coupled with an increase in shareholder activism dividends and share repurchase programs. Auto sales also provided a positive tone to the market.

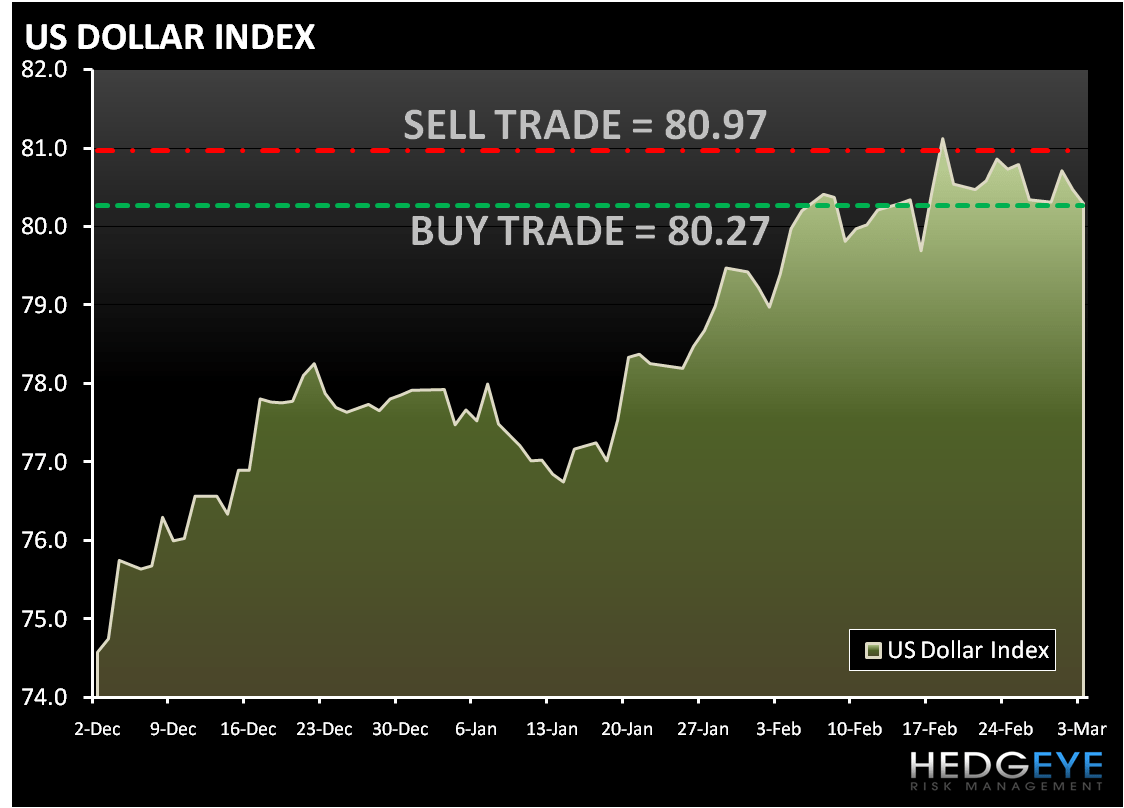

The REFLATION trade popped up yesterday, as there were a number of positive developments in the Materials (XLB). First, the dollar index declined following some early strength. Today’s set up of the Hedgeye Risk Management models have levels for the Dollar Index (DXY) at: buy Trade (80.27) and sell Trade (80.97). Second, the fertilizer group was underpinned by talk of a 15% export tax on potash in Russia. Gold and steel stocks also outperformed. The VIX declining 1.0% yesterday and today’s setup of the Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (18.68) and sell Trade (21.88). The VIX continues to be broken on all three durations – TRADE, TREND, and TAIL.

The two worst performing sectors yesterday were Consumer Discretionary (XLY) and Technology (XLK). Yesterday, retail saw a four-day winning streak snapped with the S&P Retail Index declining 0.8%. Helping to drag down the sector was SPLS which was down on a Q4 miss and conservative guidance. DPZ was a bright spot in the restaurant space on better-than-expected Q4 earnings and revenues, while DENN was up on the back of shareholder activism.

While we continue to be long technology, there was no follow thru following Monday’s performance. The semi group was unable to build on Monday’s rally, as the SOX was flat on the day. We are also long the Financials (XLF), which only slightly outperformed yesterday. After underperforming on Monday, the large-cap regional banking was stronger on the day with the BKX (0.7%).

As we wake up today, Equity futures are trading mixed to fair value having pared back gains from yesterday with Greece having unveiled additional austerity measures. On the calendar today we have:

MBA Mortgage Apps

February Challenger Job Cuts

February ADP Employment Change

Feb ISM Non-Manufacturing composite

Fed Beige Book

After the close last night the ABC consumer confidence number rose slightly to -49 from -50. As we look at today’s set up the range for the S&P 500 is 25 points or 1% (1,107) downside and 1.0% (1,122) upside.

Copper, is little changed in early trading, although there continues to be reduced concern about potential disruptions to supply in the wake of the earthquake in Chile. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.30) and Sell Trade (3.43).

Gold is trading near a six-week high and may get further support after Greece’s government passed new austerity measures and a weaker dollar. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,120) and Sell Trade (1,135).

Crude oil is trading quietly in the AM before the Energy department’s report that will likely show that crude inventories expanded for a fifth week in the U.S. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (78.09) and Sell Trade (80.77).

Howard Penney

Managing Director