We have enjoyed reading “This Time is Different” by Carmen Reinhart and Kenneth Rogoff. In fact, we have often quoted the astute historical studies in this book over the past quarter. That said, we were taken aback by some recent statements by Kenneth Rogoff. According to Bloomberg:

“China’s economic growth will plunge to as low as 2 percent following the collapse of a “debt- fueled bubble” within 10 years, sparking a regional recession, according to Harvard University Professor Kenneth Rogoff.”

In the hypothetical everything is of course possible, but what is concerning about this prognostication is that it does not seem to be based on any of Rogoff’s fine quantitative studies. By making this statement, Rogoff is suggesting that Chinese growth decelerating to a level of 2% is in the realm of real possibility.

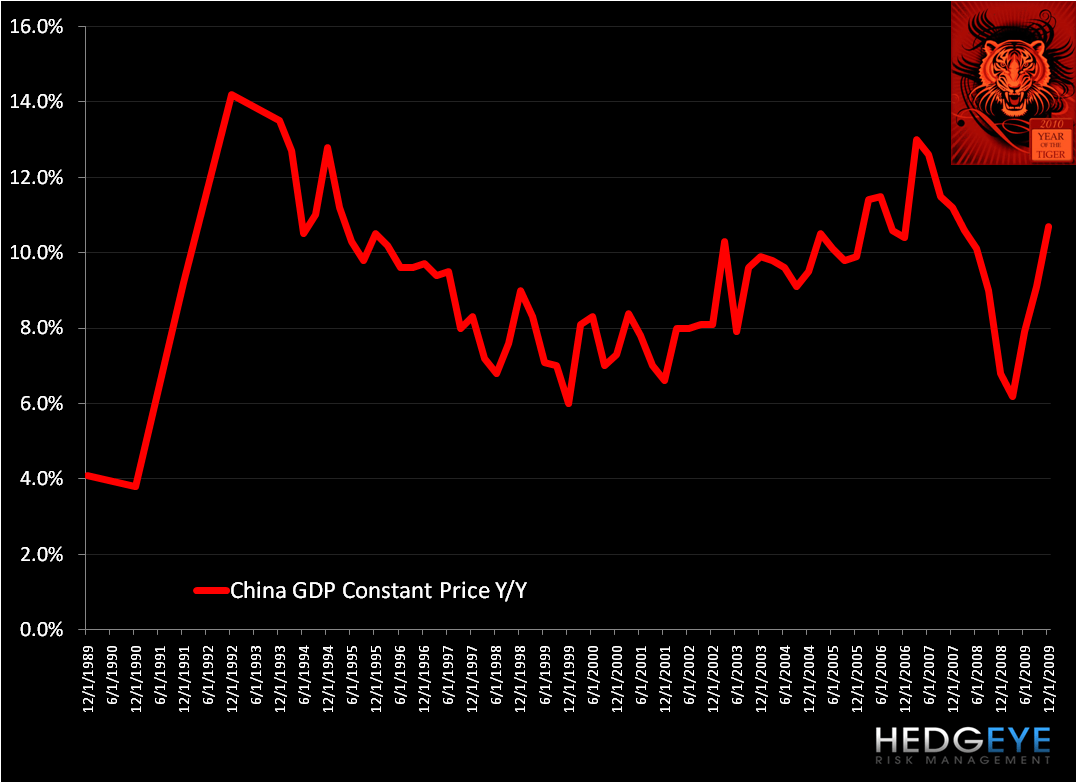

Below we’ve charted Chinese GDP growth over the past 20-years. The story from this chart is actually quite simply that a deceleration to of GDP growth to 2% would be way out there on the tails of probability. While certainly not impossible, Rogoff’s statement reeks more of that of fear mongering than an accurate assessment of probability. Over this time period, China’s GDP has average 9.2% and the range has been between 3.8% and 13.5%. So 2% . . . possible, but probable? We aren’t so sure.

In terms of context, it is also critical that this period of Chinese growth includes a massive debt bubble. In fact, according to Reinhart and Rogoff, in the late 1990s:

"China's four large state owned banks, with 68% of banking system assets, were deemed insolvent. Banking system nonperforming loans were estimated at 50%."

So, despite the Chinese financial system basically being insolvent in the late 1990s, Chinese GDP never dipped below 6%!

We certainly mean no disrespect to Professor Rogoff, but as we have found, and not dissimilar to his analysis of rating agencies, when academics start to call the markets, it is more often than not a contrary indicator. Not a shot at Rogoff, but just a fact of reality. Timing is everything in this business.

Daryl G. Jones

Managing Director