Google recently introduced YouTube Music, a paid subscription service that allows users to stream songs, make playlists, and play music videos ad-free and on demand. This move indicates that Google is out to claim a bigger share of what’s turning into a crowded space. Currently, the service to beat is Spotify, which leads the pack in paid subscribers and is the service of choice for young listeners. Yet Spotify still hasn’t figured out how to make streaming profitable—an issue fundamental to these services’ survival. Even as streaming continues to transform the way that people listen to music, the economics at work may mean that only a tech powerhouse with diverse revenue streams can afford to keep it going.

In a few short years, streaming has become the lifeblood of the music industry. According to the latest annual report from the Recording Industry Association of America (RIAA), revenues from recorded music increased 17% in 2017 for the second year in a row; most of that growth was attributable to paid music subscriptions. Streaming—a category that includes both subscription services and free, ad-supported options—is now the largest source of music industry revenues (65%), far exceeding physical sales (17%) or digital downloads (15%). Though total revenue remains a fraction of its peak two decades ago, the rise of streaming has been a balm to an industry that for years saw only declines.

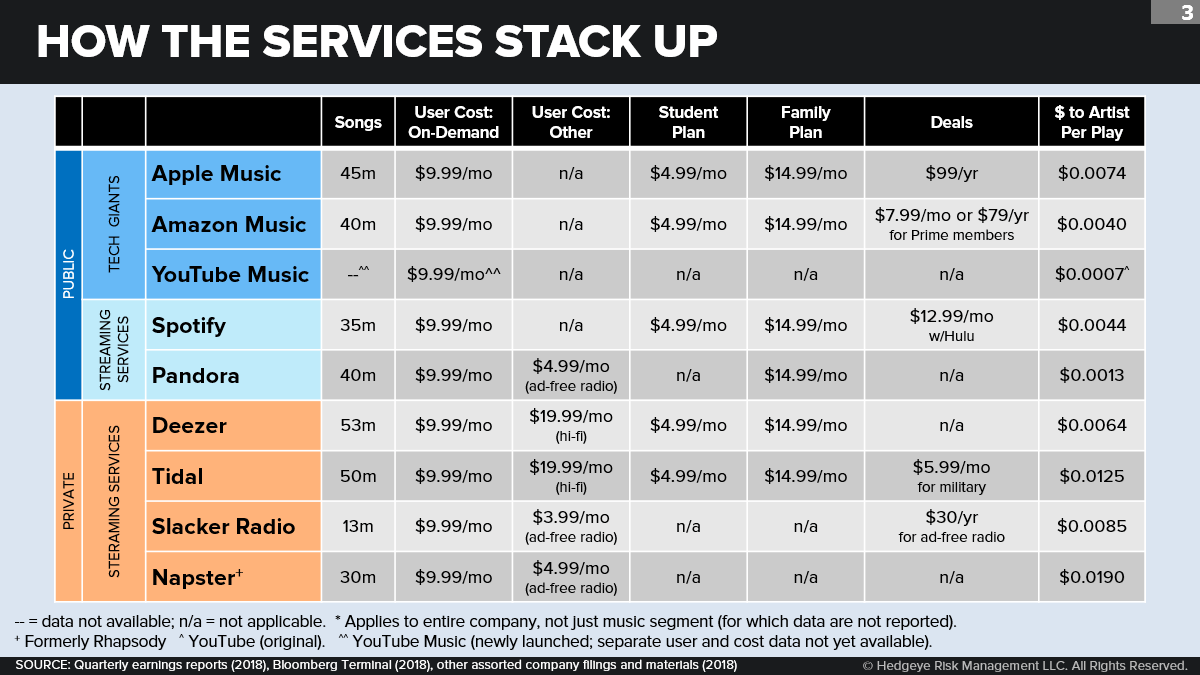

As streaming has surged in popularity, so has the number of companies that have stepped in to offer their own services. Among the rivals to YouTube Music are Spotify, Apple Music, Pandora, Amazon Music, Tidal, Deezer, Slacker Radio, and Napster—and that’s just for starters. But consumers may have a hard time telling them apart, because the plans they offer are largely the same. Some focus on radio and others on-demand streaming; some let users listen for free with ads. But all provide the same core paid service: unlimited streaming with the ability to create playlists and radio stations, as well as listen to songs offline for $9.99 a month.

So where does each service stand out? YouTube Music and Pandora claim to have the best recommendations. YouTube Music selects songs based on Google’s considerable trove of user data; it will also suggest music based on your location. Pandora has its famed Music Genome Project, which it plans to recreate for podcasts. Spotify plays on the widest variety of devices and focuses the most on social features. Tidal and Deezer tout the highest audio quality. Amazon and Apple, meanwhile, make it easy for listeners who own their hardware to enjoy seamless playback. Apple Music, for instance, is the only streaming service that works on the company’s HomePod speaker.

Though the competition in paid streaming is fierce, there’s a clear frontrunner: Spotify. As of May 2018, the company had 75 million paid subscribers and a total of 170 million monthly active users. Coming in second is Apple Music with 40 million subscribers. To be sure, these aren’t exact comparisons: Many of these services aren’t available in the same countries, while others haven’t disclosed their subscriber numbers. Spotify also isn’t the most popular source for music streaming overall; that’s the free version of YouTube. Paid subscriptions, however, generate much higher revenue per user—and, over time, ad-financed content tends to be driven downmarket.

Yet even though Spotify rules the industry, it’s not profitable. That’s because the cost of music licensing is so high and will continue to be as the company grows. Furthermore, unlike Big Tech, Spotify can’t afford to compete on pricing. It’s no coincidence that the two companies offering the deepest discounts on streaming are Amazon and Apple. And with Google trying again to enter this space, Spotify is facing another competitor with unmatched negotiating power and money to burn. In order to become profitable, it needs to either cut its music costs or pursue other sources of revenue. The company has started offering advances to indie artists and managers who license their music to Spotify directly—the first sign it may have long-term ambitions to produce content, Netflix-style.

What role might generational preferences play in Spotify’s ability to maintain its lead? The data are mixed. On the one hand, according to the RIAA, Millennials are only slightly more likely than their parents to stream music—but they’re twice as likely to be paid subscribers. And among Millennials who subscribe and those who would consider it, Spotify is the most popular choice. A 2016 study from Northwestern University found that when it comes to music discovery, young people most value convenience, lending support to Spotify’s strategy to be available on as many platforms as possible.

On the other hand, current or would-be subscribers may always be outnumbered by free listeners. According to the Northwestern study, young people are still most likely to discover music the old-fashioned way: through recommendations from friends or FM radio. In fact, the most popular sources among Millennials for new music are YouTube, Pandora, and FM radio. Discovering music through Spotify-centric routes, such as shared playlists, is less common. Free options are still seen as the most accessible and convenient to find and listen to music—though this may change. Both Pandora and YouTube are experimenting with higher ad loads in an effort to effectively annoy people into subscribing.

Whether paid or free, Internet radio or on-demand, there’s no question that streaming has become the new standard for the industry. The records and CDs that Silent, Boomers, and Xers stockpiled as youth have been replaced by digital libraries. With this has come a shift toward breadth over depth: Listeners are now able to sample music of all genres widely and quickly, creating an environment in which young people can invest much less energy into a single artist than Boomers did.

Millennials have given rise to many “one-hit wonder” bands: They care less about a vocalist’s ideology or worldview (a Boomer obsession which once fueled “big album” purchases) than they do about how a single song sounds. They care less about witnessing a performer’s artistic virtuosity live than they do about simply hearing his or her music—or, in the case of an on-stage EDM computer—its music.

The new normal leaves the industry at a crossroads. There’s more music at our fingertips than ever before, but much less money to be earned from selling it. And unless Spotify and its ilk can close the gap, streaming’s reign may end as quickly as the era of digital downloads did. Keep in mind that any tech giant could easily move to gain strength in this area if it wanted to; a small but well-regarded player like Pandora, or even a big fish like Spotify, is within reach. The fact that none has suggests that these companies don’t see a bright future there. But Spotify is determined to prove them wrong.

TAKEAWAYS

- Streaming may be the future of music—but the winner is no lock. Google’s latest streaming effort comes at a time when streaming has taken over as the music industry’s main growth driver. The space has become crowded in recent years, leaving consumers to choose between several homogeneous services. As the largest and most user-friendly on-demand streaming service around, Spotify is the unquestioned leader of the space. But its lead is not safe. Yes, streaming is undoubtedly the new norm, especially for Millennials who prefer breadth over depth. But a tech giant with other complementary revenue sources may be best-equipped to carry the format into the future.

- Tech giants pose the greatest threat to Spotify and Pandora. The conquest of streaming would constitute a modest but attractive extra jewel in any FAANG portfolio. But massive cross-subsidized competition from these giants would spell ruin for Spotify and Pandora. Think this scenario is unlikely? Take note: The big tech companies are already undercutting streaming companies on price. Apple Music offers a $99/year deal, considerably cheaper than 12 months’ worth of a paid Spotify or Pandora subscription (both would set you back $120). Amazon, meanwhile, offers its music service to Prime members for just $79/year. Although Spotify CEO Daniel Ek isn’t too concerned about the competition, investors should be.

- Spotify remains the streaming service to beat—for now. With a market capitalization $31 billion and a userbase of 170 million, Spotify is the biggest pure-play public streaming company. Spotify’s main strengths are (1) its early prioritization of on-demand music, which has driven its rapid subscriber growth; (2) its newly overhauled free-tier on-demand, which feeds the ranks of paid subscribers; and (3) its seamless ease of use across a multitude of platforms. While some analysts have urged Spotify to drop its free tier in order to improve margins and royalty rates, the service owes much of its success to its low barrier to entry.

- But Pandora may be the better long-term play. If you think a FAANG streaming takeover is inevitable, then you might be wise to go long Pandora and wait for the eventual buyout. Currently, there’s no talk of acquiring the service; the closest Pandora has gotten to acquisition was a $480 million investment from Sirius XM last year. Yet considering how closely it now resembles Spotify in features and how much the company is undervalued ($25 per Pandora user versus $162 per Spotify user!), purchasing Pandora may just constitute the cheapest and fastest means to acquire major market share.