THE HEDGEYE EDGE

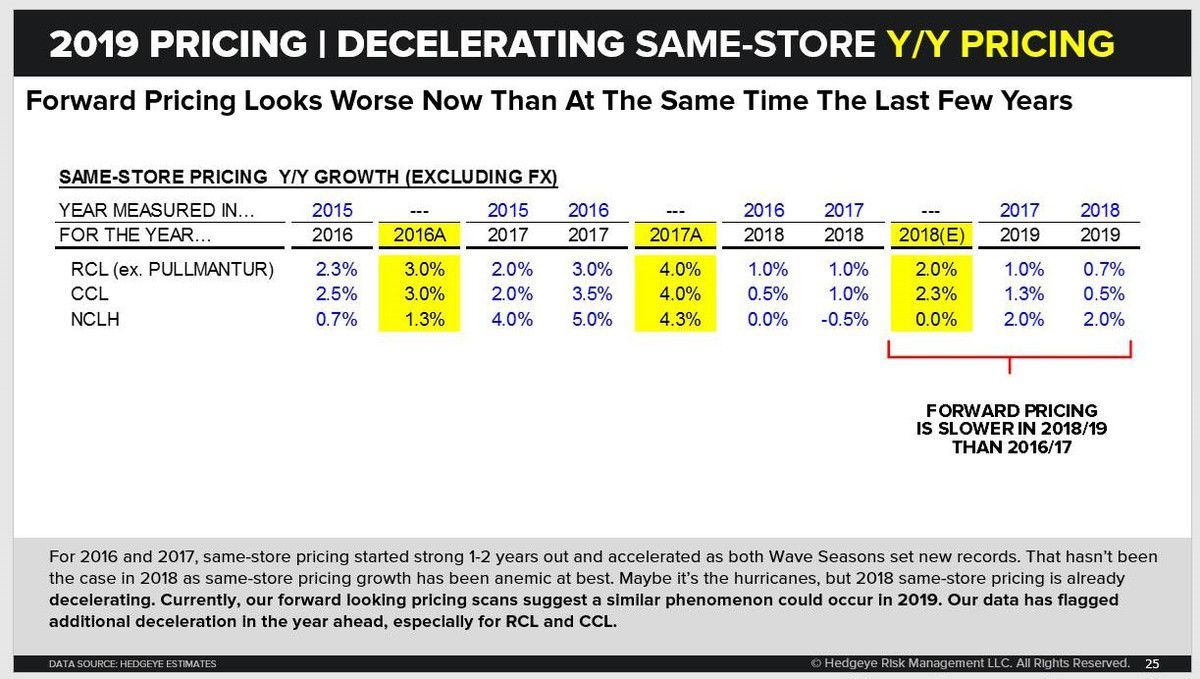

The growth engine for Carnival’s North America segment seems to have stalled recently. As we have talked about in our recent cruise presentations, the outlook from our 28,000 itinerary proprietary database for CCL Caribbean 2H 2018 suggests a softer pricing environment than 1H 2018.

There’s a list of reasons why:

- A more crowded Caribbean market

- Tougher comps; and

- A more aggressive promotional environment.

- In addition, consumers may be more hesitant than usual to book for the Caribbean this Fall given what happened with the hurricanes last year.

RECAPPING THE QUARTER

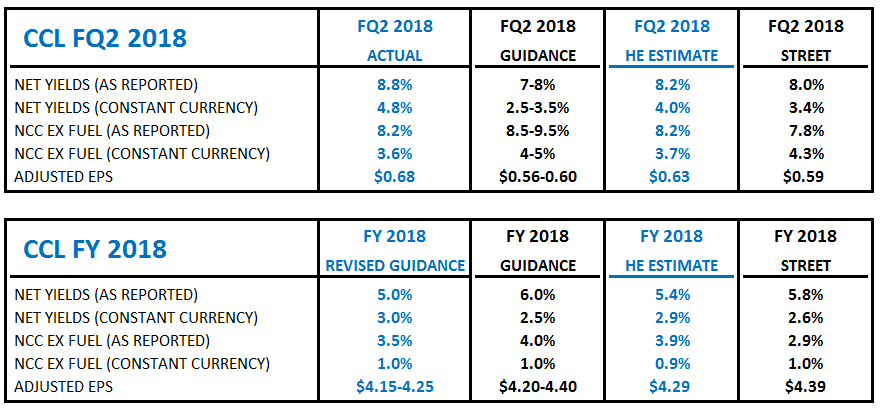

CCL's outlook is apparently a big surprise to the Street, particularly on the EPS reduction and less robust pricing color. Q2 yields beat by a big margin and while Q3 yield guidance (1.5%-2.5%) is weaker than the Street’s expectations (2.9%) and in-line with ours (2.1%), CCL’s history of beats and bookings/pricing color suggest Q3 yields are currently trending a little above 2.5%.

The full-year yield growth hike to 3% had been well anticipated and could be the last one this year. But the pricing language in the release (“in-line” vs “higher prices” in the Q1 release) concerning the next 3 quarters suggest pricing growth deceleration for 2019. This does not bode well for yield growth in 2019.

Another surprise to the Street is on FY EPS guidance of $4.15-4.25. Factset estimates for 2018 EPS was $4.36 despite the recent headwinds from FX/fuel. The Street historically have not modeled the impacts from FX/fuel well.

All-in-all, this report missed expectations on many levels.

As for Alaska, CCL’s same-store pricing has been weak, owing to new competition from Norwegian Joy. Management highlighted a “mix” issue regarding the cruise vacation packages (primarily from Holland America and Princess brands) which is really just competitive pressure from Norwegian Joy. Joy is taking share from the limited hotel inventory reserved for land vacation packages which is causing capacity issues and leading to pricing declines.

Meanwhile, margins at CCL’s NAA segment (North America & Australia) are declining. NAA margins fell 140bps YoY in Q2 2018 due to higher dry dock costs ($30m), higher commissions/transportation/other costs ($20m) and higher port fees ($11m).

Underperformance for CCL’s North America segment does not bode well for momentum heading into 2019. CCL’s 2018 yield growth will likely end up a few bps above ~3% but this is still substantially slower than the 4.5% growth seen in 2017. We continue to predict an even slower yield growth environment for 2019.

Even after CCL’s worst 1-day stock decline in 2 years, the stock is still within its 11-14x yield deceleration valuation range. The company’s willingness to aggressively buy stock in the coming months should provide a good signal as to whether the “bullish” commentary about the state of their business is real. Stay tuned.

ONE-YEAR TRAILING CHART