While volume was up 14% day-over-day, the absolute level remains very low as the stocks sold off on Tuesday. Globally the MACRO environment continues to be challenging as the RECOVERY theme is losing traction. The dollar was stronger yesterday after Germany's business climate index unexpectedly fell in February for the first time in 11 months and confidence and spending data out of Italy and France also suggest that a regional recovery is uncertain.

Domestically, the market weakness was made worse as February consumer confidence plunged 10.5 points to 46. Following a disappointing University of Michigan confidence reading on February 12th, the Conference Board’s confidence index declined from a revised 56.5 in January to 46.0 in February, the lowest reading in 10 months. According to the median of 68 estimates in a Bloomberg survey, Economists forecasted that the confidence index would decline to 55.0 from a previously reported 55.9 January number. Expectations fell to a seven-month low, while the current conditions index hit its lowest level since early 1983.

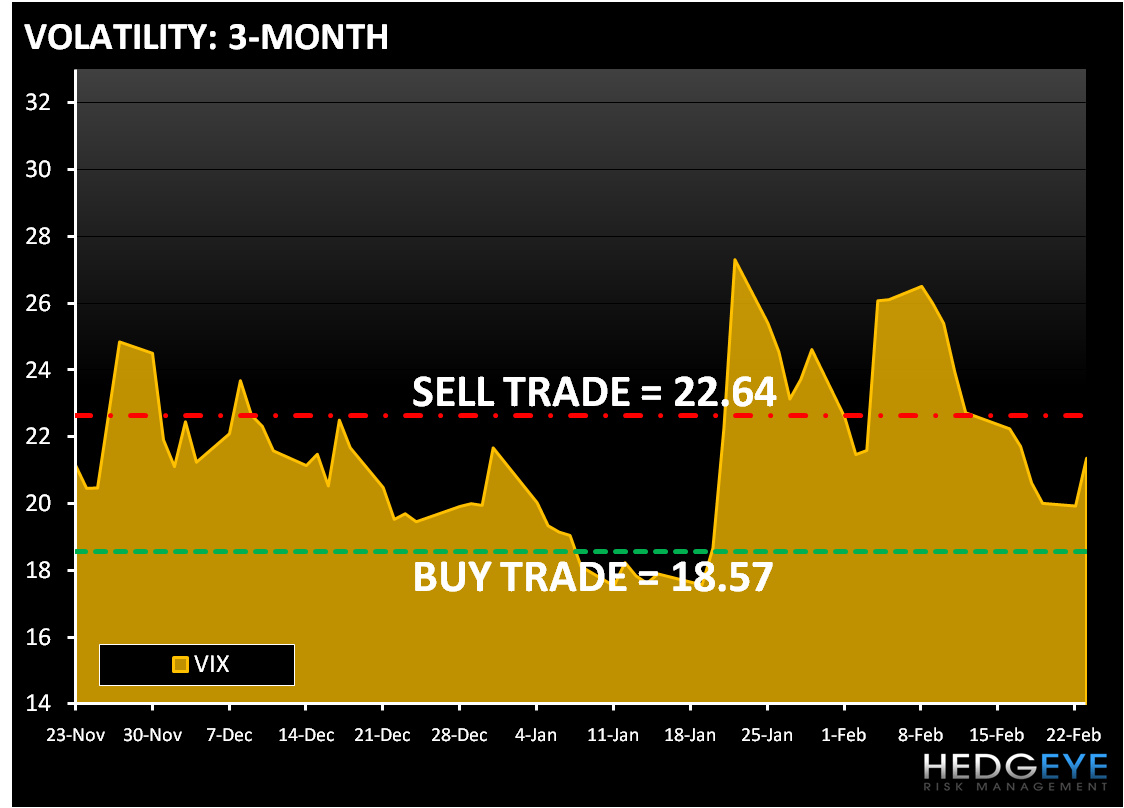

Ironically, with consumer sentiment the primary impetus for yesterday’s 1.2% decline in the S&P 500, Consumer Staples and Discretionary were the two best performing sectors in the market yesterday. With Utilities rounding out the top three, the SAFETY trade was in full force yesterday. Not surprisingly, the VIX rallied 7% yesterday. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (18.57) and Sell Trade (22.64).

Within Consumer Discretionary (XLY), Retail held up better than the S&P 500. The outperformance was on the back of HD and M, which reported better than expected trends for 4Q09. On the downside, TGT finished off its lows, but was still weaker on the day following its Q4 results and less than robust outlook.

After being the best performing sector on Monday, the Financials (XLF) was the worst performing on Tuesday. The decline in the XLF is centered on the decline in the banking stock with the BKX down 2.3%; large-cap regional’s were among the worst performers in the group.

Along with the XLF breaking TRADE and TREND yesterday, Technology (XLK) broke TRADE yesterday. Yesterday’s decline in technology was centered in the Semiconductors with the SOX down 2.8% on the day.

Equity futures are trading modestly below fair value following Tuesday's nearly 1.2% decline sparked by disappointing consumer confidence data, and ahead of Fed chairman Bernanke's testimony to Congress at 10am ET. Ahead of his testimony the Dollar index is slightly lower in early trading. The Hedgeye Risk Management models have levels for DXY at – buy Trade (79.60) and sell Trade (81.05).

As we look at today’s set up the range for the S&P 500 is 31 points or 1.7% (1,090) downside and 1.1% (1,121) upside.

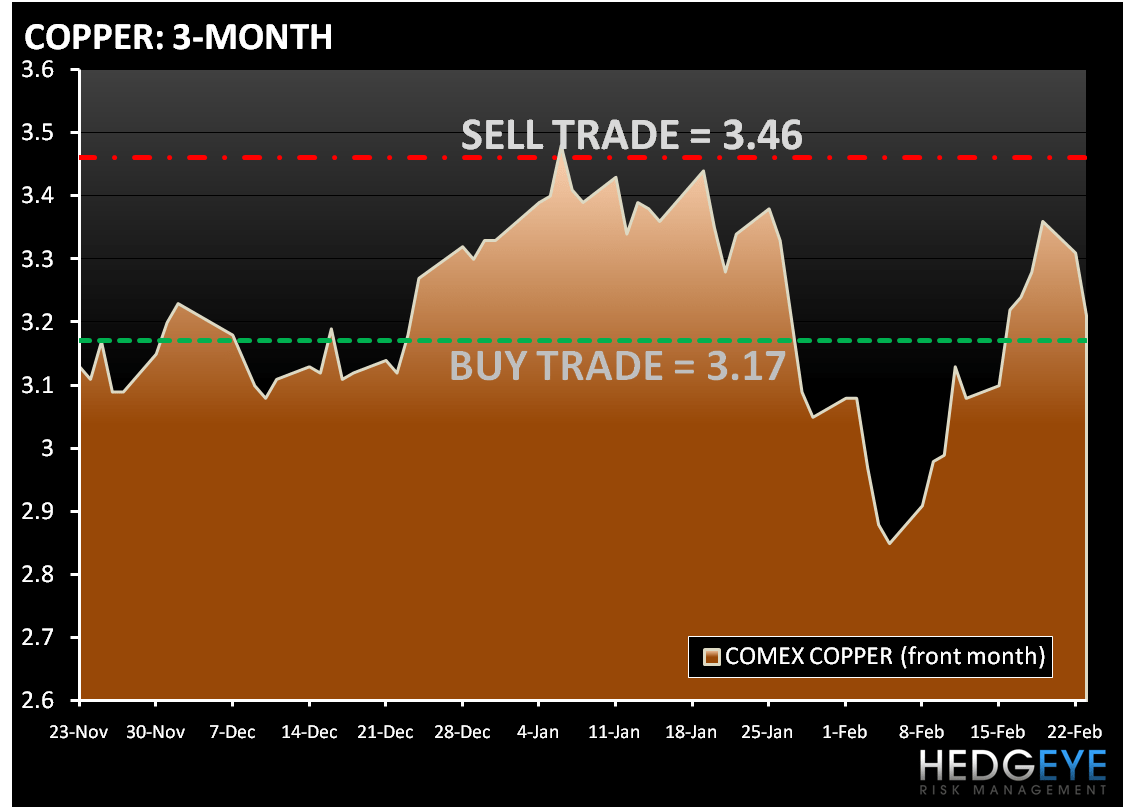

Copper is declining for a third day in London after imports of the metal into China, the world’s biggest consumer, dropped for the first time in three months. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.17) and Sell Trade (3.46).

In early trading gold is trading down for the third straight day. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,075) and Sell Trade (1,117).

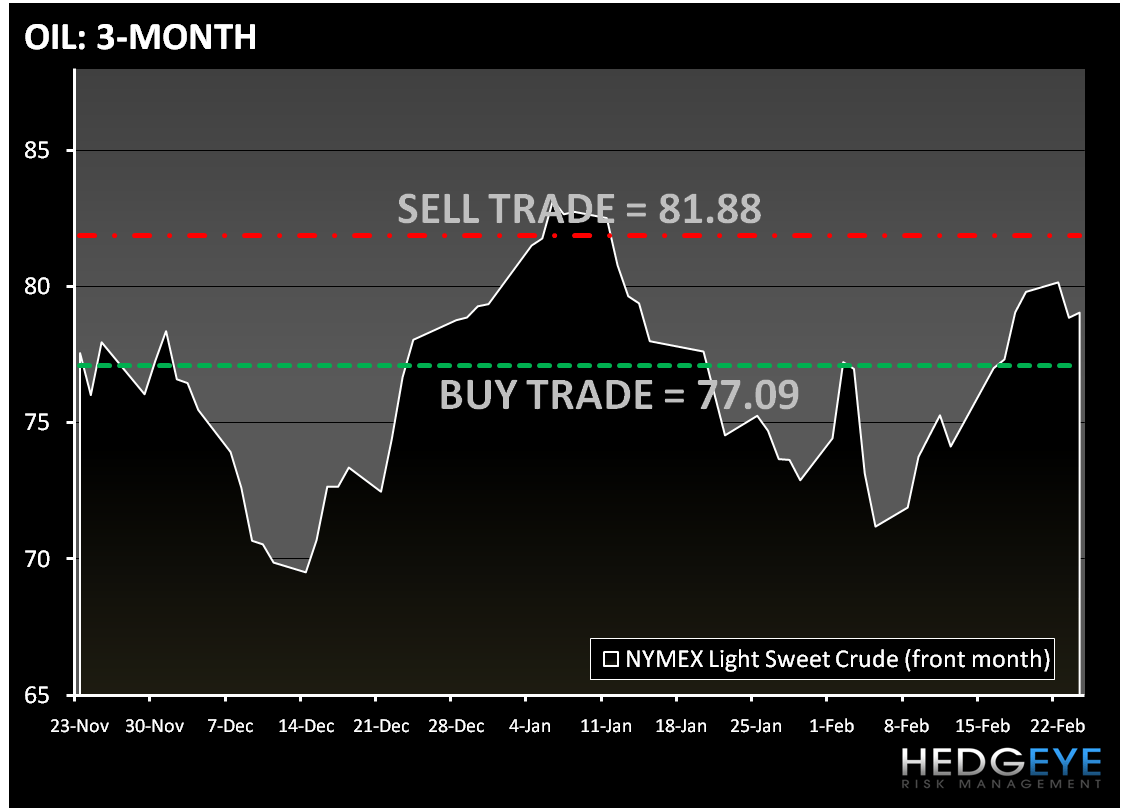

Oil is trading down for the second day in a row. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (77.09) and Sell Trade (81.88).

Howard Penney

Managing Director