There is a disconnect between how the government is reporting the economy’s performance and how the consumer feels the economy is doing.

As the Obama administration tells the story through its heavily padded economic data points, the US economy is improving and borderline hot. The latest unemployment reading fell 30 bps to 9.7%, GDP is white hot at 5.7% and retail sales in January rose a better than expected 0.5% versus a -0.3% decline in December .

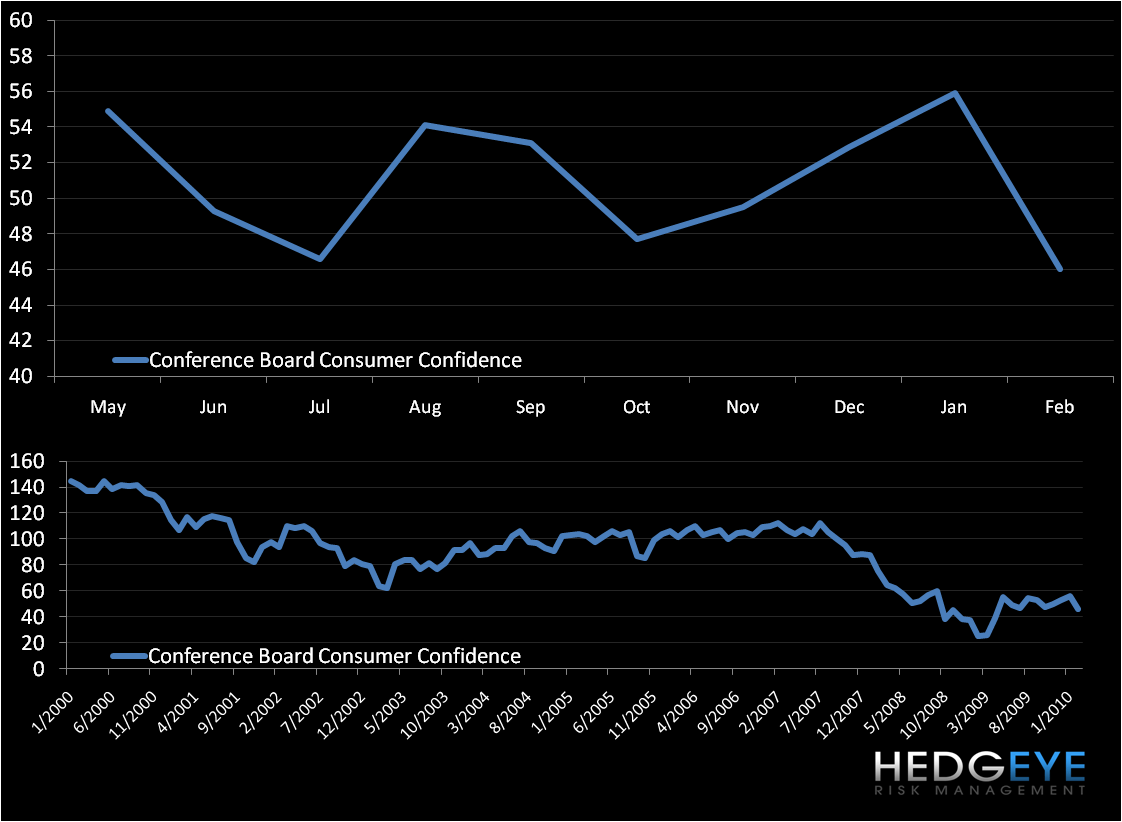

Today, the Conference Board is telling us that consumer confidence is at a 10 month low. What gives? The average consumer is just not seeing what the government is reporting.

Following a disappointing University of Michigan confidence reading on February 12th, the Conference Board’s confidence index declined from a revised 56.5 in January to 46.0 in February, the lowest reading in 10 months. According to the median of 68 estimates in a Bloomberg survey, Economists forecasted that the confidence index would decline to 55.0 from a previously reported 55.9 January number.

Could this month’s confidence number be an aberration or have consumers been too optimistic about how fast the recovery would actually impact their lives? While a monthly aberration is always a possibility and the winter doldrums are surely a negative, this month’s decline in confidence was broad based. There were declines in all of the elements of the present situation and expectations subcomponents, in all income classes, and in two of the three age groups.

On the margin, some segments of the retail landscape (including Restaurants) have been showing sequential improvement in January. While we are still cycling against very easy comparisons from last year, the decline in confidence does not help to maintain the positive momentum.

Another related, but not as relevant (it’s a December data point) consumer stat reported today is that home prices in the Case-Shiller Composite-20 City Home Price Index rose in December for a seventh consecutive month. The index increased 0.3% from the prior month on a seasonally adjusted basis, more than anticipated and matching last month’s improvement. On a year-over-year basis, the index was down 3.1% from December 2008, the smallest YOY decline since May 2007. We will have more to say on this in the coming months, but for now, the Case-Shiller data is not statistically significant.

We remain bearish about the prospects of a consumer led rebound anytime soon…

Howard Penney

Managing Director