Editor's Note: Below is are a series of excerpts transcribed from recent editions of The Macro Show laying out our views on #ChinaSlowing.

The transcription below follows a discussion between Senior Macro analyst Darius Dale and CEO Keith McCullough along with our responses to Hedgeye subscriber questions during the live Q&A portion of The Macro Show. (Click here to learn more about The Macro Show.)

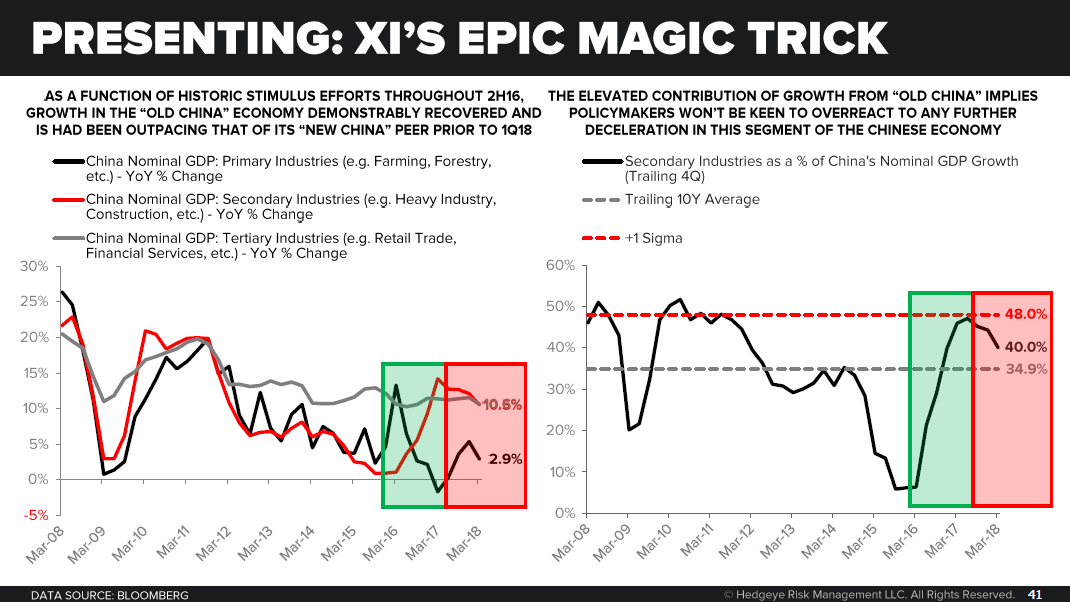

Darius Dale: Here's the backstory. China's economy accelerated materially during what had been a massive 2016 stimulus program. The rest of the world got dragged up on a lag.

China was definitely a causal factor in the synchronized global recovery. Now most Chinese economy charts you look at are moving in the wrong direction. So the key takeaway is if you believe China was a causal factor of the synchronized global recovery, now that China is moving in the wrong direction, you should continue to expect global growth divergences, particularly in countries that were impacted by China on the way up. Think Europe and Emerging Asia.

Keith McCullough: So the Chinese stimulate and at the peak this number (China Nominal GDP: Secondary Industries) was 14.2%. So we've gone from up 14% to 10.5% and falling (see chart below labelled "Xi's Epic Magic Trick"). So they stimulate the living daylights out of the Chinese economy, grip it and rip it. China peaks last year, copper peaks, aluminum peaks, and everybody gets bullish on Emerging Market growth, particularly the countries that were linked to China.

Remember, that move in Secondary Industries was almost 50% of incremental GDP in China (see chart below labelled "Xi's Epic Magic Trick"). Now, they have to compare against that.

This should be among the top three things you’re watching in the global economy right now. But you'll never hear about this in the Old Wall media. This is the problem. People are missing the biggest stuff and being distracted like Macro Tourists by the little stuff. When you start talking trade tariffs that are like $50 billion to $100 billion. $100 billion? You know how much stimulus the Chinese injected in 2016?

Dale: It was trillions of dollars. Trillions.

China is the world's second largest economy. Could you imagine if any segment of the U.S. economy went from contributing below 10% to GDP to almost 50% (see right hand scale of the chart below)? We'd be talking about that for the next 10 years but I guess people aren't sequencing markets.

Markets are forward looking so equity markets are looking ahead to increasingly steepening base effects. The two year growth rate in the comparative base period steepens for China all the way through Q1 of 2019.

So the probability that these numbers continue to slow is high. And markets are increasingly pricing in degradation in the global growth matrix.

Subscriber: Good morning. China cut interest rates recently. Does that impact #ChinaSlowing? I know if they weren’t slowing they would not have cut. Does China have the resources to change course? Thanks.

McCullough: Really good question. The People’s Bank of China cut its reserve requirement ratio by 100 basis points.

So yes it’s a move that confirms the Chinese are getting nervous about what we’ve been telling you which is the Chinese economy is slowing. Meanwhile, this cut came in conjunction with the stock market just hit year-to-date lows.

But no, I don’t think that’s the end of the #ChinaSlowing story. I think it just confirms that they’re lying to you when they say China is not slowing.

Subscriber: Do you have the same view of Chinese technology companies that you do of Chinese industrials?

McCullough: No. Let’s look at this chart (see the chart above labelled "Xi's Epic Magic Trick"). What I’d isolate here is the left side. There are three different things component parts of Chinese growth to watch.

When I think about Chinese consumption, what we’re talking about is the grey line or tertiary industries. Look at that line. It's stable. It doesn’t really do anything. I actually like the consumption story in China because you’re just building on very low per capita GDP consumption levels. I buy into that.

Now, the cyclical component or secondary industries is what we’re really concerned about. This is the one that goes all over the place.

There have been plenty of great Chinese stocks on the consumption side, but my general problem with those is that I’m so bearish on China overall that I think thematically China is for sale in people’s portfolios. That’s the factor level analysis.

So when you see anything in China it’s started to underperform because the economy had a horrible start to the year from a broader stock market perspective but I would separate China consumption from the cyclical component which has wicked difficult comparisons.