"Hope is not the conviction that something will turn out well but the certainty that something makes sense, regardless of how it turns out”

-Vaclav Havel

HOPE is not an investment process, but I HOPE the EU and Ben Bernanke get it right. As Keith McCullough posted yesterday he thought the prepared statement was “refreshingly objective” in saying the Federal Reserve will raise the discount rate “before long.” This is an explicit change in the Fed’s language; a change we thought should have come in January.

The two dominant MACRO factors at work yesterday were the fiscal challenges in Europe and Ben Bernanke testimony that wasn’t. On the lack of conviction on how this is going to end, the S&P 500 finished lower by 0.22% on very light volume. Although, the light volume is likely more a function of the East Coast snowstorm.

In our multi-factor model, the VIX was the only factor that suggested a continued benefit from the RISK AVERSION trade. The VIX closed down 2.3% to 25.40, but is still bullish on TRADE and TREND. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (22.40) and Sell Trade (28.34).

The favorable risk implications are emanating from increased expectations for some kind of Euro/German rescue package for Greece and other troubled European nations. Greek Prime Minister George Papandreou is on the tape saying he does not need help, but has apparently hammered out an aid package. The Dollar index (DXY) gained some strength yesterday finishing up 0.21%. The Hedgeye Risk Management models have levels for DXY at – buy Trade (79.69) and sell Trade (80.67).

Yesterday, the Consumer Discretionary (XLY) underperformed the S&P 500 and broke TREND, leaving Healthcare as the only sector positive on TREND. Although it should be noted that the XLV was the second worst performing sector yesterday, declining 0.6%

The only sector up on the day was Financials (XLF). The money center banks bounced yesterday from the benefited of the RISK AVERSION trade; the two standouts were BAC and JPM. Outside of the banks, the asset managers outperformed too.

The strength in the DXY and earnings miss put pressure on the Materials (XLB), the worst performing sector yesterday. The XLB declined 0.7% yesterday, with the weakness focused on the steel sector. ArcelorMittal announced below consensus Q1 EBITDA guidance, as higher shipments will be offset by lower ASPs and increased costs. Ah yes inflation!

As we look at today’s set up, the range for the S&P 500 is 31 points or 2.1% (1,045) downside and 0.74% (1,076) upside. Equity futures are currently trading above fair value in a follow through to yesterday's late day bounce and the EU support of Greece.

Copper climbed the most in almost three months in London as lending increased in China and employers added jobs in Australia, improving the demand outlook. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (2.82) and Sell Trade (3.14).

The correlation for gold continues - gold is trading lower on the back of a stronger dollar. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,044) and Sell Trade (1,111).

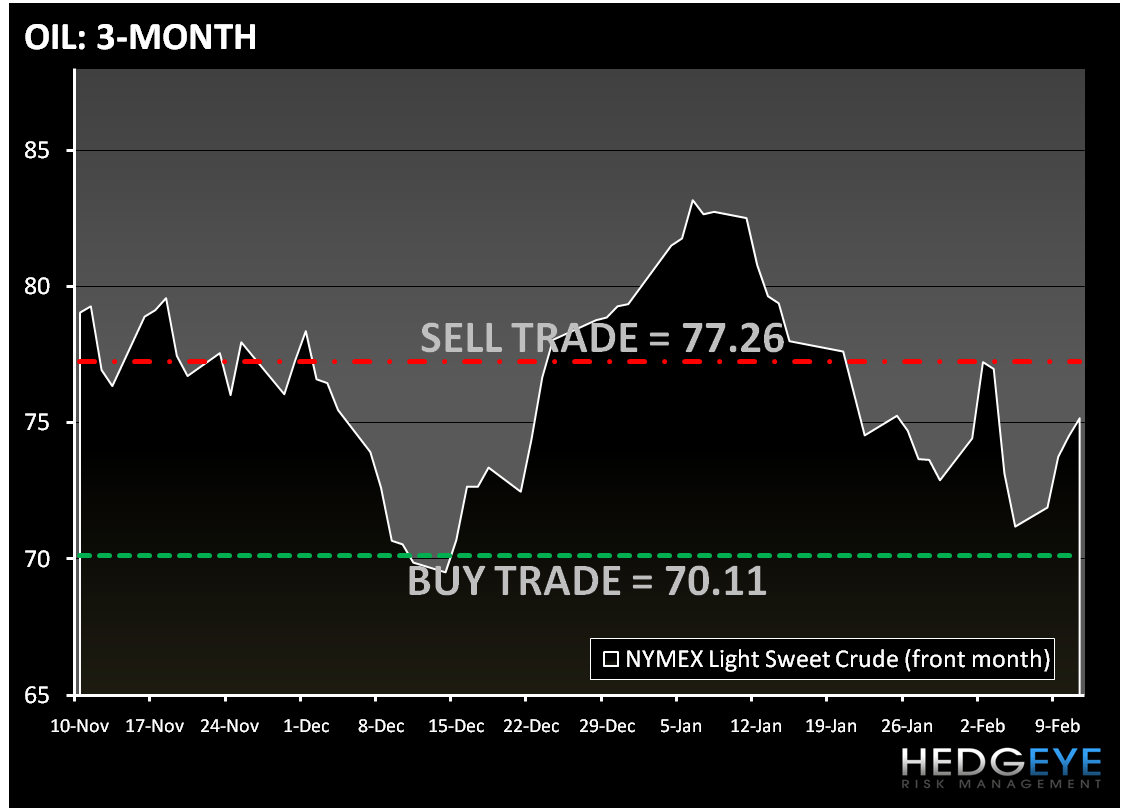

The International Energy Agency raised its forecast for global oil demand this year as developing countries need more crude to fuel their economies. Oil has traded higher for the last three day and looks to be up again today. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (70.11) and Sell Trade (77.26).

Howard Penney

Managing Director