MARKET WATCH

Are corporate earnings losing their market-moving potential? That’s the question posed by researchers Feng Gu and Baruch Lev in a new report published in Financial Analysts Journal (FAJ), which finds that even perfect prediction of earnings no longer generates a hefty above-market return. This conclusion has obvious implications for equity asset managers. Even more impactful is the companion discovery that the earnings-return relationship may be weakening because of an economy-wide shift toward intangible assets. Optimists interpret this shift as evidence that years of heavy investment in hi-tech innovation will inevitably pay off in a higher economic growth rate. Pessimists say a great deal of spending on intangibles is wasted on jealously guarding intellectual property (IP) rather than creating it.

Earnings reports aren’t what they used to be. In the FAJ report, researchers Gu and Lev examine historical corporate earnings beats and misses alongside stock market returns going back to the late 1980s. They consider a hypothetical “perfect” investor who, at the beginning of a given quarter, held a long position in every company that would subsequently beat its quarterly earnings estimate and held a short position in every company that would subsequently miss its quarterly earnings estimate. The conclusion: In that given quarter, such an investor would have generated a rather sizable 6 percent premium over the rest of the market in 1989-91. But the same investor would have generated just 2 percent more than the market in 2013-15.

The researchers also accounted for earnings growth and decline rather than beats and misses by constructing a second hypothetical scenario. In that scenario, a perfect investor would have generated a 4 percent premium over the rest of the market in 1989-91. But the same investor would have generated just 2 percent more than the market in 2013-15.

This trend clearly impacts equity asset management as a profession. After all, if even perfect prediction of earnings leaders and laggards no longer generates much of a premium, a fallible human manager who can only occasionally see the future correctly may more often drift down to (or below) the benchmark—making it harder to justify the premium that investors are paying for his or her services.

What could possibly explain it? One possibility is that quarterly earnings reports no longer indicate company performance. Indeed, as observed by The Wall Street Journal, an earnings beat increasingly reflects a proactive IR department rather than an outperforming firm. Maybe investors have simply learned to tune out corporate optimism. Another explanation is the rising prevalence of subjective accounting methods like “fair value” accounting, “big bath” bookkeeping, and the establishment of “cookie-jar” reserves. Figures from Audit Analytics confirm that companies are indeed getting more creative with accounting practices that end up boosting their reported income.

Yet there may be a better explanation of the weakening earnings-return relationship—and that’s the fundamental shift toward an intangible economy.

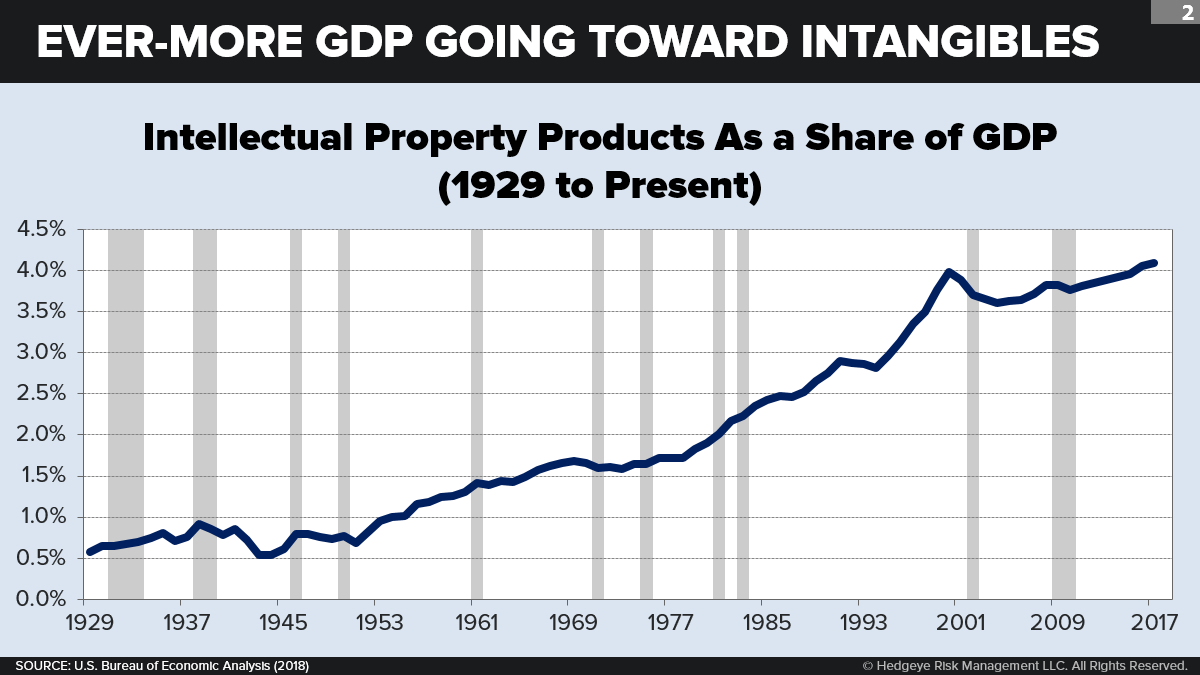

Until very recently, most of the market’s top firms were rich in “tangible assets” such as factories, machinery, land, and inventory. As recently as 2001, the most capitalized U.S. firms included industrial giants like General Electric and oil barons like Exxon flush with fixed capital. But over the past three decades, the rise of super-scalable tech—especially in new industries like e-commerce, the sharing economy, and digital media—has produced a new crop of “asset-lite” market leaders. An early example was Microsoft, whose actual plant and equipment in 2006 constituted just 1 percent of its market cap. Today, Microsoft has been joined by the so-called “FAANGs”: Facebook, Amazon, Apple, Netflix, and Google. Instead of factories, these companies deal largely in intangible, conceptual assets like patents, copyrights, data, “brands,” and other types of IP.

How, exactly, does this shift toward intangible assets affect corporate earnings? Quite simply, modern accounting understates earnings for companies that produce a lot of intangible assets. A tangible asset is capitalized; only its depreciation, rather than the cost of the entire asset, is counted as an expense on the income statement. By contrast, under GAAP, all IP production is expensed immediately—which lowers earnings in any given quarter in which a company spends heavily on intangible assets.

What are the attributes of companies that invest heavily in IP? To the extent that such firms are growing in their relative size and importance, how does that growth affect the behavior of the U.S. economy? For an in-depth discussion, see the recent book by Jonathan Haskel and Stian Westlake, Capitalism Without Capital: The Rise of the Intangible Economy (2018). Some of the overall features of this growth include:

- more sunk costs;

- more scalability and synergy;

- more market concentration; and

- more struggle to protect IP ownership and acquire spillovers.

There is broad agreement that the rise of the intangible economy is probably implicated in a wide number of structural shifts in business behavior. But when we get to next question—whether the net impact of intangibles is good or bad for the U.S. economy—opinions are divided rather starkly.

An optimistic viewpoint holds that this recent IP boom represents an extraordinary wave of technological innovation that will ultimately generate dramatic gains in living standards. Like earlier waves that gave us the steam economy or the railroad economy or the electrical economy, this new wave rivals or exceeds its predecessors. Of course, as we’ve mentioned before (see: “The Great Productivity Slowdown: Fact or Fiction?”), the dramatic slowdown in labor productivity growth since the Great Recession undercuts this hypothesis.

Problems with the optimistic account have bred a newer, contrarian viewpoint. According to pessimists, much of what we measure as a rise in intangible “investment” is attributable to rising monopoly rents claimed on the already-owned innovation that firms are exploiting. What’s truly unique about IP is not so much how it enables owners to use knowledge, but rather how it enables owners to exclude others from using knowledge. And, by any measure, the U.S. legal system recently has gotten much better at rewarding efforts by firms to expand and defend what constitutes ownable knowledge. In the past, inventions from penicillin to the World Wide Web to the transistor were allowed to pass fairly easily into the public domain. But today, corporations and individuals rush to patent anything of even middling value—from crustless sandwiches (Smucker’s) to rounded corners (Apple).

So which side is right? Looking only at the data won’t give you the answer. Though we are getting better at measuring intangible investment, the available data are agnostic. Growing intangible investment could be taken as evidence that businesses are creating huge new technological gains (the optimistic viewpoint)—or as evidence that businesses are simply better able to exert their monopoly power (the pessimistic viewpoint). Right now, the evidence favors the pessimists. But in any case, as U.S. firms continue to ramp up their intangible investments, the debate will continue to gain fuel.

TAKEAWAYS

- Realize that the shift toward intangible investments impacts everything from finance to the broader economy. New research finds a weakening correlation between corporate earnings and stock market returns, a trend which poses serious challenges to equity asset managers. The most likely explanation deals with the rise of intangible investments that are not capitalized on the balance sheet. The economy-wide shift toward intangible investments is a phenomenon in its own right, one that has stirred up a lively debate. Optimists interpret this shift as evidence that higher economic growth is inevitable. Pessimists say that much of this spending is wasted on protecting a firm’s existing intangible assets rather than generating new ideas.

- Take the optimists’ argument with a grain of salt. Optimists believe the ongoing IP boom will soon produce both a high ROR on capital and a high rate of overall economic growth. But there’s no evidence thus far to support this viewpoint. To the contrary, labor productivity growth has actually decelerated since the GFC. What about informal measures of standard-of-living growth? Think again: A plurality (41 percent) of U.S. citizens say life in their country is worse than it was 50 years ago for people like them. Meanwhile, more than half of Americans (56 percent) believe the next generation will be economically worse off than they are.

- Understand how to invest in the intangible economy. Optimists will want to track the emergence of game-changing innovations, those most likely to generate a higher ROR, wider profit margins, and more rapid revenue growth for entire industries. Pessimists will want to track those firms which produce or acquire the most "ownable" IP and which can best use that IP to create islands of privileged incumbency. (Think of Warren Buffett’s “business moats.”) Optimists will be more interested in the underlying technology. Pessimists will be more interested in the fine print and loopholes of each deal—and in any changes in public policy that could reshuffle the playing board overnight.

- Keep in mind that R&D spending has changed significantly in recent decades. Back when the G.I. Generation ran America, most U.S. R&D (67 percent in 1964) was funded by the federal government. But the decades-long rise in business spending on R&D has been matched by the decline in federal spending—to a mere 22 percent of all R&D by 2015. What’s distinctive about federal research? For starters, the public sector rarely patents its high-tech breakthroughs on behalf of taxpayers. Typically, it just lets the knowledge quickly and freely flow through to industry, which accelerates economic growth. Moreover, a much larger share of federal research is “basic,” that is, oriented toward fundamental technological discoveries.