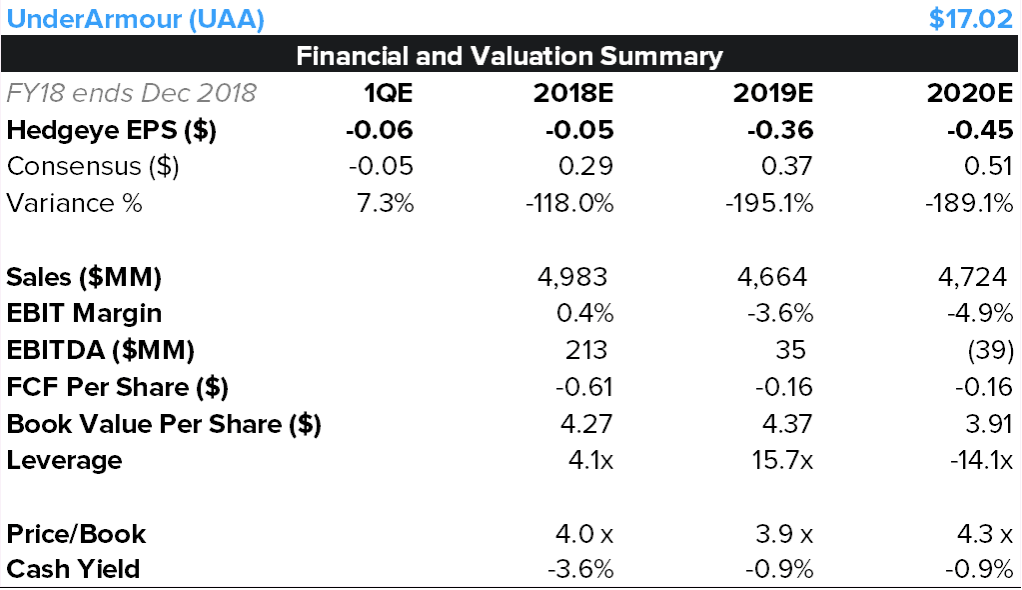

The likelihood of Under Armour having one of those gut-wrenching ‘I can’t believe revenue is actually down -10% after such a confident guide’ moments is about as high as any company in retail today. Our conviction short side is clearly higher given what’s likely to be unhittable numbers. Unlike names like FL, RL, TIF, LB, etc… this one is likely to be violent as opposed to a series of guide downs. Yes, the company just gave confident guidance, but remember when Plank fired his CFO a month after issuing guidance at the company’s Sept '15 analyst meeting? The guide comes from the top, with targets pushed down to the rank and file – and very little respect for the process (if there is one) that develops the internal financial plan.

I’m taking down our model to a flat year in ’18, and a 6% sales decline in 2019 with an equity deal of $400mm, $200mm in debt issuance, negative EBITDA, leverage going north of 10x before the equity deal, and negative earnings for the next three years. Remember when LULU and LIZ both hit $3? That was a different environment – but given the lack of talent inside the company (ie severe step-up in firings/retirements) at a time when UAA needs more internal resources than ever to right the ship. I don’t see how – for the life of me – UAA can grow without major structural change. Planks needs to fire himself, and hire a real CEO. He built something great…one of the best ideas in a generation. But at least Chip Wilson had the sense to know when his time was up.

We’re hosting a black book on March 20th at 12:30PM EDT (details to come) to review our full short thesis, including why an activist role might actually work (despite class C shares) after the EV is halved -- again.