Below are analyst updates on our seventeen current high-conviction long and short ideas. Please note we removed AMN Healthcare Services (AMN) from the short side of Investing Ideas this week. Below are Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

Levels

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TWX

Click here to read our original analysis on why we think the AT&T/Time Warner (TWX) deal will be approved.

Telecom & Media analyst Paul Glenchur has been in the courts and all over this AT&T/Time Warner merger case with the court denying AT&T’s (T) request for White House documents in Time Warner (TWX) deal litigation recently. Glenchur expected AT&T would likely struggle in its effort to present a credible claim that the Justice Department action to block the Time Warner acquisition constitutes selective prosecution. This is a defense that could have opened the door to documents and other evidence to prove inappropriate White house involvement in the TWX antitrust review.

Ultimately, we continue to believe that AT&T prevails in this merger. As Glenchur has noted, the underlying merits of the government's case to block the deal are highly questionable. The Antitrust Division will need to present compelling evidence that AT&T's ownership of Time Warner content will lead to increased costs to distribution rivals that will be passed along in consumer subscription bills. The level of asserted price hikes, according to indications from the recent hearing, are not alarming and could be neutralized by AT&T at trial. The case remains on track for the March 19th trial start date.

More could be at stake than AT&T's Time Warner acquisition. Comcast reportedly offered to buy Fox (FOXA) entertainment assets at a price that was roughly 15 percent above what Disney has offered for the same assets. If, as we believe, Fox rejected the Comcast bid largely due to antitrust concerns arising from the DOJ challenge to the AT&T/Time Warner transaction, a DOJ retreat or defeat in the current trial could resurrect Comcast-Fox discussions.

Indeed, if AT&T ultimately prevails, a range of deals for content assets could be pursued as various players seek scale or other strategic benefits in a disrupted media environment.

RRR

Click here to read our analyst's original report.

Gaming, Lodging & Leisure Sector Head Todd Jordan anchored The Macro Show earlier this week and gave a very timely update to his Red Rock Resorts (RRR) long thesis. RRR reported earnings this week and, as Todd says, the company "offers the most long term appreciation potential in domestic gaming."

CLICK HERE to watch this edition of The Macro Show.

CLICK HERE to access Todd's RRR slide deck (which starts on page 11).

HST

Click here to read our analyst's original report.

The latest weekly STR data indicates that Hotel RevPAR slowed vs. the prior week and was weaker than the prevailing 3-4 month trend. This choppiness jives with management guidance and commentary that has leaned bullish, but also cautious given the recent volatility in RevPAR growth. For the week ended 2/24/18, total US RevPAR grew 2.0% YoY.

MTD trends have been choppy, with some weeks indicating broad strength and others showing weakness. That said, the broader trend still look positive to us on the 2nd derivative, and we expect a solid finish to the month of February. We estimate February RevPAR to grow at least 3%.

The recent sell off has created buying opportunities in some of our favorite hotel REIT stocks, like Host Hotels (HST). We believe that HST is likely to outperform in terms of EBITDA and RevPAR growth in the coming year. As it currently stands, our top down view is unchanged and we still see better RevPAR growth as the more probable outcome.

MLCO

Click here to read our analyst's original report.

Q4 was a strong one in Macau and we were particularly impressed with the performance of the mass segment. Mass growth surged in Q4 and if March can sustain the combined growth of Jan/Feb, Q1 earnings should exceed expectations for most of the Macau operators. We’re bullish on Macau’s near and long term outlook and Melco Resorts (MLCO).

While February GGR fell a little short of consensus expectations, we would buy these stocks on any weakness. February faced a tough comp and an unfavorable Chinese calendar and volatility with this seasonally up and down period is difficult to forecast. We see a nice bounce back in March which should round out a strong quarter of revenues and earnings. A closer look at the visitation statistics suggest surging 1st time visitation and faster growth from underpenetrated provinces. These are nice trends and suggest a long tail of growth for Macau, not necessarily reliant on the macro.

![]()

TWTR

Click here to read our analyst's original report.

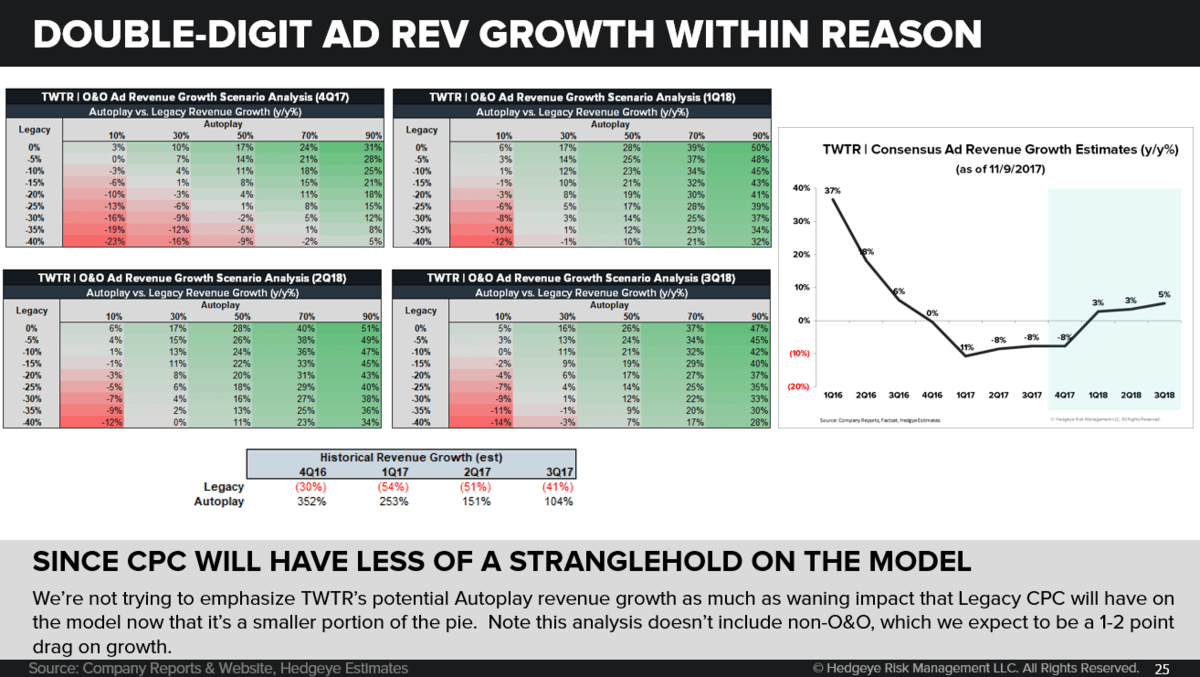

Owned & Operated Ad Revenues returned to positive growth, a 14 percentage-point acceleration (from -7% in 3Q17 to +7% in 4Q17). We estimate Twitter (TWTR) did so despite continuing declines in Legacy CPC ad revenue, which should be a waning drag moving through 2018.

We continue to think double-digit ad revenue growth is within reason. We're not trying to emphasize Twitter's potential Autoplay revenue growth as much as waning impact that Legacy CPC will have on the model now that it's a smaller portion of the pie.

KR

Click here to read our analyst's original report.

Below are three key reason why we continue to like Kroger (KR) on the long side:

1. Fundamentals are turning the corner

Starting with fundamentals (Sales, Gross Margin, EBIT, EPS), where we saw a marked improvement in 3Q17 on a one-year basis. Looking out to CY2018, KR has a favorable setup with easy comparisons due to their poor performance and extreme deflation over the past 18 months. We are looking for sales to improve on the heels of investments into the business which will enable long-term operating profit and EPS growth as they gain greater leverage in their model.

2. Taking the multi-employer pension plan issue head on

KR announced that they have withdrawn from the Central States Pension Fund, that was effective on December 10, 2017. The company recorded a one-time non-cash charge of approximately $410M in the fourth quarter, to remove 1,800 active associates from the plan. Although they have more work to do on the pension front, this is a big step in the right direction and the current market environment will put any underfunded pension risk on the back-burner.

3. Hedgeye GIP (Growth, Inflation and Policy) model points to more favorable environment for consumer staples in the back-half of 2018

We collaborated with our Macro team to leverage Hedgeye’s proprietary GIP model. Our Macro Team is modeling the US economy moving from Quad2 (growth accelerating as inflation accelerates and a hawkish monetary policy bias), where it is now, into Quad3 (growth slowing as inflation accelerates and a constrained monetary policy bias) by 3Q18. If we are right about the company’s accelerating fundamentals into FY18, and the Hedgeye Macro team’s models suggest that the setup is more favorable to be LONG Consumer Staples.

ORLY

Click here to read our analyst's original report.

AutoZone reported same store sales (SSS) of 2.2% this week, the highest SSS increase of the auto parts retailers. It is important to note that due to a different fiscal year AutoZone has the month of January in its quarter instead of October. The more seasonal winter weather boosted sales for the auto parts retailers in categories like wipers and batteries. Management said, “… our business improved due to the more harsh weather conditions we experience in late December and January.” Management also expressed optimism that there is a longer benefit for the balance of the year for the under carriage of cars – brakes, shocks, etc. Weather benefits are not part of our thesis of improving sales trends in the sector, but the increasing percentage of vehicles entering the sweet spot for repairs will be a key industry benefit.

AutoZone also reported a 26 basis point improvement in gross margins. While the improvement was modest it was the largest expansion we have seen since Q1 of last year. It is also notable given the concerns the market has for price pressure in the Do-It-Yourself (DIY) segment. The market is concerned that online price transparency will be detrimental to sales and margins at the auto parts retailers, but that has not happened to date despite the growth of auto parts online. We reiterate our long call on O'Reilly (ORLY).

MD

Click here to read the Mednax (MD) stock report Healthcare analyst Tom Tobin sent Investing Ideas subscribers earlier this week.

CERN

Click here to read our analyst's original report.

President Trump released his FY 2019 budget last month. It has everything you would expect; border walls, increased defense spending and cuts to domestic programs in education and health and human services. What the POTUS FY 2019 does not have is any reference to fully funding the VA Electronic Health Records Modernization project that is designed to replace the aging VistA technology with Cerner's (CERN) Millennium EHR.

The narrative description of the VA budget request suggests most of the $675 million EHR contract will be for the purchase of CERN services.

Keeping in mind the FY 2019 POTUS budget request is largely a political document, the notable absence of language dedicated to a multi-year $10 billion high profile contract suggests the following possibilities:

- The White House, in a show of fiscal responsibility is trying to avoid a big ticket line item, $18 billion border walls notwithstanding

- The VA is not yet ready to discuss and defend the project to Congress, already skeptical of a major IT expenditure, given less than perfect roll-out of the CERN system at DoD facilities in the Pacific Northwest.

The solution to these quandries appears to be incrementalism. The VA will limit its plans to adopting the DoD system and upgrade the VistA system to make it function in a standard and secure manner across all VA facilities.

VIRT

Click here to read our analyst's original report.

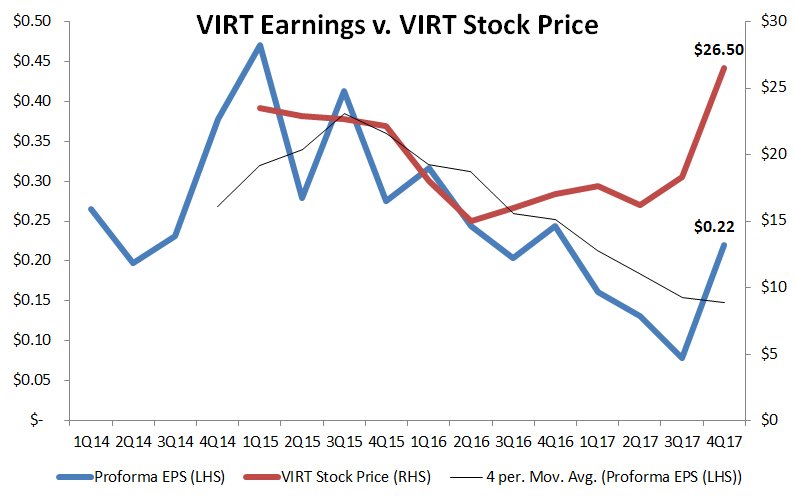

The trajectory of Virtu Financial's (VIRT) non GAAP earnings despite the 4Q17 earnings beat has not broken its down trend. The stock reaction is well ahead of its earnings opportunity set which sits at $1.20 to $1.40, still implying a substantial jump up (i.e. high expectations) from the $0.22 per share or $0.88 in annualized EPS:

HCA

Click here to read our analyst's original report.

Maternity continued to trend poorly in 4Q17 as it has for several years. HCA Healthcare (HCA) management commented that, consistent with our Maternity Tracker and recent results, births declined -2.5% while NICU volume was +0.6%. Despite the current strength of the 2017-2018 influenza season, flu was only a modest positive according to management. Guidance net of the Oklahoma divestiture and the loss of "$180M" in EBITDA looks particularly positive in relation to 2018 EBITDA guidance of $8.45B to $8.75B. While the volume and cost metrics continue to follow our models for volume by payer, the critical upside driver in the quarter was surprisingly strong acuity and the positive impact on pricing, particularly within the Managed Care payer segment.

We continue to find it highly unlikely that 4Q17 will continue through 2018. While it may be hard to remember, it was not such a long time ago when 2017 consensus EBITDA peaked at $8.8B, versus the final $8.2B reported. 2018 expectations were once $9.5B, versus the current midpoint of 2018 guidance of $8.6B. While 4Q17 held operational positives, HCA's future commitments appear excessive in comparison by committing to a $0.35 quarterly dividend and continued share repurchases, accelerating capital spending, and adding $300M in new employee training and retention costs. We believe the embedded risk for this high debt high fixed cost business has increased as a result.

DPZ

Click here to read our analyst's original report.

It appears that the issues seen in the Domino’s international business have finally reached Stateside! Last week we reiterated our Domino’s Pizza (DPZ) short when DMP-AU reported abysmal 1H18 figures, and we “continued to gain confidence in our position that Domino’s domestic business will meet the same fate.”

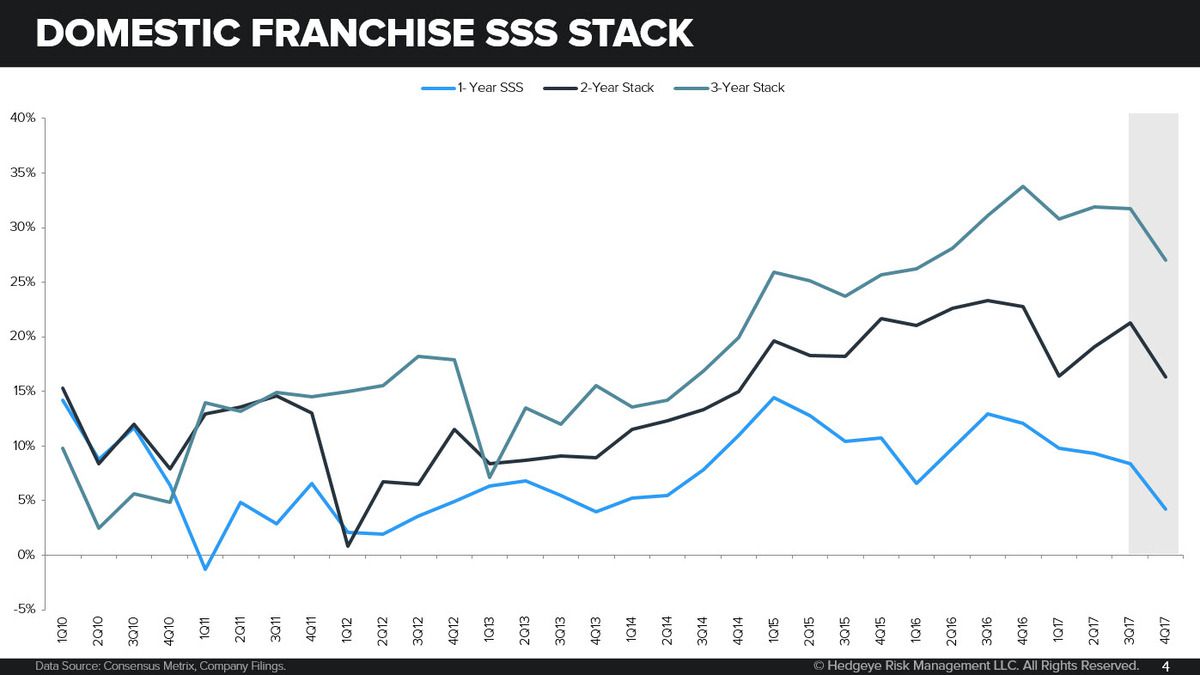

On a two year-average basis, DPZ’s international franchised, company-owned, and franchise domestic same-store sales showed sequential decelerations of 245bps, 235bps, and 250bps, respectively. The management team harped on the fact that they were facing a tough comp this quarter, but same-store sales has seen a stark deceleration even when you look at the 2-year and 3-year stack (see below).

TSLA

Click here to read our analyst's original report.

A Note from Industrials analyst Jay Van Sciver...

Criticism That We Are Undermining “A Good Cause” By Having Tesla (TSLA) As A Best Ideas Short:

Personally, I am someone who likes the environment and clean air. I think there are huge environmental problems beyond concerns around climate change, from giant garbage islands in the ocean to high rates of extinction. I support Tesla’s stated environmental goals, which is another reason why its losses and cash burn are so dangerous. If Tesla goes belly-up, it could create another Solyndra-esque example for those that oppose the government ‘picking winners and losers’, or some other narrative. If Tesla loses investor money, it may well increase capital costs (or curtail capital availability) for the next environmentally friendly, innovative commercial entrant in an established entity. Long-term, Tesla’s losses have an impact well beyond a quarter or a short position.

More generally, a value creating economic actor is supposed to deploy scarce labor and resources to generate something more ‘valuable’ than the inputs. One can argue what ‘value’ means, but for most companies it means a profit. If Tesla cannot generate a profit making somewhat more environmentally friendly vehicles, it should get out of the way and let someone else take the lead. It most likely means that, in aggregate, it is squandering scarce resources by turning a dollar’s worth of inputs into, say, 80 cents. No investor or government is going to cover Tesla-size losses per unit to replace a relevant potion of the world’s car fleet with more eco-friendly EVs. Creative destruction is on its way for Tesla, and that may be a great thing for the environment.

MC

Click here to read our analyst's original report.

Moelis (MC) stands at risk from a decline in M&A activity as volatility kicks up and equity values decline. Moelis reported slack in its earnings report this quarter with top line revenues of $169 million declining -17% over the 4Q16 period. This decline was flagged by our Boutique Activity Tracker (BAT) as MC specific activity has been trending behind expectations all quarter. From an earnings standpoint, MC reported $0.52 in EPS, which comped to the $0.66 per share from last year in 4Q16.

Volatility and equity price declines historically dry up strategic M&A activity so the current environment bears watching for an more intermediate term impact to the mid cap M&A advisors.

HBI

Click here to read our analyst's original report.

One of Hanesbrands' (HBI) key competitors had some major events in the last week and a half.

It reported earnings just over a week back, the big takeaway is Gildan branded men’s underwear continues to take share, with unit share up 160bps yy to 12%.

Then, this past week the company had an Analyst day in NYC. GIL reviewed details around a new re-organization, partially driven by the fact that it will chase sales in competitive businesses with price since the mass channel is shifting to private label.

Ultimate this means that Gildan is preparing itself for a shift happening in major distribution, HBI is not preparing for this.

The growth of online brand access means that branded products are increasingly available on Amazon and other sites at competitive prices, therefore the mass channel is focusing more on exclusive product or private label, to enhance the value to customers.

This shift is proven by the fact that HBI lost its Just My Size brand at Wal-Mart. When customers can get Just My Size on Amazon, Kohl’s, Target, and others, Walmart feels it’s better to stock its own brands in store so it can create better price/value offerings.

HBI will continue to lose share at the low end in the mass channel which makes up over 30% of sales, while competitive brand pressure means share loss in the rest of its distribution.

Organic growth will to continue to miss expectations.

UAL

The United Continental (UAL) Investor event recently was exceptional in that it completely reversed course on many key prior initiatives.

The most off target part of the presentation, in our view, is the focus on EPS and representations about the balance sheet. UAL burns cash – Free Cash Flow is negative. If one values UAL as an operating company, it should be worth the present value of future free cash flows to equity. If an airline burned cash over a 6 year period during decent economic activity, and burned cash in 2017, which was a very robust macro economy, a period over which its fleet aged and it “was shrinking”, what would that equity be worth?

SBUX

Click here to read the Starbucks (SBUX) stock report Restaurants analyst Howard Penney sent Investing Ideas subscribers earlier this week.