After a 5.7% correction in the S&P500 since January 19th the Hedgeye Risk Management models have zero sectors positive on TRADE and only three sectors positive on TREND - XLI, XLY and XLV. The S&P 500 came under pressure on Thursday, closing down 1.18%, though it did finish off their worst levels on the day.

Yesterday, the blame game put Greece, the tax proposals in President Obama's State of the Union address, earnings and initial jobless numbers as the reason for yesterday’s decline.

On the MACRO front, Initial claims fell to 470,000 in the week-ended January 23rd from 478,000 in the prior week, compared with consensus expectations for a decline to 450K. On a rolling 4-week basis, average initial claims rose 9k to 457k from 448k and are up 15k in the last two weeks. While the rolling number remains within the channel of improvement (see yesterday’s post for the chart), it is moving to the upper band of that channel quickly. Given the historical tendency for this seasonally adjusted data to trend up in mid-to-late January we will give it the benefit of the doubt for now that the longer-term trend lower remains in place, but we think the next month's worth of data will be very important. It’s definitely time to pay attention.

Durable goods orders rose 0.3% month-to-month vs. consensus expectations for a 2% increase. The miss was fueled by a 38.2% decline in non-defense aircraft orders. However, there were some positives, particularly in terms of the 1.3% increase in core capital goods, which followed an upwardly revised 3.1% increase in November.

The Dollar was strong again yesterday, up 0.29%, on the back of the increased RISK AVERSION trade surrounding the fiscal troubles in Greece and a 2.5% increase in the VIX. The Hedgeye Risk Management models have the following levels for DXY – buy Trade (77.81) and Sell Trade (79.26).

A surprising relative outperformer was the Financials (XLF). The Banks were a bright spot yesterday with the BKX up 0.3% on the day Regional and money center names fared the best with C, BAC and JPM up on the day.

The best performing sector yesterday was the Consumer Staples (XLP). RISK AVERSION played a big part in the outperformance, while P&G was up after the company raised its 2010 growth rate.

The RECOVERY trade remained under pressure with Materials (XLB) underperforming the S&P 500 by 60bps. In addition, earnings out of the Technology (XLK) was not met with a warm reception, especially the results out of the communications equipment and semiconductors space. Yesterday the XLK declined 2.9%, with the SOX down 3% and the S&P Communications Equipment Index down 6.95%. QCOM declined 14.2% and was the worst performer after the company guided March quarter EPS below the consensus and MOT declined 12.4% on lower guidance too.

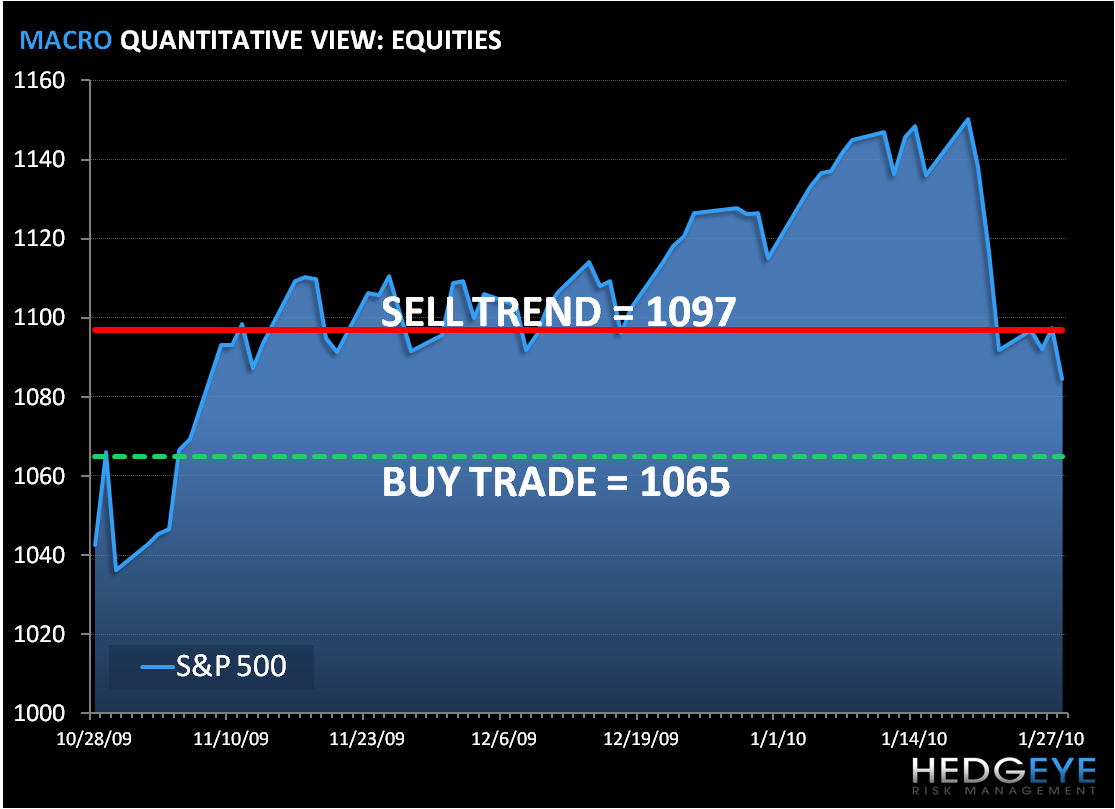

As we look at today’s set up, the range for the S&P 500 is 32 points or 1.7% (1,065) downside and 1.1% (1,097) upside. At the time of writing the major market futures are trading up slightly on the day.

In early trading today, Copper is up slightly, but is looking at its worst monthly loss since December 2008, because of six-year high stockpiles, a stronger dollar and concern about China’s demand. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.10) and Sell Trade (3.32).

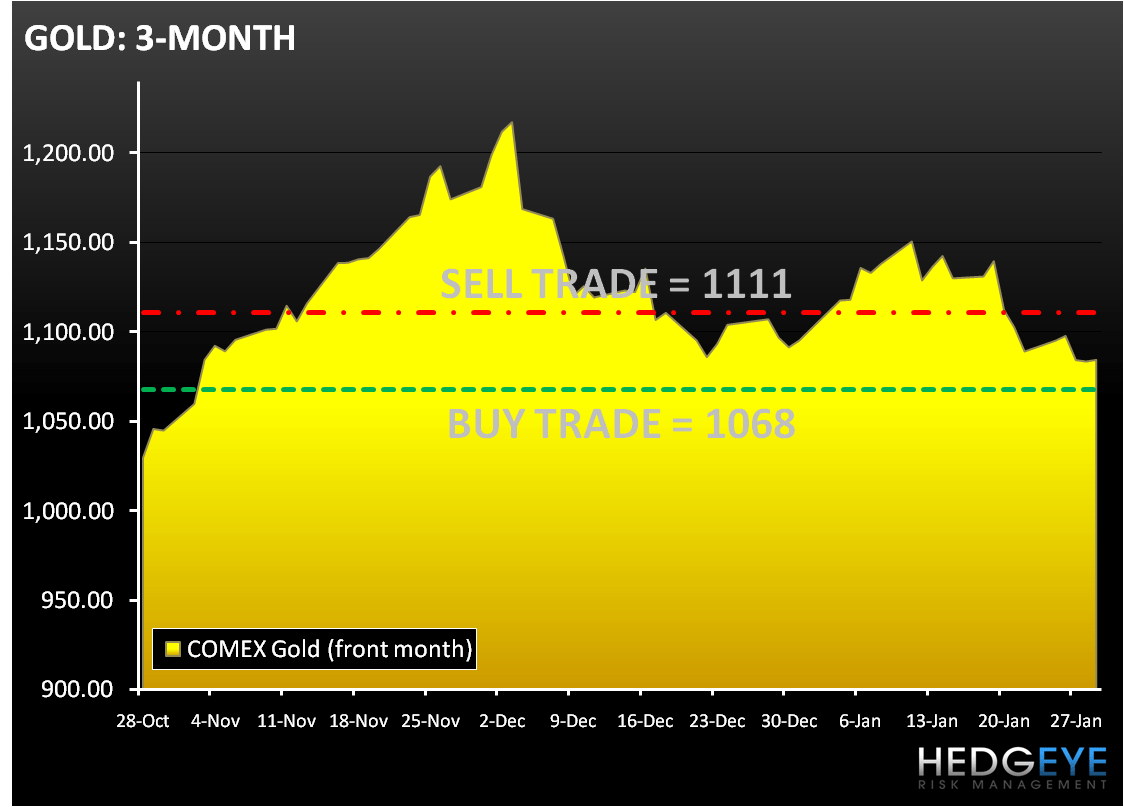

In early trading today Gold is little changed but is headed for its second monthly decline. The decline in gold is consistent with our “BREAK-OUT BUCK” theme. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,068) and Sell Trade (1,111).

Crude oil is trading slightly higher in early trading, but is looking at the second straight weekly decline and first monthly decline since September 2009. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (71.98) and Sell Trade (77.04).

Howard Penney

Managing Director