A head of “the super bowl of politics” today, all of the major indexes closed in the red yesterday. The “super bowls of politics” is our term for today’s testimony of Tim Geithner, the Federal Reserve meeting and capping the day with President Obama’s State of the Union address.

The Washington madness is keeping “government sponsored volatility” at elevated levels. More importantly, the RECOVERY trade continues to feel the pressure on continued concerns about tighter credit conditions in China, as well as renewed sovereign concerns stemming from the S&P's move to cut its outlook on Japan's long-term sovereign debt rating.

This dynamic helped fuel a bounce in the dollar, which was up 0.31% yesterday and 0.73% year-to-date. The Hedgeye Risk Management models have the following levels for DXY – buy Trade (77.70) and Sell Trade (79.09).

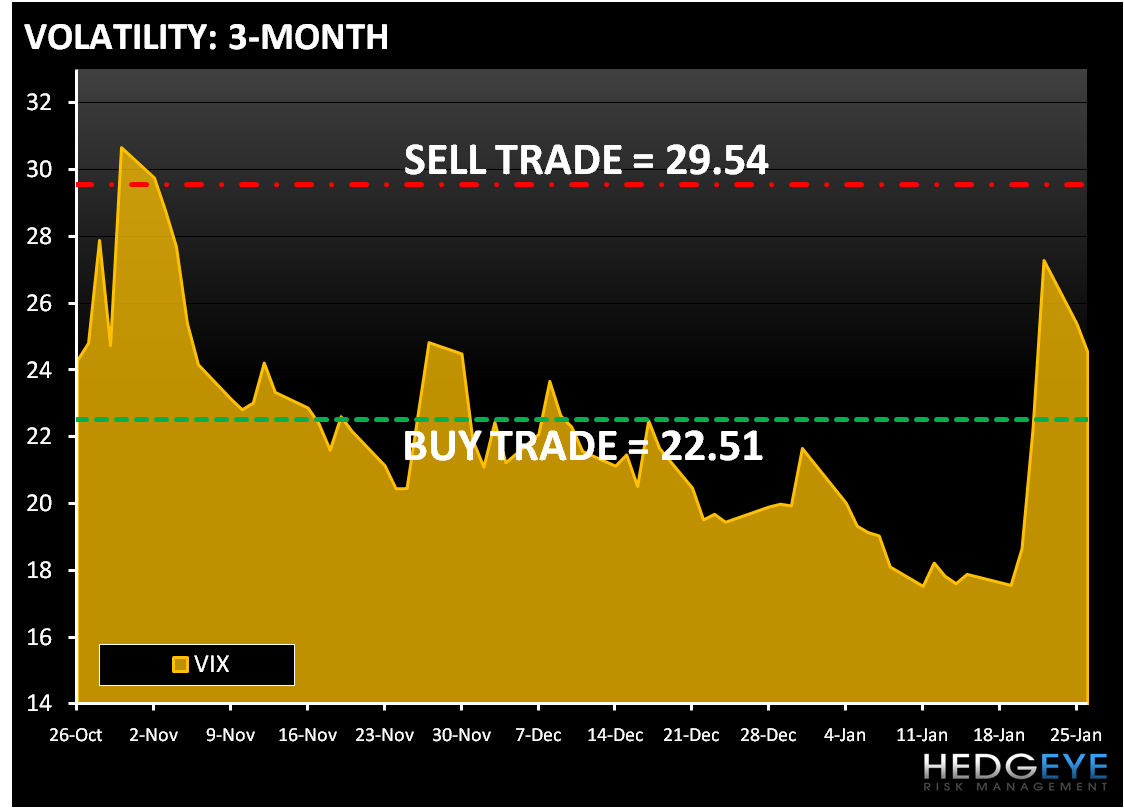

After a 52% move last week the VIX has seen a two day correction, declining 3.38% yesterday, following a nearly 6.96% decline on Monday. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (22.51) and Sell Trade (29.54).

On the positive side of the ledger, there continues to be a favorable reaction to the better-than-expected earnings out of the Technology, Chemicals, Packaging, and Insurance and selected Energy names. The MACRO calendar provided some support as consumer confidence continues to show some improvement and the Case/Shiller home-price index increased for a sixth consecutive month in November.

The worst performing sector yesterday was the Financials (XLF). The banks were a standout underperformer with the BKX down 2.2% yesterday. Financial regulatory reform is forcing the street to re-value the franchises of the nation’s largest financial institutions. The regional names outperformed for the better part of the day before decline into the close.

While Technology closed down 0.3% it slightly outperformed the S&P 500. The outperformance can be attributed to better-than-expected earnings from some high profile names like AAPL. The Semis also outperformed on a relative basis with the SOX down 0.2% on the day.

The RECOVERY trade got hammered yesterday, as Energy (XLE) and Materials (XLB) rounded out the three worst performing sectors after Financials (XLF). The weakness in Asia and the bounce in the dollar are putting significant pressure on the RECOVERY trade. However, parts of the Energy sector held up a bit better on the back of some early strength in the coal and oil services, underpinned by the strong earnings trends. Steel stocks weighed on the materials sector in the wake of a wider-than-expected Q4 loss and disappointing Q1 guidance out of X.

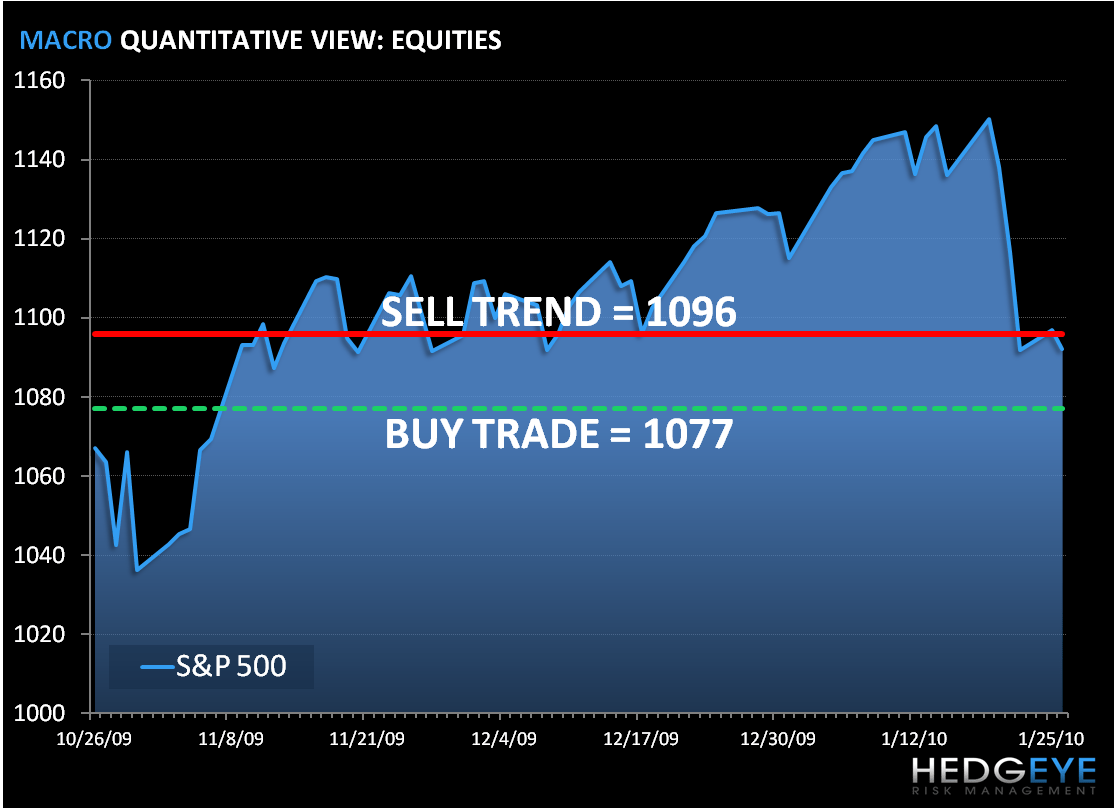

As we look at today’s set up the range for the S&P 500 narrowed significantly from 45 points to 19 points or 1.3% (1,077) downside and0.36% (1,096) upside. At the time of writing the major market futures are trading flattish on the day.

Copper is trading lower in London trading for the second day on speculation that China will curb lending. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.28) and Sell Trade (3.32).

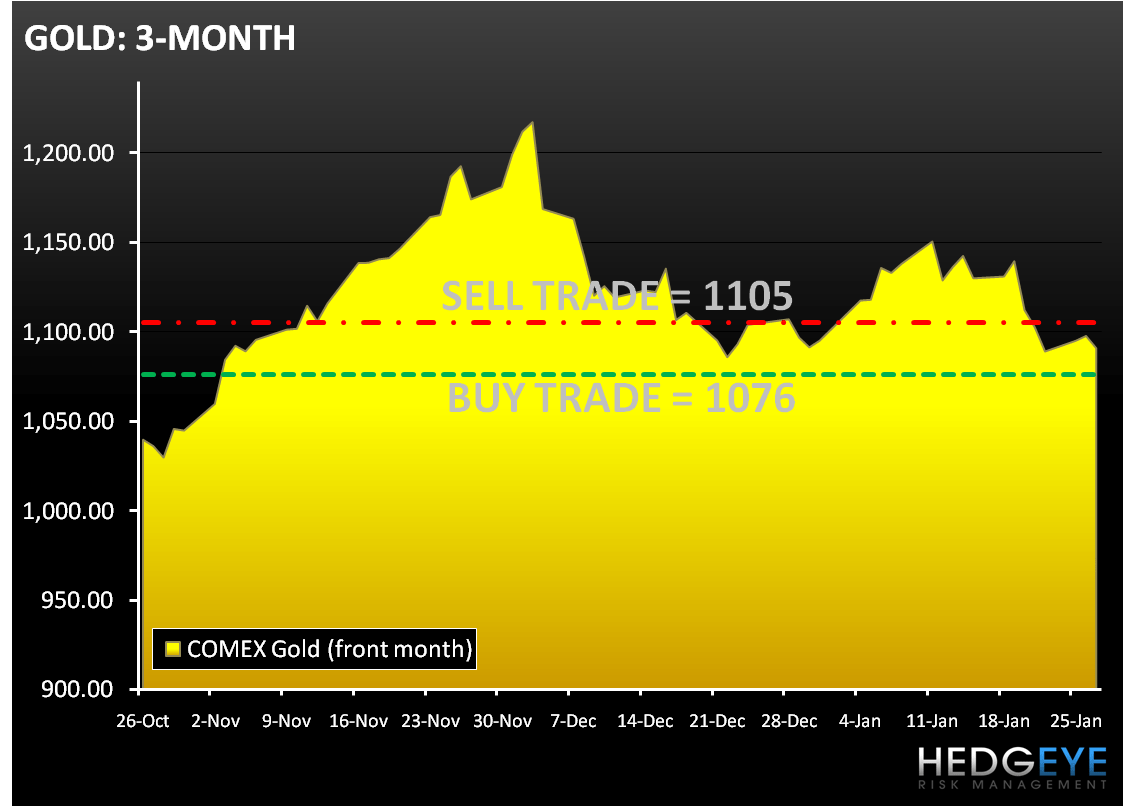

In early trading today Gold is little changed but is headed lower on the outlook for a stronger dollar. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,076) and Sell Trade (1,105).

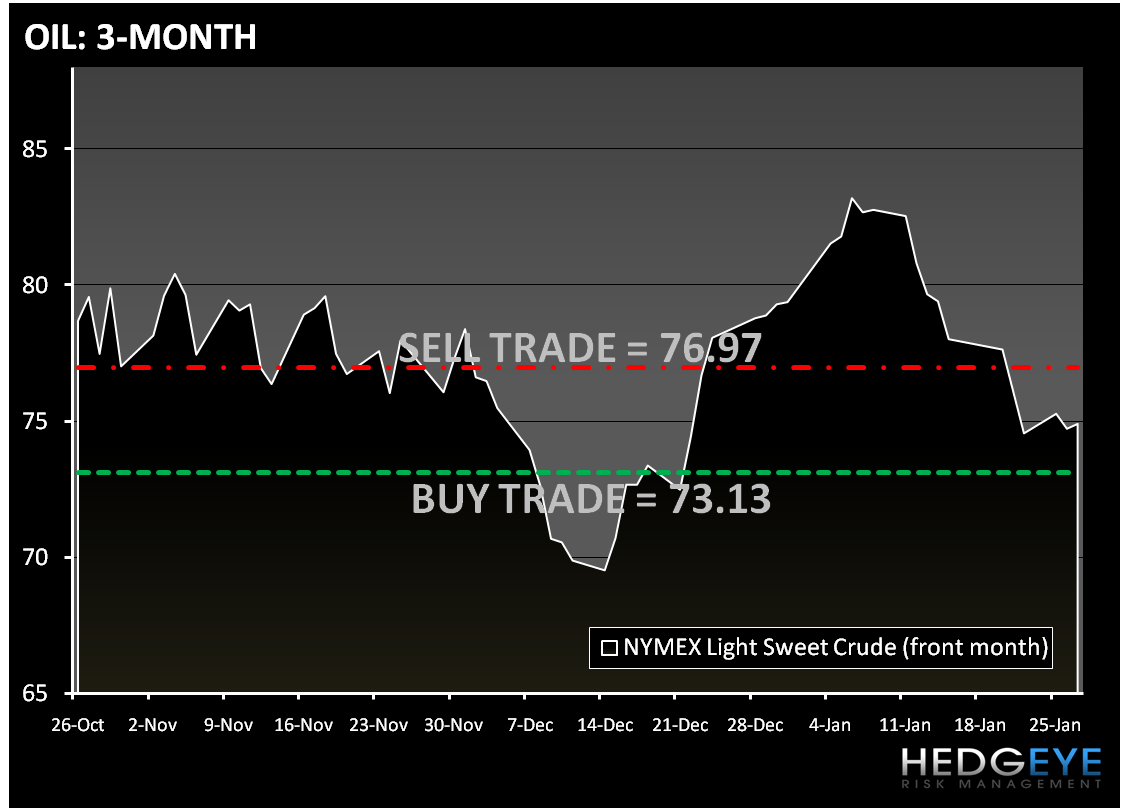

Crude oil is trading little changed ahead of the latest numbers on U.S. inventories. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (73.13) and Sell Trade (76.97).

Howard Penney

Managing Director