The major indexes – the Dow, S&P, NASDAQ and Russell - all closed at new highs for the year. The big winner on the day was the continued outperformance of the Healthcare (XLV) as it outperformed the S&P 500 by 120bps on expectations of a Republican victory in the Massachusetts.

The Hedgeye sector models are back to having all nine sectors positive on TRADE and TREND.

Also on the positive side were increased M&A activity and some better-than-expected earnings/guidance from Parker Hannifin. Yesterday the market seemed to ignore another tightening move out of China and the Greek budget deficit crisis. Other MACRO data points should have presented some additional headwinds. The National Association of Home Builders index of builder confidence decreased to 15 from 16 the prior month to the lowest level since June 2009. After the close the ABC consumer confidence declined for the second week in a row.

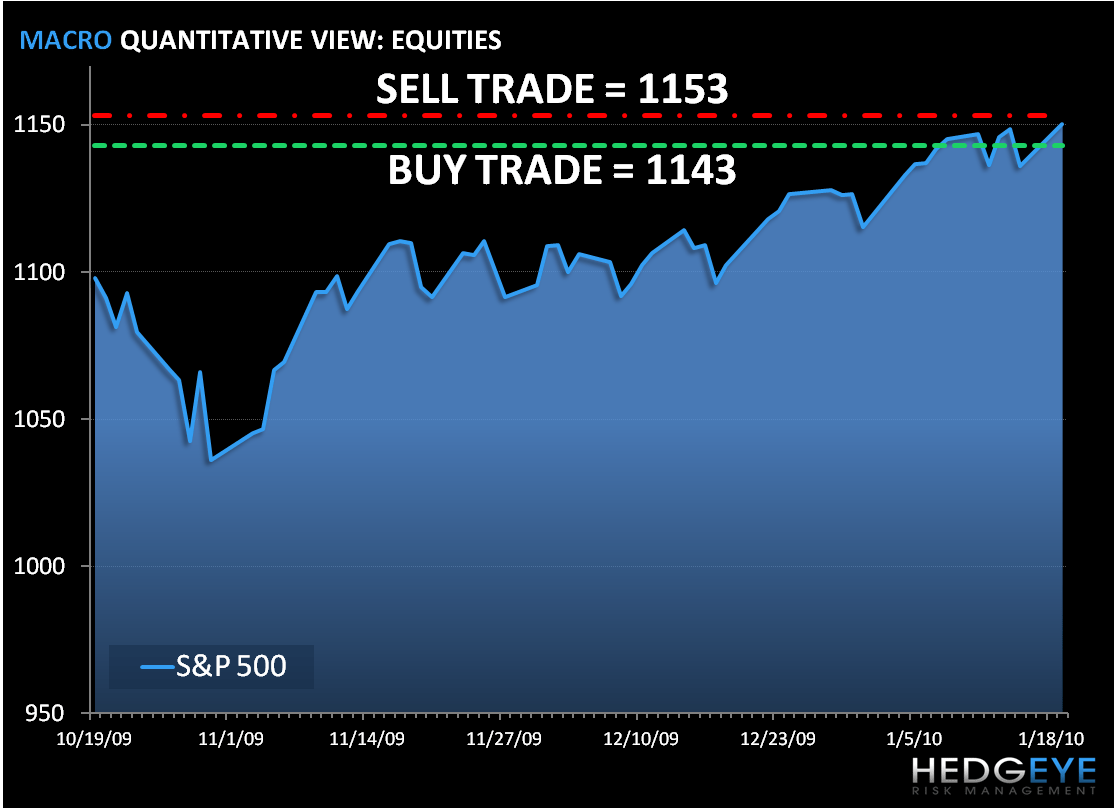

As we look at today’s set up the range for the S&P 500 narrowed from 20 points on Friday to 10 points or 0.60% (1,143) downside and 0.3% (1,153) upside. At the time of writing the major market futures are trading down on the day.

Yesterday, Technology (XLK) was the second best performing sector. Within the XLK the communications equipment group provided upside leadership and AAPL +4.4% was the highlight in the hardware space after the company confirmed it will be holding a 27-Jan event to launch its “latest creation”. Semis rebounded from a 6% selloff last week with the SOX +1.8%.

Despite virtually no MACRO data points, parts of the RECOVERY trade outperformed. The Materials (XLB) sector has been down 4 of the last 5 days, but was the third best performing sector yesterday. Steel stocks were among the best performers in the group with the S&P Steel Index +2.9%.

The Financials (XLF) rebounded from a 2% decline on Friday, though the banking sector was a slight laggard. Citigroup outperformed the large-cap group after reporting Q4 results. The regional banks outperformed with ZION and PNC among the notable gainers.

In early trading Copper is trading down on China tightening concerns. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.28) and Sell Trade (3.49).

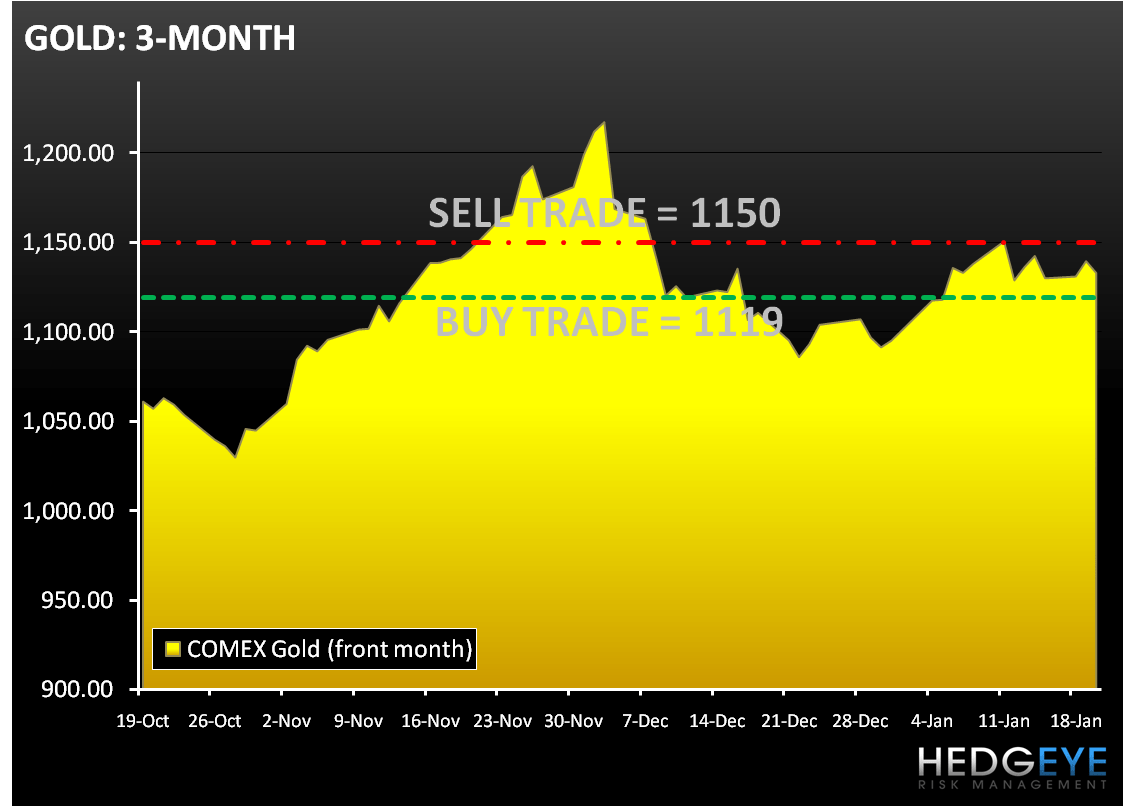

In early trading Gold is trading down about 0.8% to 1,130. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,119) and Sell Trade (1,150).

Yesterday crude traded up by 1.3%, but is giving back all the gains in early trading today. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (77.51) and Sell Trade (81.10).

Howard Penney

Managing Director