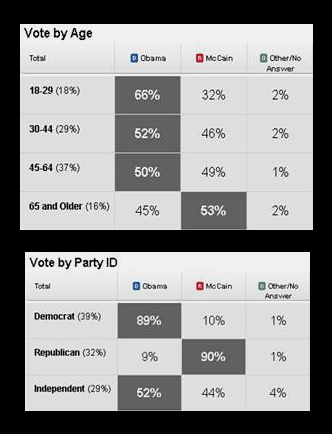

With the odd turn of events into the Massachusetts special election, one of our top 10 ‘probable improbables’ (presented on 1/8/10) is looking even more scary. Number 8 on our list is, “labor and the threat of unionization become a major issue in 2010”. The could be a big, big deal for retail.

As it stands, the Employee Free Choice Act (EFCA) was introduced and championed by the late Senator Ted Kennedy. Today’s candidates are on complete opposite sides of the topic. Coaklely (D) is a strong advocate of the bill and vows to continue to keep Kennedy’s legacy alive. Brown (R) strongly opposes the EFCA, and with his lead at the polls, could put the bill into jeopardy. Regardless of the outcome, there is no question that the idea of increased labor organization is gaining mindshare. While our original thoughts may be slightly altered with a Republican victory, the key point is worth republishing.

#8. Unionization Becomes a Major Issue. Regardless of your political view, one thing that is pretty difficult to deny is that after a tough 2009, Obama is backed into a corner as it relates to placating the masses. He’s not doing so with the Economy, and certainly not with Afghanistan. Health Care Reform is likely a bust. So what’s next? Stepping up to vilify the self-proclaimed Wall Street Elite much the same way FDR did in launching the Mellon Tax Trials in 1935 (Andrew Mellon was then the former Treasury Secretary, and the richest man in America). For what it’s worth, Mellon was exonerated, albeit two years after he died. So goes the shallow world of politics.

Is this possible today? You bet. But another way to show his support for those that voted for him, Obama could go the Labor route. Tom Tobin, our Health Care Sector hear, said it perfectly…

“Kids and independents elected Obama. It may be that the 2010 midterm elections do not matter since the likelihood of losing a majority in the House appears slim. But a political focus would also have to include the 2012 Presidential election as well. Where Labor was a factor in the 2008 elections, replacing the optimistic kids who were on a messianic mission and the independents will be a tall order. This is why I have the Employee Free Choice Act on my radar. I think Obama may have made a mistake in pushing Health Reform I first, but rather should have used his fleeting political capital to secure what will surely be an enduring and growing base of union members should the Bill pass.”

What does this mean for retail? Everything! Call a retailer and ask them what this means. They’ll probably say something that sounds like “We pay our store employees well and don’t think this is a problem.” C’mon man, are you kidding? Don’t you realize that you should be monitoring the gap between your pay and work rules and those of your competition? Also, if you’re managing an Abercrombie, your competition for employees is not just American Eagle. It’s also the Nathan’s selling greasy hot dogs in the food court. Retailers should turn to China to see how labor changed the competitive landscape. Why did factory wages rise in China by over 30% in 2006? Because the migrant workers coming in to factories to cut, sew, glue, and generally get treated like dirt by non-compliant factories saw that they could go to a major city like Beijing and work at a KFC instead for more money and a better lifestyle. This is an extreme example, of course, but if this Employee Free Choice Act gains traction, then it will be a big, big deal for retail.