In physics, defining a "downward" direction, buoyancy is the upward force, caused by fluid pressure which keeps things afloat; this force enables the object to float or at least seem lighter. While the S&P 500 is not floating on liquid it’s floating on the free money policy of the Federal Reserve.

One day after all the major indexes all posted their biggest one-day losses for 2010, the market came back strong with every sector in positive territory yesterday. It should be noted that the quality of the rally yesterday was low as the volume on the NYSE declined 11.6% sequentially.

From a MACRO standpoint there did not seem to be any specific catalyst behind yesterday’s move, though one of positive dynamics was acceleration in mortgage applications which increased 14.3% from 0.5% last week.

The best performing sector yesterday was Healthcare (XLV), rising 1.3%. The pharma group was one of the bright spots with the positive tone set by upgrades at Credit Suisse. The facilities and Biotech names also outperformed; the Amex Biotech index has only declined twice so far in 2010.

After turning in the worst sector performance on Tuesday, the Financials (XLF) outperformed the S&P 500 by 30bps on Wednesday. On the back of acceleration in mortgage applications, the mortgage insurance group outperformed the overall index. Within the banking group, the regional’s put in the best performance.

In a surprising move the Technology (XLK) sector outperformed the S&P 500 by 20bps. A bulk of the outperformance came from a rebound the semi names, as the SOX increased 1.6% after falling the previous two days. Also bucking the downward trend were Software stocks with the S&P Software Index up 1.1%.

The worst performing sector yesterday was Energy (XLE). The XLE underperformed as crude oil declined for the fifth straight day. Oil stockpiles rose by 3.7M barrels last week vs. expectations for a 1.5M barrel build. In addition, distillate inventories increased 1.35M barrels vs. expectations for a 1.3M barrel draw.

Slowing growth in China is also a concern for the RECOVERY trade, although the Materials (XLB) was the second best performing sector yesterday.

The range for the S&P 500 is 18 points or 0.8% (1,155) upside and 0.7% (1,137) downside. At the time of writing the major market futures are trading flat on the day.

Yesterday the CRB finished higher by 0.28% on the back of the Industrials and Precious metals. Once again the soft commodities and Grains were the worst performing.

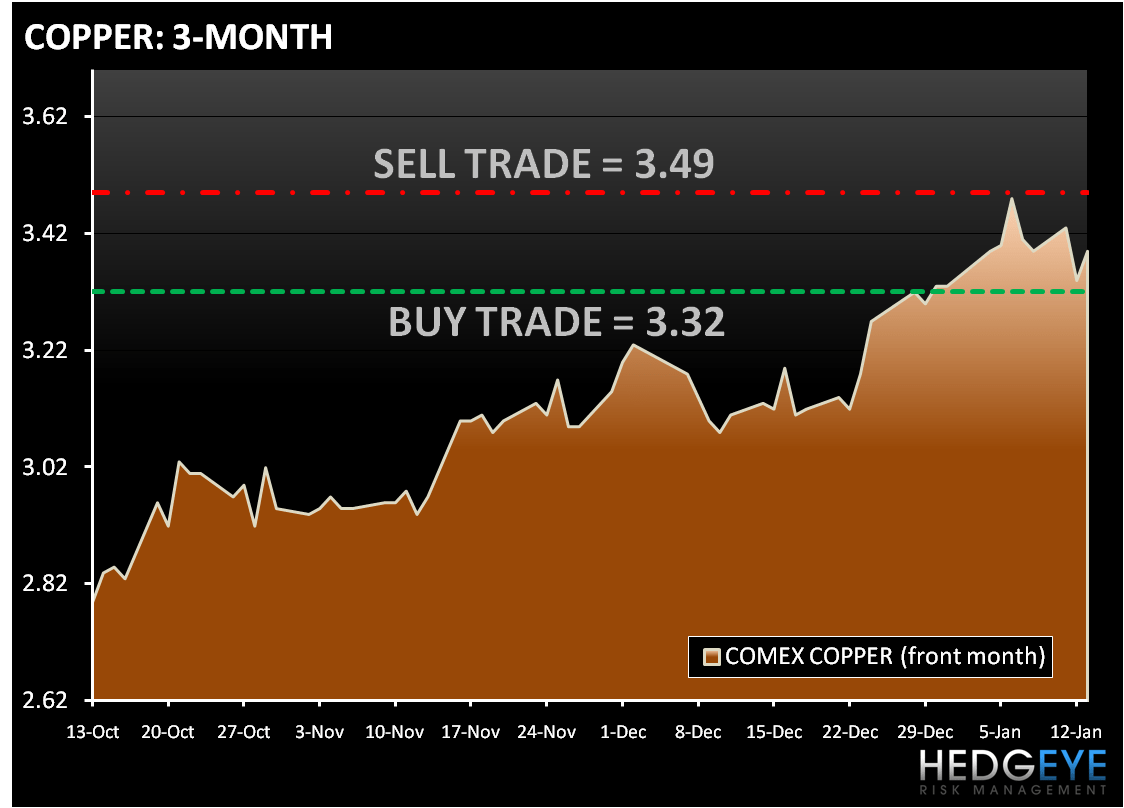

In early trading today Copper is trading higher, after increasing 1.5% yesterday. The Hedgeye Quant models have the following levels for COPPER – buy Trade (3.32) and Sell Trade (3.49).

Gold is trading in a narrow range. It traded up modestly yesterday and is down in early trading today at $1,134. The Hedgeye Quant models have the following levels for GOLD – buy Trade (1,120) and Sell Trade (1,158).

Yesterday, crude oil traded down for the third day in a row and is trading flat in early trading. As we mentioned, the supply picture is putting pressure on the commodity. The Hedgeye Quant models have the following levels for OIL – buy Trade (79.22) and Sell Trade (84.11).

Howard Penney

Managing Director