One of our key themes for 1Q10 is – CHINESE OX IN A BOX – and it’s important to watch what the Chinese are saying. In simple terms, they are all about QUALITY GROWTH not SPECULATIVE GROWTH. Right now in “real time” the Chinese self imposed slowdown in lending has the Chinese market down for 3 of 4 trading days in 2010. The Shanghai A share index declined 1.89% last night and is now down 2.58% so far in 2010.

In the USA, after three days of trading all nine sectors are positive on TRADE AND TREND! There was generally a positive tone to the performance of the S&P 500 yesterday with seven of the nine sectors outperforming. The volume is still on the light side as it seems like market participants are looking for guidance on which way to turn. The MACRO calendar could paint a clearer picture with some direction from December same-store sales data and Friday's release of December nonfarm payrolls.

Yesterday’s MACRO calendar did not support the momentum provided by Monday's release of better-than-expected manufacturing data. Yesterday, the sectors that benefit the most from the RECOVERY trade - Materials (XLB) and Energy (XLE) - extended their outperformance in 2010.

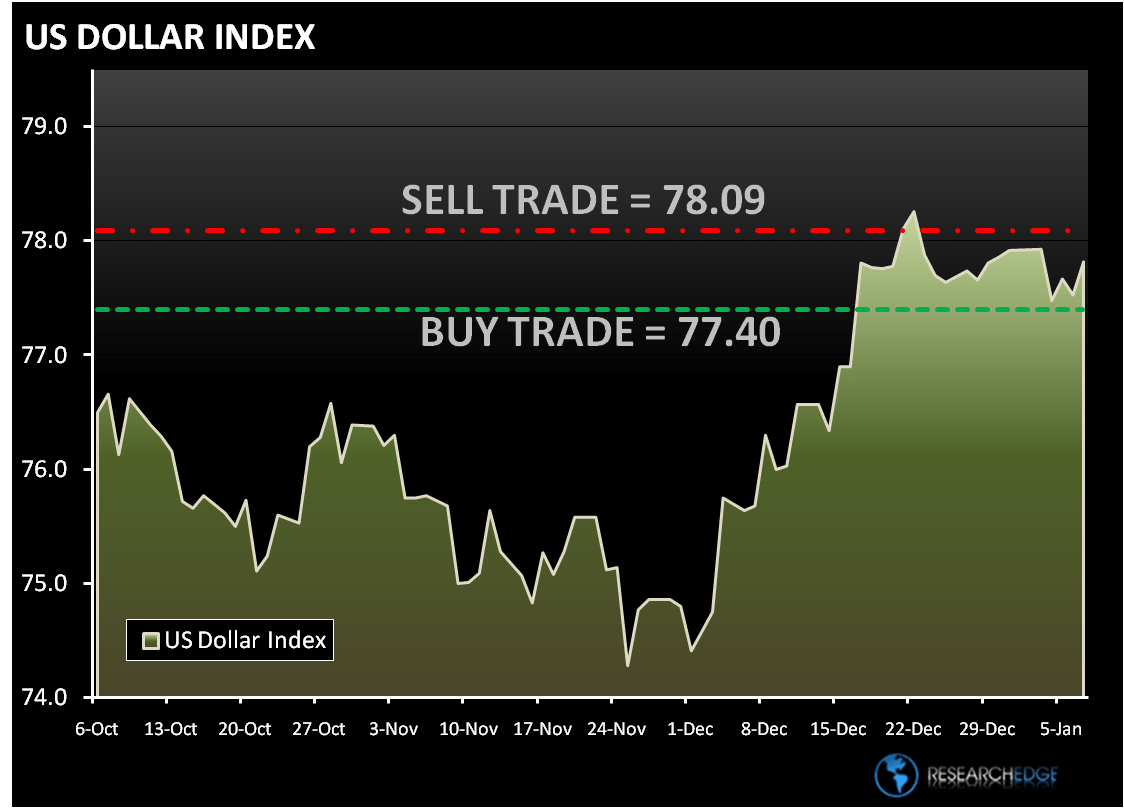

Additional support to the RECOVERY trade came from the Dollar Index sliding to 77.49, down 0.16%. The RISK trade continues to come out of the market with the VIX down (-0.98%) yesterday and has declined every day this year, but the higher beta NASDAQ and Russell underperformed yesterday.

Yesterday, the ISM non-manufacturing index moved into expansionary territory last month, rising to 50.1 from 48.7 in November. However, the reading was slightly below the consensus of 50.5 and the forward-looking new orders component fell to 52.1 from 55.1. While employment improved to 44 from 41.6, it remained firmly in contraction territory.

Also on the MACRO calendar, the ADP private payrolls fell by 84,000 in December, a figure that was weaker than 75,000 decline expected by economists in a Bloomberg survey. Yesterday’s reported decline in the ADP numbers was a significant improvement from the 145,000 decline reported in November 2009. In addition, December marked the ninth consecutive month in which the pace of job cuts slowed.

The Materials (XLB) was the best performing sector yesterday and extended 2010 outperformance to 320bps. The CRB was up 1.45% yesterday as commodities and commodity equities remained underpinned by the global recovery trade. Precious metals stocks were also a bright spot, and the fertilizer stocks put in another day of outperformance.

While the XLF was not one of the top three performing sectors, it did outperform. The BKX in now up three days in a row, up 5.79% so far this year. The laggards in the sector were names such as ICE (3.1%), MCO (2.1%) and IVX (2.1%).

The notable laggard yesterday was Technology (XLK) down 1.1% on the day. While there was no visible catalyst, telecom and software stocks were the weakest group in the XLK.

The range for the S&P 500 is 14 points or 0.4% (1,141) upside and 1.0% (1,127) downside. At the time of writing the major market futures are trading lower on the day.

Copper fell 0.93% yesterday and is trading lower today on concern that demand may wane as China moves to curb growth in bank lending. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.35) and Sell Trade (3.50).

Gold fell the most in a week in London as a stronger dollar curbed demand for the metal as a hedge against weakness in the currency. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,086) and Sell Trade (1,137).

Crude oil fell in New York, snapping 10 days of positive performance. The Energy Department said crude inventories rose 1.3 million barrels last week, the first increase in five weeks. The Research Edge Quant models have the following levels for OIL – buy Trade (79.72) and Sell Trade (83.57).

Howard Penney

Managing Director