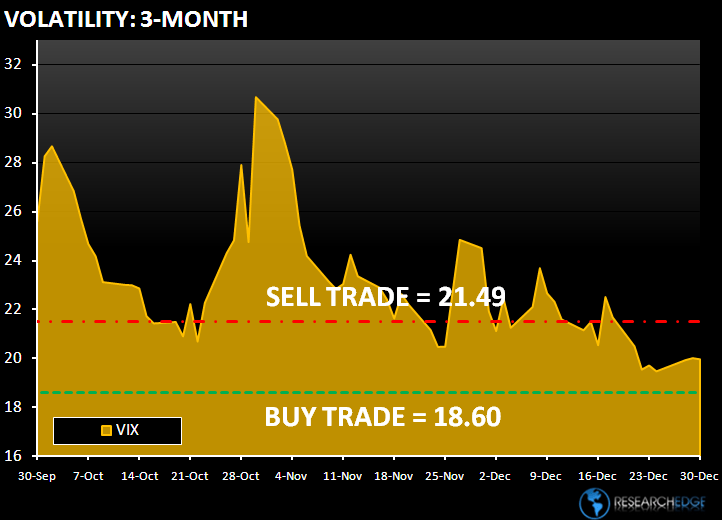

Optimism about the market is at the highest level since April 1987. Yesterday, the Investors Intelligence pessimism level fell to 15.6% from 16.7% last week. Sentiment has improved since October 2008, when the financial crisis drove the figure to a 14-year high of 54.4%. Volatility is the other extreme. The VIX closed at 19.96 yesterday down 0.25% and is now down 50% in 2009.

The Dollar Index has traded higher for the past two days, but is looking at its biggest decline since December 1st in early trading today.

With the market painfully quiet and volume on the NYSE at the lowest levels of the year, preparing for next week seems like time better spent. The MACRO calendar is busy next week: ISM manufacturing data on Monday, Pending home sales and domestic vehicle sales on Tuesday, MBA mortgage applications on Wednesday and the December payrolls data on Friday. On the corporate front, we will be getting the much anticipated holiday sales updates from the retail community.

Yesterday, the S&P 500 closed flat on the day, with only two sectors positive – Technology and Financials. On the MACRO calendar there were no significant headlines yesterday, outside of the better-than-expected Chicago Purchasing Managers reading. The Chicago PM could be a precursor to next week's ISM number. The Chicago PM increased to 60 from 56 in November and was above the consensus of 55.

Technology was the best performing sector yesterday as semis and hardware led the way. NVDA and DELL were the two best performing stocks (following upgrades) while MSFT was the notable underperformer. The Financials also outperformed, led by Real Estate management companies and the brokers – the two best performing stock were CBG and GS. The Research Edge MACRO models have the XLF broken on both the TRADE and TREND durations.

The notable underperformer yesterday and for the past week is Energy (XLE). Crude oil rose for a seventh day as shrinking U.S. crude stockpiles increase confidence that demand is recovering. Increased geopolitical concerns and the tensions in IRAN are also helping crude trade near the $80 level. The XLE underperformed the S&P 500 by 0.1% yesterday and 0.8% over the past week. The Research Edge Quant models have the following levels for OIL – buy Trade (76.49) and Sell Trade (80.76).

The range for the S&P 500 is 22 points or 1.0% upside and 1.0% downside. At the time of writing, the major market futures are trading flat on the day. Today on the MACRO calendar Initial jobless claims are due out at 8:30; consensus is for 460,000 versus the prior reading of 452,000

COPPER is up five of the last six days, trading at the highest price in almost 16 months. Copper continues to trade higher on speculation that supplies from Chile, the world’s largest producer, may be disrupted by a mine strike. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.17) and Sell Trade (3.38).

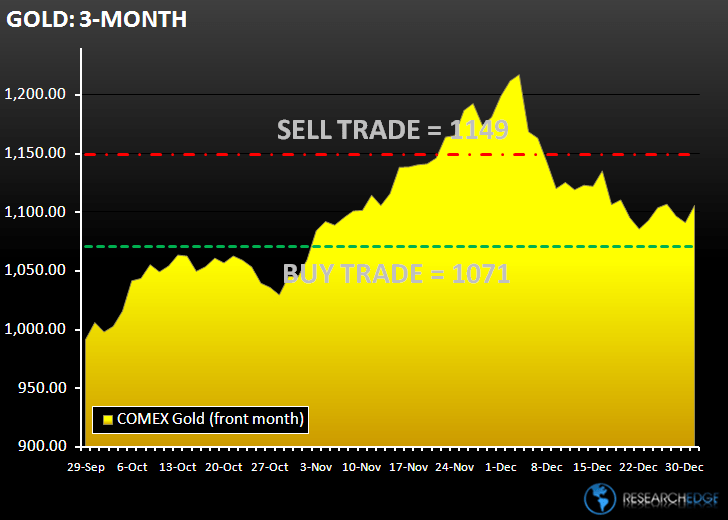

In early trading today GOLD is trading up $15.00 to 1,107.50. Gold is up 24% this year and is now looking at its 9th annual gain in 2009. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,071) and Sell Trade (1,149).

Howard Penney

Managing Director